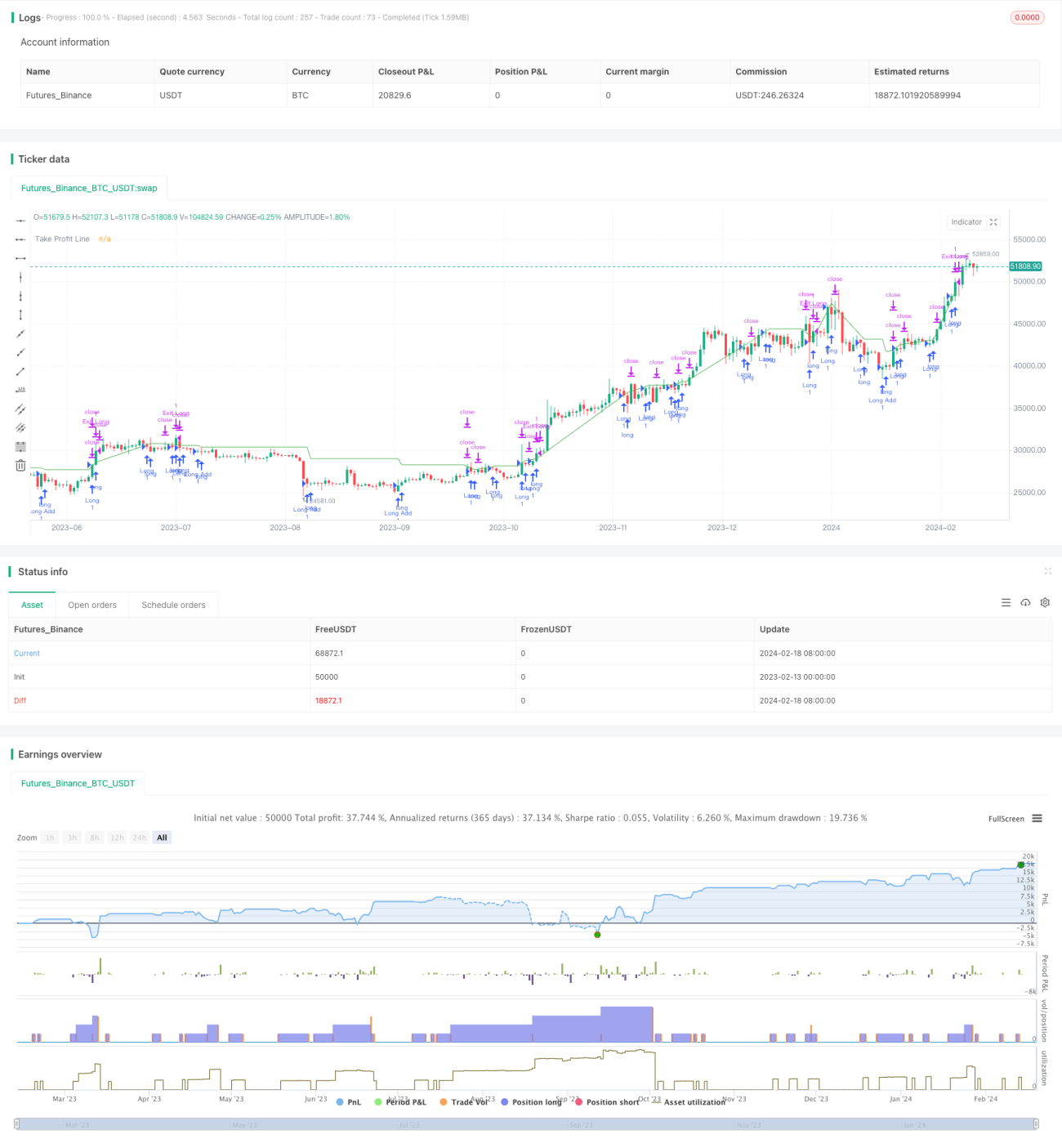

複数のファクターに基づくクオンツ取引戦略

概要

本戦略は、RSI、MACD、OBV、CCI、CMF、MFI、VWMACDなどの複数のテクニカル指標を総合的に活用し、価格と出来高の間のダイバージェンスを検出することで、潜在的なエントリーチャンスを特定します。また、ユーザー定義のディップ検出指標と組み合わせ、高ボラティリティかつ深さまたはVFI条件を満たした場合に取引シグナルを発します。戦略はロングのみで、トレーリングストップを用いてポジションを段階的に増やしながら構築します。

戦略の原理

-

RSI、MACD、OBV、CCI、CMF、MFI、VWMACDなどの指標を計算し、適応線形回帰法を用いて各指標と過去の価格との間のダイバージェンスを検出します。指標が新安値を更新したにもかかわらず価格がそれに追随して新安値を付けていない場合、買いシグナルを発します。

-

ユーザーが入力したボラティリティ閾値と深さ百分率閾値に基づき、VFI指標によるフィルタリングを併用し、高ボラティリティかつ深さテストを満たすローソク足でシグナルを発します。

-

初期ロング後、価格が最後のロング価格から一定割合(設定可能)下落した場合、再度ロングを追加します。

-

トレーリングストップを使用し、設定された利確割合に達した時にポジションを決済します。

優位性分析

-

マルチファクターの組み合わせにより、価格指標と出来高指標を総合的に活用し、シグナルの信頼性を向上させます。

-

適応線形回帰法によるダイバージェンス検出により、主観的な判断を排除します。

-

ボラティリティと深さ/VFI検出指標を組み合わせることで、反転の機会を発見しやすくなります。

-

複数回の追加ロングにより、価格の押し目を活用でき、トレーリング利確で利益を確定しやすくなります。

リスク分析

-

マルチファクターの組み合わせ判断は複雑であり、パラメータ最適化やダイバージェンス認識の効果が実際のパフォーマンスに影響を与える可能性があります。

-

片方向のみのポジション保有はリスクが高く、判断ミスにより大きな損失が発生する可能性があります。

-

繰り返し追加ロングを行うモードでは、損失も拡大するため、ポジション管理に慎重な注意が必要です。

-

取引手数料が実際の利益に与える影響に留意する必要があります。

最適化の方向性

-

異なるパラメータ組み合わせや指標の効果をテストし、最適な設定を選択します。

-

ストップロス戦略を追加し、1回あたりおよび最大損失をコントロールします。

-

双方向取引の機会を検討し、リスクを分散します。

-

機械学習手法を組み合わせてパラメータを自動最適化します。

まとめ

本戦略は複数のテクニカル指標を組み合わせてエントリータイミングを特定し、ユーザー定義条件とVFI指標を用いて偽シグナルをフィルタリングします。価格の押し目を利用して追加ロングを行いトレンドに乗ることで、トレンド内の機会を捉えやすくなっています。一方で、判断ミスや片方向ポジション保有のリスクも存在するため、指標パラメータやストップロス戦略などを適切に最適化し、リスクを低減して利益拡大を図る必要があります。

- 1