動的チャネル移動平均線トレンド追従戦略

1

Follow

1802

Followers

概要

本戦略は、動的チャネルと移動平均線を用いたトレンドフォローの原理に基づいて設計されています。価格の動的チャネルを計算し、チャネルの上限・下限でトレンド方向を判断し、移動平均線で価格のばらつきをフィルタリングして、取引シグナルを生成します。本戦略は中短期のトレンド取引に適しています。

原理

本戦略は主に以下の原理に基づいています:

-

動的価格チャネルの計算。最高値と最安値からチャネル中心線を計算し、チャネル上限は中心線+価格ばらつきの移動平均、下限は中心線-価格ばらつきの移動平均とします。

-

トレンド方向の判断。価格が上限を上抜けた時を強気、下限を下抜けた時を弱気と定義します。

-

ノイズのフィルタリング。一定期間の価格ばらつき移動平均を使用し、価格のランダムな変動によるノイズを除去します。

-

取引シグナルの生成。強気の場合、その期間の終値が始値より低い時に買いシグナルを生成し、弱気の場合、その期間の終値が始値より高い時に売りシグナルを生成します。

優位性

本戦略には以下の優位性があります:

- 動的チャネルがリアルタイムで価格トレンドを捉えます。

- 移動平均線によるフィルタリングで偽シグナルを低減します。

- トレンド方向とローソク足の実体方向を組み合わせて取引シグナルを生成するため、逆行を回避できます。

リスク

本戦略には以下のリスクも存在します:

- パラメーターの選択が不適切だと過剰最適化につながる可能性があります。

- レンジ相場では誤ったシグナルが発生しやすいです。

- 価格の急激な変動を予測できません。

対応策:

- 厳格なパラメーター選択とテスト。

- フィルター条件を追加し、レンジ相場を識別。

- ストップロス・利確を設定し、リスクを管理。

最適化の方向性

本戦略は以下の点から最適化が可能です:

- 異なる期間パラメーターの安定性をテスト。

- 出来高やボラティリティ指標を追加し、勢いを判断。

- バンドやチャネルなどを組み合わせてエントリーとエグジットを判断。

まとめ

本戦略は動的チャネルと移動平均線によるトレンド判断の考え方を統合し、中短期でのトレンド方向の捉え方に優れたパフォーマンスを示します。ただし一定の限界もあり、さらなるテストと最適化により、より多くの市場状況に適応させる必要があります。

Source

Pine

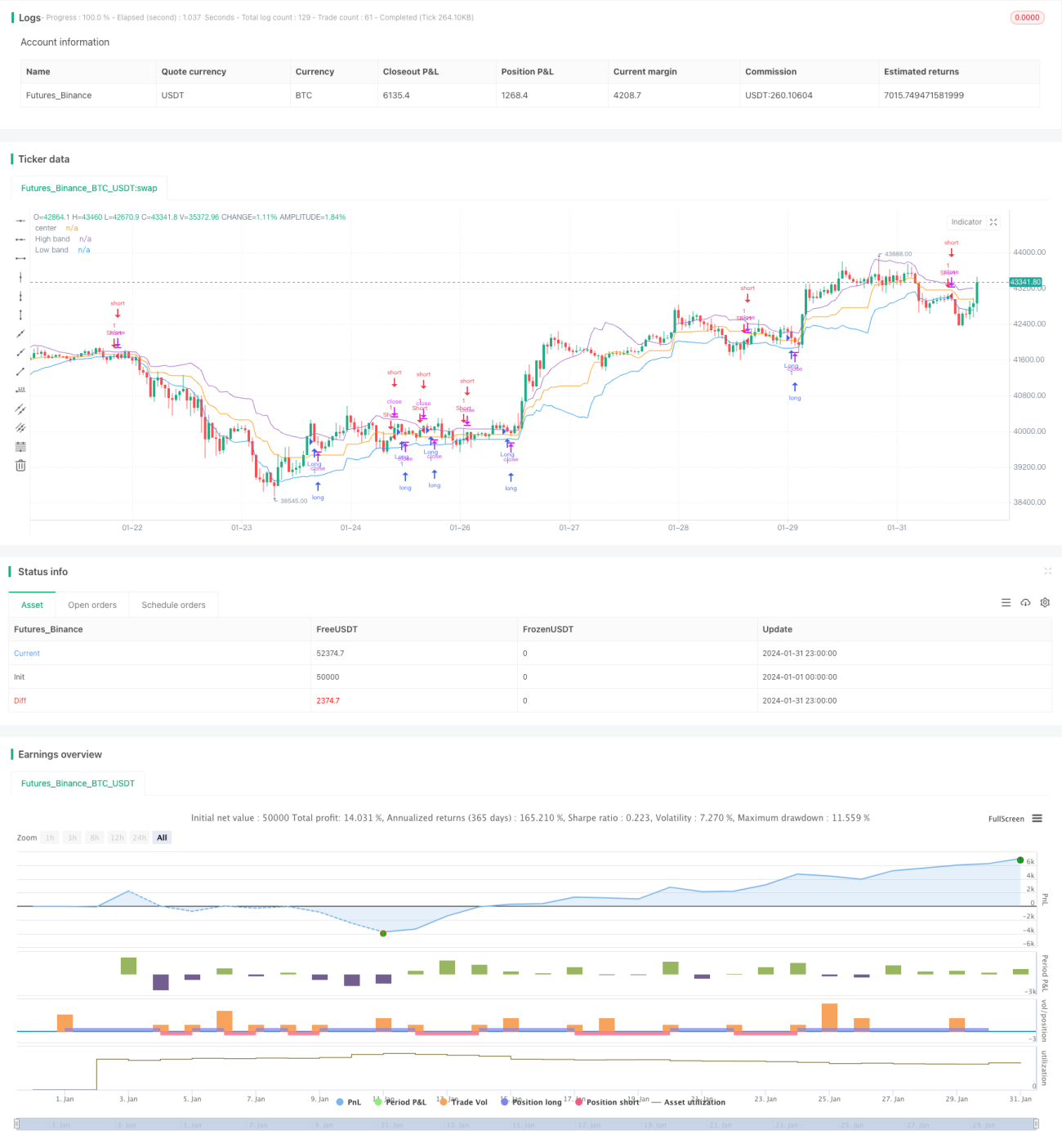

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Strategy v1.0", shorttitle = "NoroBands str 1.0", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1