月相に基づく双方向取引戦略

1

Follow

1802

Followers

概要

本戦略は月相の変化に基づき、新月で買い(ロング)、満月で売り(ショート)を行い、双方向取引を実現します。

戦略の原理

本戦略ではカスタム関数を使用して月相を計算し、日付から月相の月齢を正確に求めます。月齢が15未満の場合は新月、15以上30未満の場合は満月と判定します。戦略は月相に基づいて買い・売りのシグナルを判断し、新月で買いポジションを建て、満月で売りポジションを建てます。決済時はその逆で、満月で買いポジションを手仕舞い、新月で売りポジションを手仕舞います。

ユーザーは「新月で買い、満月で売り」または「新月で売り、満月で買い」の2つの戦略を選択できます。戦略はブール変数を使用して現在のポジション保有状況を追跡します。シグナルが発生し、それまでポジションがなかった場合は新規エントリーし、シグナルが反転した場合は現在のポジションを決済します。戦略の視覚化では買い・売りのマークが表示されます。

優位性分析

- 月相の周期性を活用し、長期的なトレンドを捉える

- 色や塗りつぶしなど、戦略の表示をカスタマイズ可能

- 双方向取引戦略を選択可能

- エントリー・決済マークの表示により操作が明確

- バックテストの開始時期をカスタマイズでき、戦略を最適化可能

リスク分析

- 月相の周期が長く、短期的なトレンドを捉えられない

- 損失を制限できず、大きな損失が発生する可能性がある

- 固定周期のため、パターン化しやすい

リスク解決方法:

- 他の指標と組み合わせてマルチタイムフレーム取引を実現

- ストップロス機構を追加

- ポジション管理を最適化し、1回の損失が与える影響を低減

最適化の方向性

本戦略は以下の点から最適化が可能です:

- より多くの周期指標を組み合わせて取引シグナルのフィルターとし、戦略の安定性を向上

- ポジション管理モジュールを追加し、ポジションサイズを最適化して1回の損失の影響を低減

- ストップロスモジュールを追加し、損失の拡大を防止

- エントリー・決済条件を最適化し、スリッページを減らし勝率を向上

まとめ

本戦略は月相の周期性を利用し、新月と満月に基づく双方向取引戦略を実現しています。戦略の表示は明確でカスタマイズ性が高く、長期的なトレンドの捉えに適しています。ただし、損失を制限できないためリスクが高く、他の短期指標と組み合わせて使用し、ポジション管理やストップロス管理モジュールを追加することでさらに最適化することを推奨します。

Source

Pine

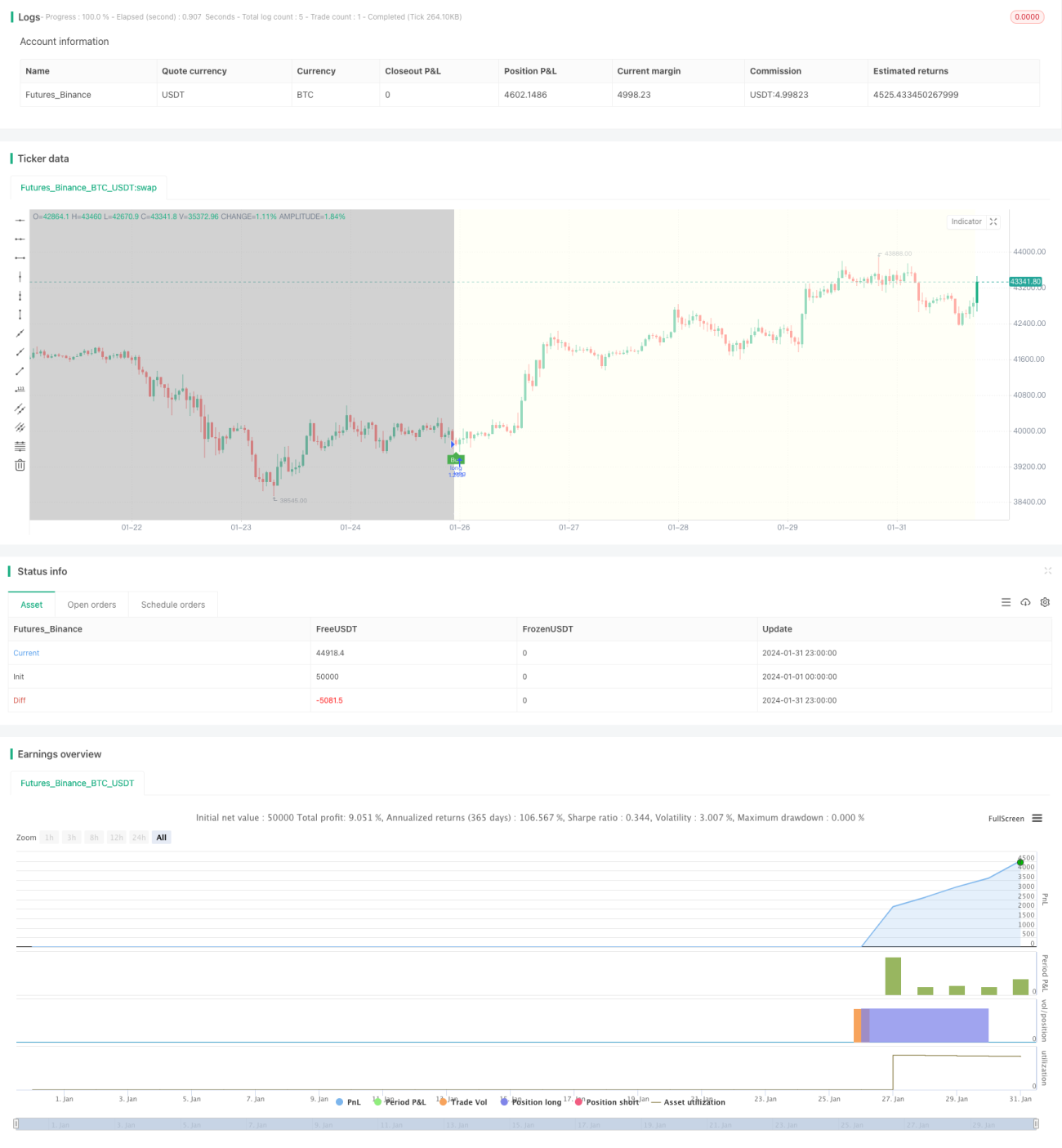

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// ---------------------------© paaax----------------------------

// ---------------- Author1: Pascal Simon (paaax) ----------------Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1