ボリンジャーバンドとMACDに基づく量的取引戦略

概要

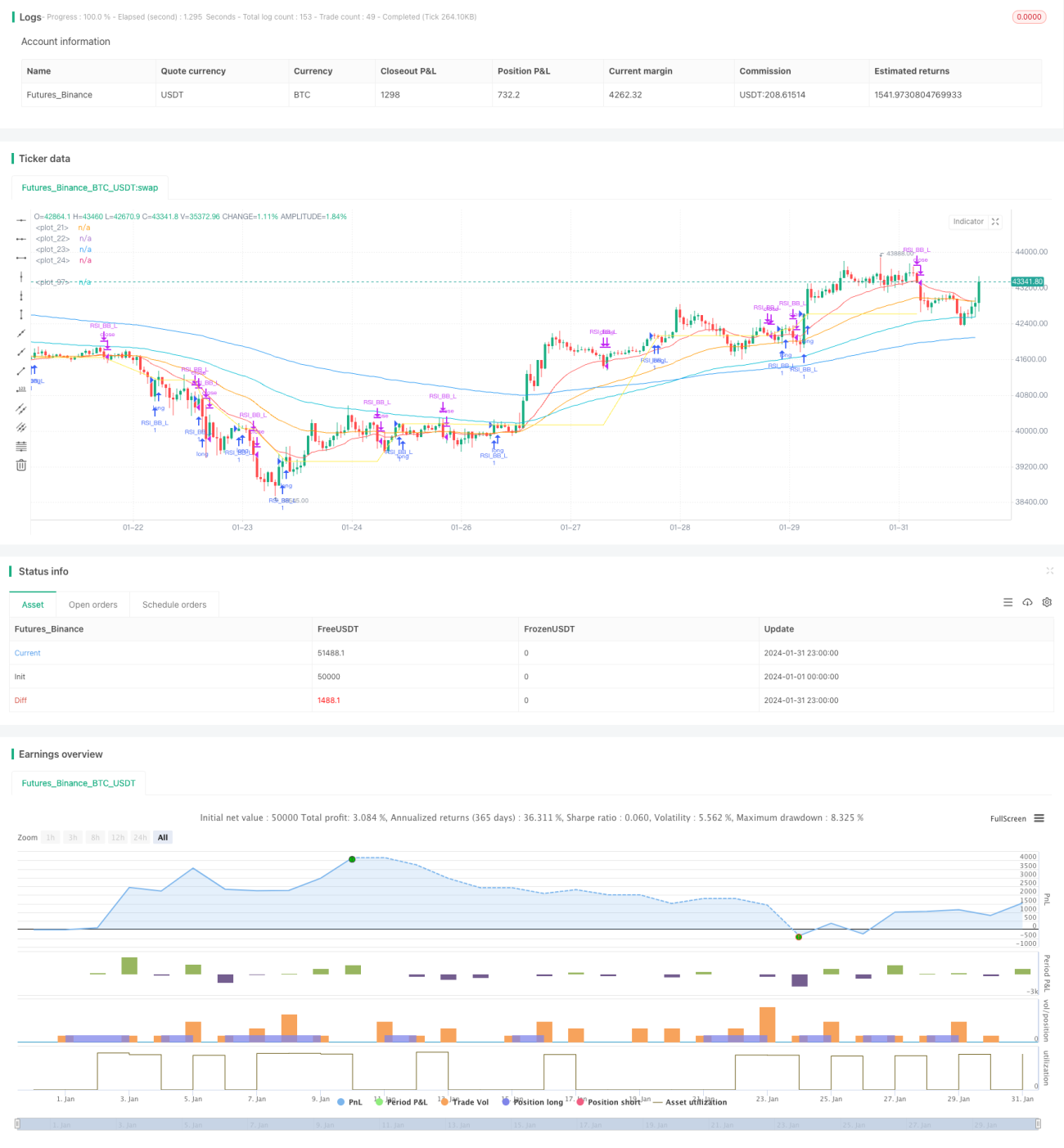

この戦略は、ボリンジャーバンドとMACD指標に基づく定量取引戦略です。ボリンジャーバンドのブレイクアウト取引とMACDのトレンドフォローを組み合わせることで、取引シグナルの質を高めることを目的としています。

戦略の原理

この戦略は主にボリンジャーバンド指標とMACD指標を用いて取引シグナルを判断します。

ボリンジャーバンドは中央線、上限線、下限線で構成されます。価格が下限線を下回ると買いシグナルが生成され、価格が上限線を上回ると売りシグナルが生成されます。本戦略ではボリンジャーバンドのブレイクアウト原理を利用して、より強いブレイクアウトシグナルを特定します。

MACD指標は短期と長期の移動平均線の関係を反映し、差し引き線とシグナル線のゴールデンクロス・デッドクロスにより売買タイミングを判断します。本戦略ではMACD指標を併用してボリンジャーバンドのシグナルをフィルタリングし、差し引き線がシグナル線を上回ったときに効果的な買いシグナルを生成します。

全体として、本戦略はボリンジャーバンドのトレンドフォローとMACDの移動平均線の利点を組み合わせ、強いトレンドの中でより大きな値動きを捉えることを目指しています。

戦略の優位性

-

ボリンジャーバンドとMACD指標を組み合わせることで、取引シグナルがより信頼性高くなります。

-

トレンド相場では、ボリンジャーバンドのトレンドフォローとMACDの移動平均線クロスにより強いエントリーシグナルが得られます。

-

二重の指標判断により、偽シグナルを効果的にフィルタリングし、取引リスクを低減します。

-

戦略パラメータの最適化の余地が大きく、異なる銘柄や期間に応じて調整可能です。

戦略のリスク

-

レンジ相場では、ボリンジャーバンドとMACDが発生させる取引シグナルが頻発し、スキャルピングリスクが生じる可能性があります。

-

MACD指標が低水準で3回目のゴールデンクロスを発生させた場合、反転下落リスクに直面する可能性があります。

-

戦略で多くの指標を使用しているため、パラメータ最適化や戦略テストが難しくなります。

上記リスクに対しては、適切な保有期間の調整、ストップロスラインの設定、パラメータ最適化などの手法で管理することが可能です。

戦略の最適化方向

-

より長い期間のボリンジャーバンドパラメータをテストし、取引頻度を低下させる。

-

MACDの短期・長期移動平均線のパラメータを最適化し、指標の感度を高める。

-

KDJやRSIなど他の指標を追加し、シグナルの品質を向上させる。

-

動的なストップロスを設定し、自動で損切りを行い、1回の取引リスクを制御する。

まとめ

本戦略はボリンジャーバンドのブレイクアウト取引とMACD指標によるフィルタリングを統合しており、理論上は高品質な取引シグナルを生成できます。パラメータ最適化とリスク管理手法により、良好なバックテスト結果が期待できます。ただし、いかなる戦略も損失を完全に回避できるわけではないため、実際の取引効果を慎重に評価する必要があります。

- 1