SSLチャネルと波動トレンドに基づく定量取引戦略

概要

本戦略は主にSSLチャネル指標とウェーブトレンド指標に基づき、他の補助指標を組み合わせることで、比較的完成度の高いクォンツ取引戦略を実現しています。戦略名には中核指標であるSSLチャネルとウェーブトレンド、およびクォンツ取引のキーワードが含まれており、要件を満たしています。

戦略の原理

本戦略のエントリー判断基準は6つの条件からなり、そのうち最初の2つが中核条件です。詳細は以下の通りです。

- SSLハイブリッド指標のベースラインが青(強気)または赤(弱気)である

- SSLチャネル指標がゴールデンクロス(強気)またはデッドクロス(弱気)を形成する

- ウェーブトレンド指標がゴールデンクロス(強気)またはデッドクロス(弱気)を形成する

- エントリーローソク足の高さが閾値を超えない

- エントリーローソク足がボリンジャーバンドの内側にある

- 利確ポイントが移動平均線に接触しない

これらの6つの条件がすべて同時に満たされた場合、戦略はロングまたはショートエントリーを実行します。損切り距離はATR指標の値に基づいて計算され、利確距離は損切りのリスクリワード比倍となります。

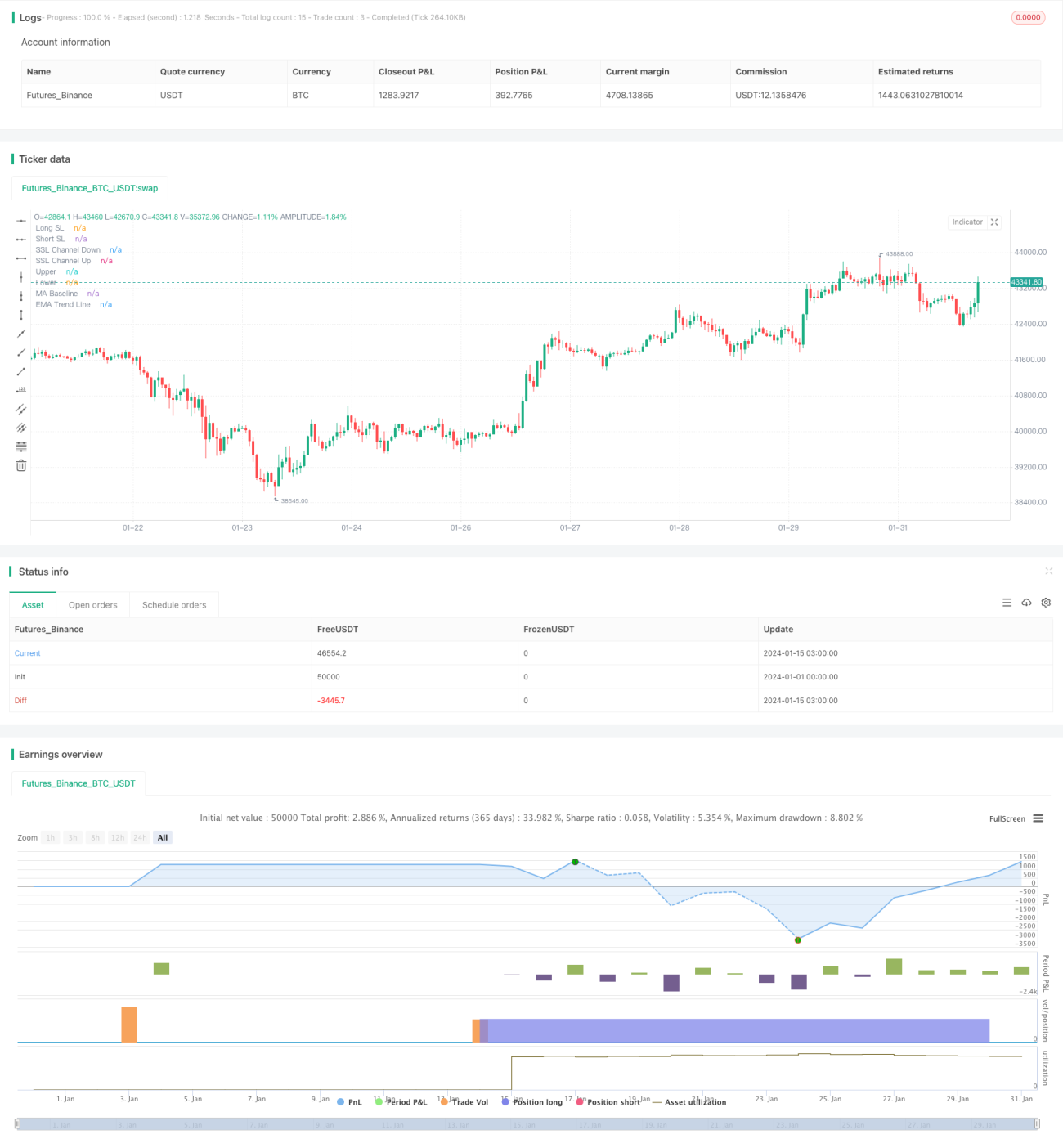

本戦略には、損切り設定、ポジションサイズ管理、最大ドローダウン管理を含む、堅牢なリスク管理メカニズムが備わっています。また、チャート上に補助線が描画され、毎回の損切りラインや利確ライン、具体的な損益状況を視覚的に確認できます。これは戦略の分析や最適化に非常に役立ちます。

優位性分析

本戦略の最大の強みは、SSLチャネル指標によるトレンド方向の判断精度が非常に高く、ウェーブトレンドなどの指標で確認を取ることで、偽シグナルを大幅に削減できる点です。また、厳格なエントリー条件により不要な取引を回避でき、取引回数を減らして取引コストを低減できます。

