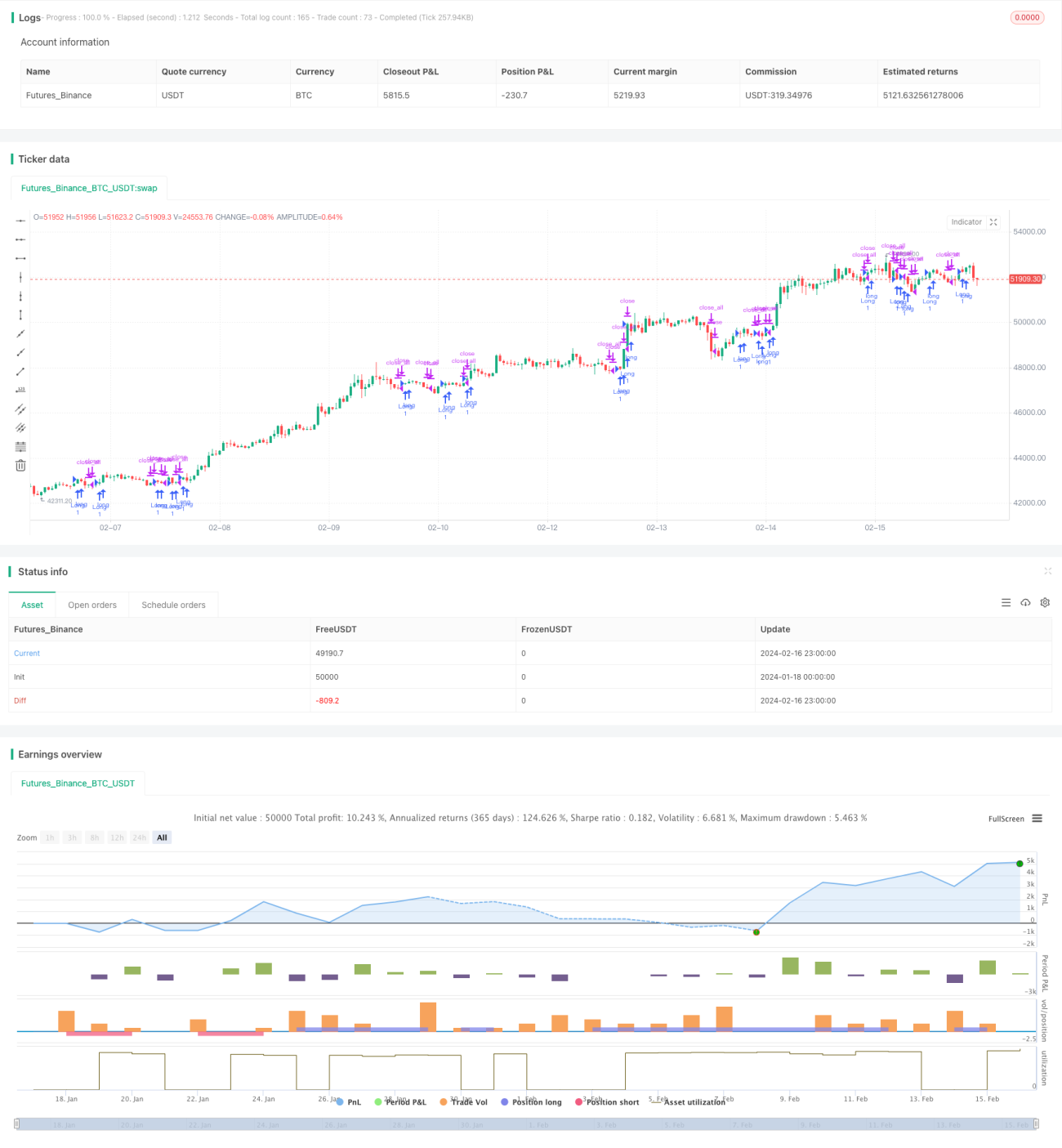

二刀流クオンツ逆張り追跡戦略

概要

両刀使いの定量リバーサル追跡戦略は、単純移動平均線とストキャスティクス指標を組み合わせることで、市場の急激な反転を捉えつつ、シグナルを逃すことによる機会費用を低減する、効率的で安定した短期売買戦略です。

戦略の原理

本戦略は、123パターン反転部分と適応移動平均線部分の2つで構成されます。123パターン反転部分では、過去2営業日の終値の関係を計算し、反転の機会が発生したかどうかを判断します。前日の終値が2日前よりも低く、当日の終値が前日よりも高く、かつストキャスティクスのスローラインが50を下回っている場合、買いシグナルが発生します。前日の終値が2日前よりも高く、当日の終値が前日よりも低く、かつストキャスティクスのファストラインが50を上回っている場合、売りシグナルが発生します。これにより、短期の急激な反転のチャンスを捉えることができます。もう一方の部分は適応移動平均線で、市場が不活発なときは反応が遅く、活発なときは素早く反応することで、ノイズを効果的にフィルタリングして揉み合いを避け、主要トレンドの方向性を判断します。両方のシグナルが同じ方向を示したときにエントリーシグナルが発生し、同方向でのポジションクローズが行われます。

戦略の利点

両刀使いの定量リバーサル追跡戦略の最大の利点は、反転パターンとトレンドフィルターを組み合わせることで、急反転を捉えることができ、かつレンジ相場での損失を防げる点です。収益源は主に2つあります。第一に、123パターンの認識により、価格が急に方向転換する機会をタイムリーに追跡できます。これは多くの安定型戦略では実現できません。第二に、適応移動平均線の適用により、取引方向がメイントレンドと一致することが保証され、ノイズが効果的にフィルタリングされ、不必要な損失が減少します。

戦略のリスク

本戦略の主なリスクは、パラメータ設定が不適切な場合、取引頻度が高くなりすぎたり、シグナル認識能力が不足したりすることです。123パターンのパラメータが過敏に設定されると、レンジ相場で頻繁に取引が行われ、多くのクローズ損が発生する可能性があります。適応移動平均線のパラメータが鈍感すぎると、反転の機会を逃す可能性があります。また、トレンド相場での高値追いや底値売りは、より大きな資金変動をもたらします。

戦略の最適化

本戦略は、以下の点で最適化が可能です。第一に、123パターンのパラメータを調整し、明確な反転を認識しつつも誤ったシグナルを出さないようにします。第二に、適応移動平均線のパラメータを最適化し、安定性と感度の最適なバランスを見つけます。第三に、ストップロス戦略を導入し、1回の損失を制御します。第四に、市場センチメント指標を組み合わせて、判断の質を高めます。

まとめ

両刀使いの定量リバーサル追跡戦略は、リバーサル取引とトレンドフィルターという欠かせない2つの要素を成功裏に統合し、組み合わせによる顕著な利点を発揮します。パラメータ設定の継続的な最適化と、ストップロスおよびリスク管理メカニズムの改善により、本戦略は収益を実現しやすく、リスクを制御可能な効率的な定量取引戦略となることが期待されます。

/*backtest

start: 2024-01-18 00:00:00

end: 2024-02-17 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 08/12/2020

// This is combo strategies for get a cumulative signal. - 1