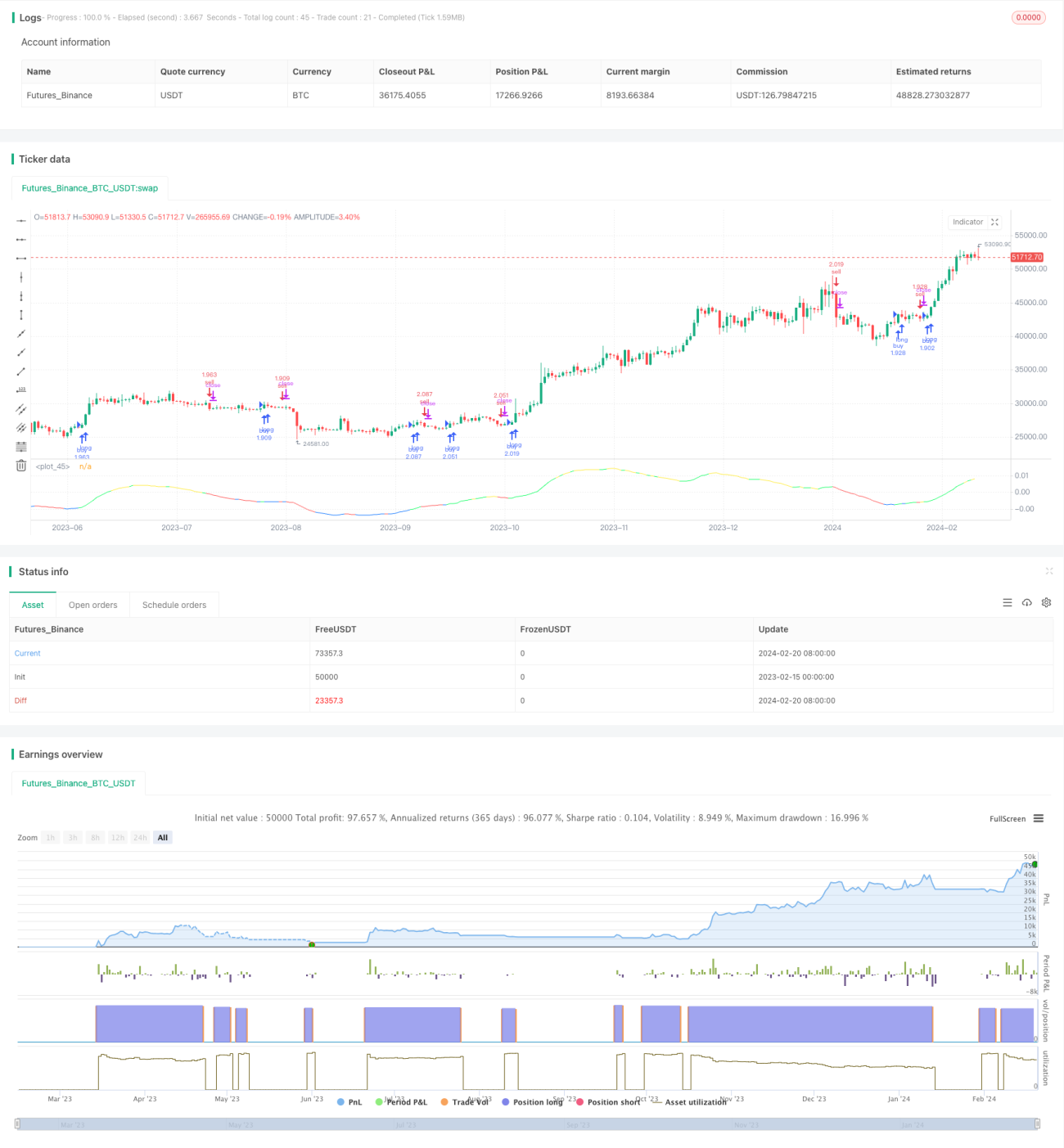

MyQuantトレンド識別戦略

概要

MyQuantトレンド識別戦略は、ビットコインの日足取引に使用する戦略です。本戦略は、価格の移動平均線とその1次導関数・2次導関数を計算することで市場のトレンドを識別し、それに基づいて売買判断を行います。

戦略の原理

本戦略では、まず価格の適応移動平均線(ALMA)とその1次導関数、2次導関数を計算します。1次導関数は価格変化の速度を、2次導関数は価格の曲率を表します。1次導関数と2次導関数の値から、現在が上昇トレンド、下降トレンド、またはレンジ相場かを判断します。さらに株価指標と組み合わせて、買いまたは売りの条件を満たすかどうかを判定します。

具体的には、以下の指標を計算します:

- ALMA:価格の適応移動平均線。期間140、高速係数1.1、シグマ6

- dema:ALMAの1次導関数

- d2ema:demaの1次導関数。価格の2次導関数に相当

- index:dema指標のオシレーター指数

- ind:価格の移動平均線からの乖離度指数

買い条件が満たされた場合、CAUSED.Accumulation/Distribution BandsおよびCaused Exposure Top and Bottom Finderのシグナルに基づいて買い株数を計算します。売り条件が満たされた場合は、全ポジションを売却します。

戦略の優位性

本戦略はトレンドと指標を組み合わせて判断するため、市場のトレンド転換点を効果的に識別できます。価格の1次導関数と2次導関数を用いてトレンドを判断することで、価格のノイズの影響を受けにくくなり、シグナルがより明確になります。一般的な移動平均線戦略と比較して、判断精度が高いなどの利点があります。

リスク分析

本戦略は取引期間の選択とパラメータ調整に非常に敏感です。期間の選択が不適切で重要な価格転換点をカバーできなかった場合、戦略の効果が低下します。指標パラメータの設定が不適切な場合、売買シグナルにノイズが多く含まれるようになり、戦略の収益に影響を及ぼします。また、戦略に予め設定されたストップロス条件も最終的な収益に影響を与えます。

最適化の方向性

本戦略は以下の点からさらに最適化することができます:

- 期間選択ロジックの最適化:バックテストおよび実取引の期間をよりインテリジェントに選択することで改善。

- 指標パラメータの最適化:ALMAやdemaの期間などのパラメータを調整。

- ストップロス条件の追加:最大損失を抑制。

- 異なる暗号通貨での効果を評価し、最も良好なパフォーマンスを示す銘柄を選択。

まとめ

MyQuantトレンド識別戦略は、価格の適応移動平均線の1次および2次導関数を計算することで、ビットコインの市場トレンドを効果的に識別し、それに応じた売買判断を行います。本戦略は複数の指標を組み合わせて判断することで、シグナルが過度なノイズに影響されることを防ぎます。さらなる期間とパラメータの最適化により、本戦略の効果はさらに向上する可能性があります。

- 1