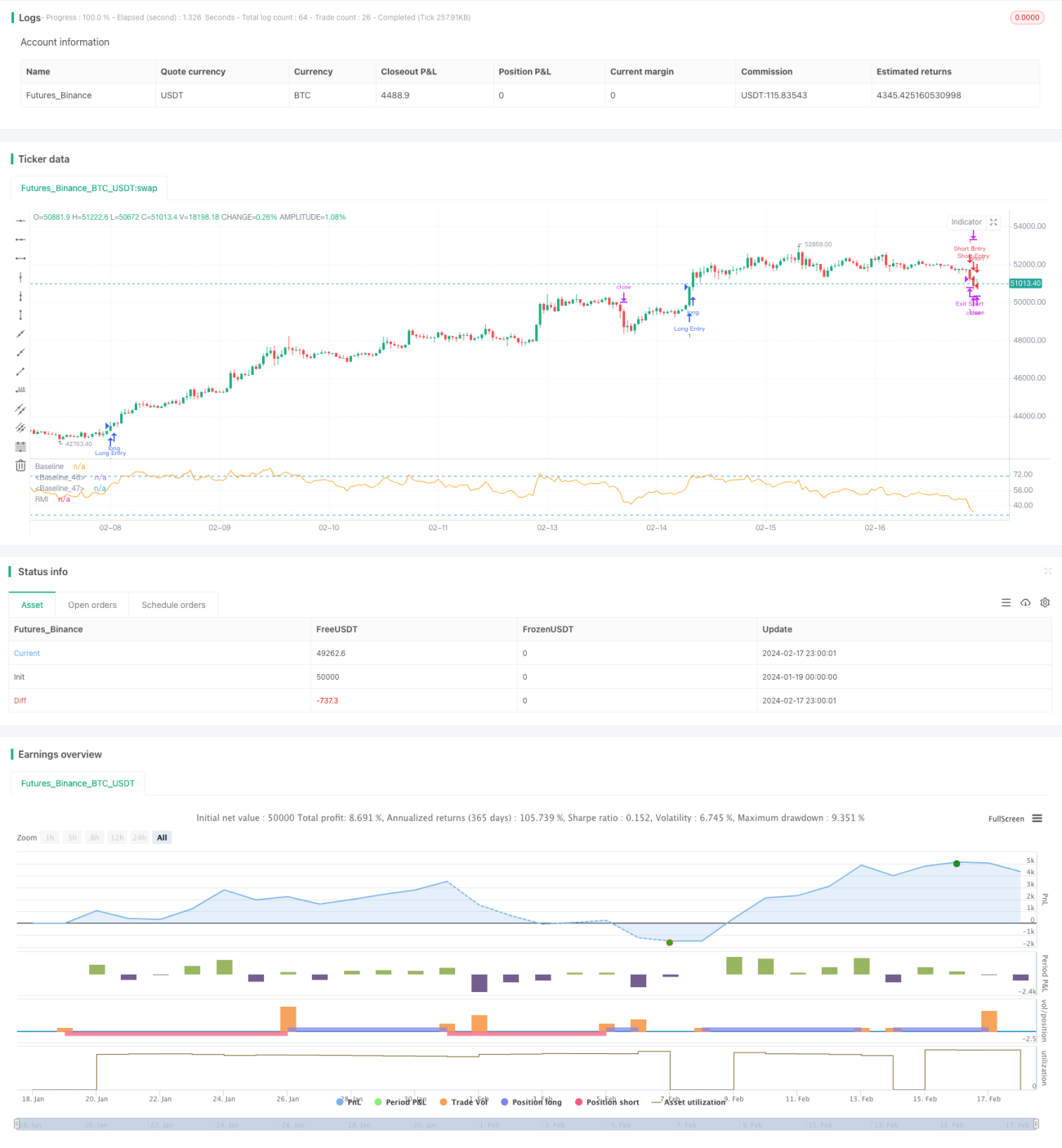

モメンタムトレンド同期戦略

概要

モメンタムトレンド同期戦略は、相対モメンタム指数(RMI)とカスタムのpresentTrendインジケーターを組み合わせた取引戦略です。この戦略は多層的なアプローチを採用し、モメンタム分析とトレンド判断を統合することで、トレーダーにより柔軟で高感度な売買メカニズムを提供します。

