DEMAクロストレンド追跡戦略

概要

本戦略は二重指数移動平均線(DEMA)のクロスを取引シグナルとし、トレンドフォロー方式を採用し、自動的にストップロスと利確を設定します。戦略の利点は、取引シグナルが明確で、ストップロス・利確の設定が柔軟であり、リスクを効果的にコントロールできる点です。

戦略の原理

-

短期DEMA(8日)、長期DEMA(24日)、補助線DEMA(設定可能)を計算します。

-

短期線が長期線を上抜けた(ゴールデンクロス)場合に買い、短期線が長期線を下抜けた(デッドクロス)場合に売りを行います。

-

取引シグナルのフィルターを追加し、補助線の当日値が前日より高い場合のみシグナルを生成することで、偽のブレイクアウトを回避します。

-

トレンドフォロー型ストップロス機構を採用し、ストップロスラインは価格の動きに応じて調整され、一部の利益を確保します。

-

同時に固定比率のストップロスと利確を設定し、1回の取引における最大損失と利益を制御します。

戦略の優位性

-

取引シグナルが明確で、エントリーとエグジットのタイミングを判断しやすい。

-

二重DEMAアルゴリズムはより平滑で、過度な最適化を避け、シグナルがより信頼できる。

-

補助線フィルターによりシグナル判断の効果が向上し、偽シグナルを減少させる。

-

トレンドフォロー型ストップロスにより、一部の利益を確保し、リスクを効果的にコントロールできる。

-

固定比率のストップロス・利確を設定することで、1回の取引の最大損失を制御し、リスク範囲を超えるのを防ぐ。

戦略のリスク

-

レンジ相場では頻繁な取引が発生しやすく、ポジションが増加し、戦略に損失をもたらす可能性がある。

-

設定した固定ストップロス比率が大きすぎると、異常な相場で大きなストップロスが発動する可能性がある。

-

DEMAクロスシグナルには遅延が生じるため、急激な相場では高値付近で買いを入れ、損失リスクが増加する。

-

実戦投入時にはスリッページコストが収益性に影響を与えるため、利確・ストップロスのパラメータを調整する必要がある。

戦略の最適化

-

市場状況に応じてDEMAパラメータを調整し、最適なバランスポイントを探す。

-

実戦ではスリッページコストを考慮し、固定ストップロスの範囲を適宜拡大する。

-

MACDなどの他の補助判断指標を追加し、シグナル効果を高めることができる。

-

トレーリングストップロスのステップ値を設定し、ストップロスロジックを最適化する。

まとめ

本戦略はDEMAのトレンド判断能力を活用し、トレンドフォロー機構と組み合わせてリスクをコントロールするもので、トレンド方向を判断する取引戦略体系において非常に典型的な代表例です。全体的に、シグナルが明確で、ストップロス・利確の設定が合理的であり、習得しやすくリスクコントロール可能な取引戦略です。実戦ではスリッページコストの最適化や補助指標の判断を組み合わせることで、良好な投資リターンを得ることができます。

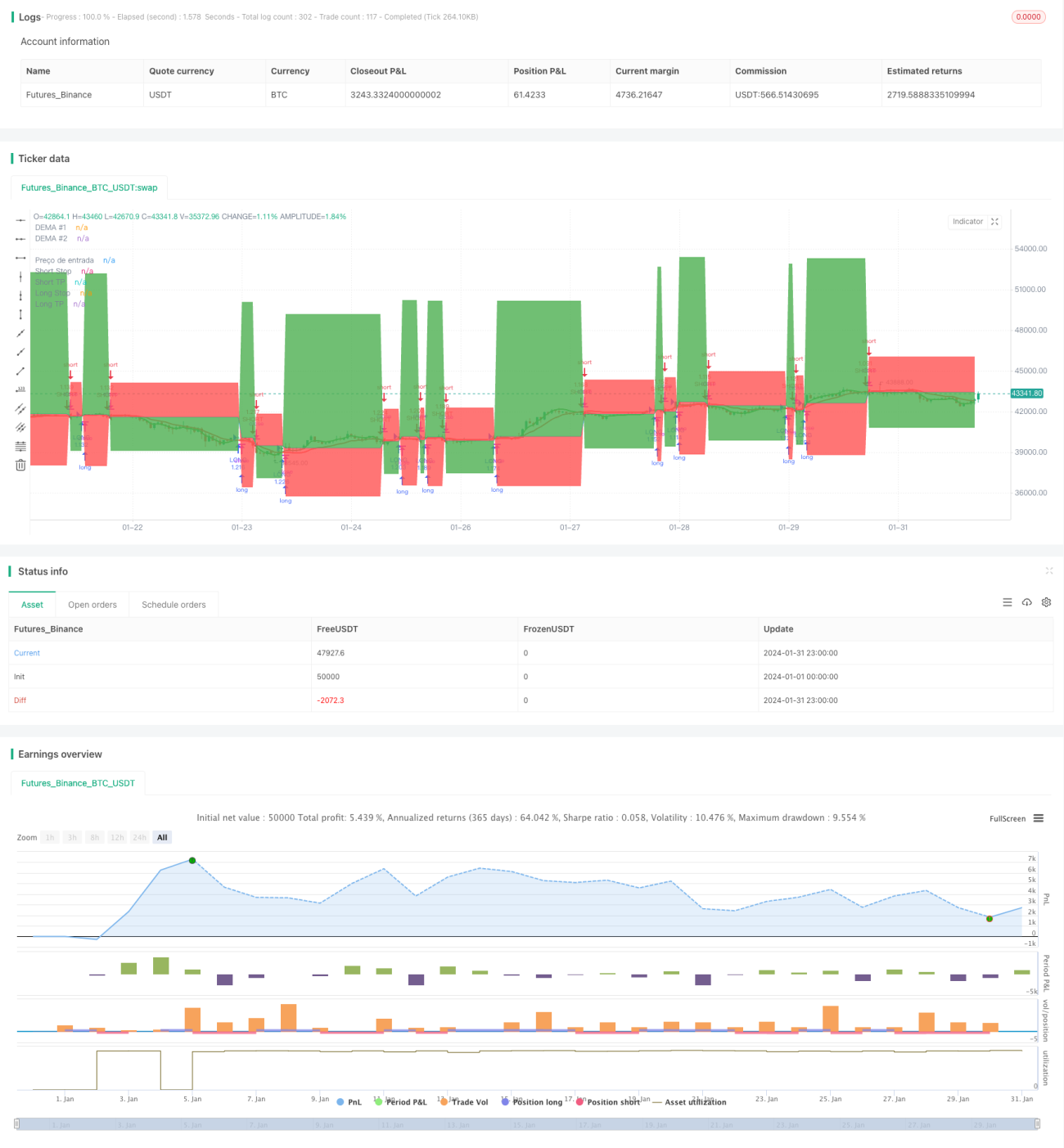

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zeguela

//@version=4

strategy(title="ZEGUELA DEMABOT", commission_value=0.063, commission_type=strategy.commission.percent, initial_capital=100, default_qty_value=90, default_qty_type=strategy.percent_of_equity, overlay=true, process_orders_on_close=true)- 1