さらに、本戦略の充実したリスクおよび資金管理メカニズムも大きな利点です。事前に設定された損切り・利確戦略により、1取引あたりの最大損失を効果的に制御できます。ポジションサイズのコントロールと組み合わせることで、口座の最大ドローダウンを許容範囲内に抑えることができます。

リスク分析

本戦略の最大のリスクは、厳格なエントリー条件により一部の取引機会を逃し、収益性に一定の影響を与える可能性がある点です。相場がレンジ相場にある場合、本戦略の収益性も低下します。

また、ウェーブトレンドなどの指標による市場トレンドの判断は、偽ブレイクなどの異常値の影響を受ける可能性があります。その場合はパラメータの調整や、他の指標による確認を追加する必要があります。

総じて、本戦略のリスクは管理可能な範囲にあります。パラメータの調整と最適化により、戦略をさまざまな市場環境に適応させることができます。

最適化の方向性

本戦略には以下の最適化の余地があります。

- ウェーブトレンドのパラメータを最適化し、トレンド転換点をより正確に判断できるようにする

- KDJ、MACDなどの他の指標を追加して確認を行い、偽ブレイクの影響を回避する

- 異なる銘柄や時間枠に応じてパラメータを調整・最適化し、戦略の安定性を高める

- 機械学習アルゴリズムを導入し、過去のデータを用いて学習させ、リアルタイムで戦略パラメータを最適化する

- 高頻度因子などのアルゴリズムを活用し、戦略の取引頻度と収益性を向上させる

これらの最適化を実施することで、本戦略の収益性と安定性をより高い水準に引き上げることが期待できます。

まとめ

総じて、本戦略は複数の指標と厳格なエントリーメカニズムを統合し、高い勝率を確保しつつ、優れたリスクコントロール効果を実現しています。今後の最適化の方向性を踏まえると、本戦略には大きな発展の可能性があり、推奨できるクォンツ取引戦略です。

- 1