戦略の原理

RMIインジケーター

RMIは相対力指数(RSI)の変種であり、過去一定期間の価格変動に対する上昇・下降モメンタムの大きさを測定します。計算式は以下の通りです。

RMI = 100 – 100 / (1 + 上昇平均値 / 下降平均値)

- 上昇平均値は過去N期間の平均上昇幅

- 下降平均値は過去N期間の平均下降幅

RMIの値は0から100の間を取り、値が大きいほど上昇勢力が強く、小さいほど下降勢力が強いことを示します。

presentTrendインジケーター

presentTrendインジケーターは、真の変動幅(ATR)と移動平均線を組み合わせてトレンド方向および動的サポート・レジスタンスラインを判断します。計算式は以下の通りです。

-

上限バンド:移動平均線 +(ATR × F)

-

下限バンド:移動平均線 –(ATR × F)

-

移動平均線は過去M期間の終値平均

-

ATRは過去M期間の平均真の変動幅

-

Fは感度を調整する乗数

価格がpresentTrendの上下バンドをブレイクすると、トレンド転換を示し、潜在的なエントリーまたはエグジットのシグナルとなります。

戦略ロジック

エントリー条件:

- ロング:RMIが閾値(例:60)を超え、強い強気モメンタムを示し、かつ価格がpresentTrendの上限バンドを上回り、上昇トレンドが確認された場合にロングエントリー。

- ショート:RMIが閾値(例:40)を下回り、強い弱気モメンタムを示し、かつ価格がpresentTrendの下限バンドを下回り、下降トレンドが確認された場合にショートエントリー。

エグジット条件(動的ストップロス付き):

- ロングエグジット:価格がpresentTrend下限バンドを下回るか、RMIが中立領域に戻り、強気勢力の減退が示唆された場合にエグジット。

- ショートエグジット:価格がpresentTrend上限バンドを上回るか、RMIが中立領域に戻り、弱気勢力の減退が示唆された場合にエグジット。

動的ストップロスの計算式:

- ロングポジション:エントリー後、presentTrend下限バンドをエグジット価格とする

- ショートポジション:エントリー後、presentTrend上限バンドをエグジット価格とする

本戦略の優位性は、RMIのモメンタム判断とpresentTrendのトレンド判断および動的ストップロスを融合し、トレンドに追随しながらリスクを効果的にコントロールできる点にあります。

優位性分析

本戦略には以下の利点があります。

- 多層的判断メカニズムにより、モメンタム指標とトレンド指標を組み合わせ、意思決定の効率を向上

- 動的ストップロスメカニズムにより、市場変動に応じてストップロス位置を調整し、リスクを効果的に管理

- 個人の好みに応じてロング、ショート、または双方向取引を選択可能で、柔軟性が高い

- RMIパラメータを調整可能で、異なる期間の判断に対応

- presentTrendパラメータを調整可能で、戦略の感度を制御可能

リスク分析

本戦略には以下のようなリスクも存在します。

- 売買シグナルが多く、過剰取引による取引コストとスリッページリスクが増加

- 二重判断メカニズムにより、一部の取引機会を逃す可能性

- パラメータを適切に調整し、自身の取引スタイルと一致させる必要あり

- 大きなトレンド方向の判断は依然として人手に委ね、逆張り取引を回避する必要あり

エントリー条件を適度に緩和し、パラメータ組み合わせを最適化し、トレンド判断と組み合わせることで上記リスクを低減できます。

最適化の方向性

本戦略は以下の方向で最適化が可能です。

- ボラティリティ指標と組み合わせ、高ボラティリティ時の誤エントリーを回避

- 出来高指標を追加し、十分な勢力によるエントリーを確保

- 動的ストップロスの幅を最適化し、損失を抑えつつより大きな利益を追求

- 再エントリー条件を追加し、トレンド機会を十分に捕捉

- パラメータ最適化とバックテストを行い、最適パラメータを見つけて収益率を最大化

まとめ

モメンタムトレンド同期戦略は多層的な取引戦略であり、モメンタム指標とトレンド指標の両方を考慮し、正確な判断と優れたリスク管理を特徴とします。本戦略は個人の好みに応じて柔軟に調整可能で、深度最適化後にトレンド捕捉の利点を最大限に発揮できる、推奨に値する取引戦略です。

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

//@version=5- 1