1

Follow

1802

Followers

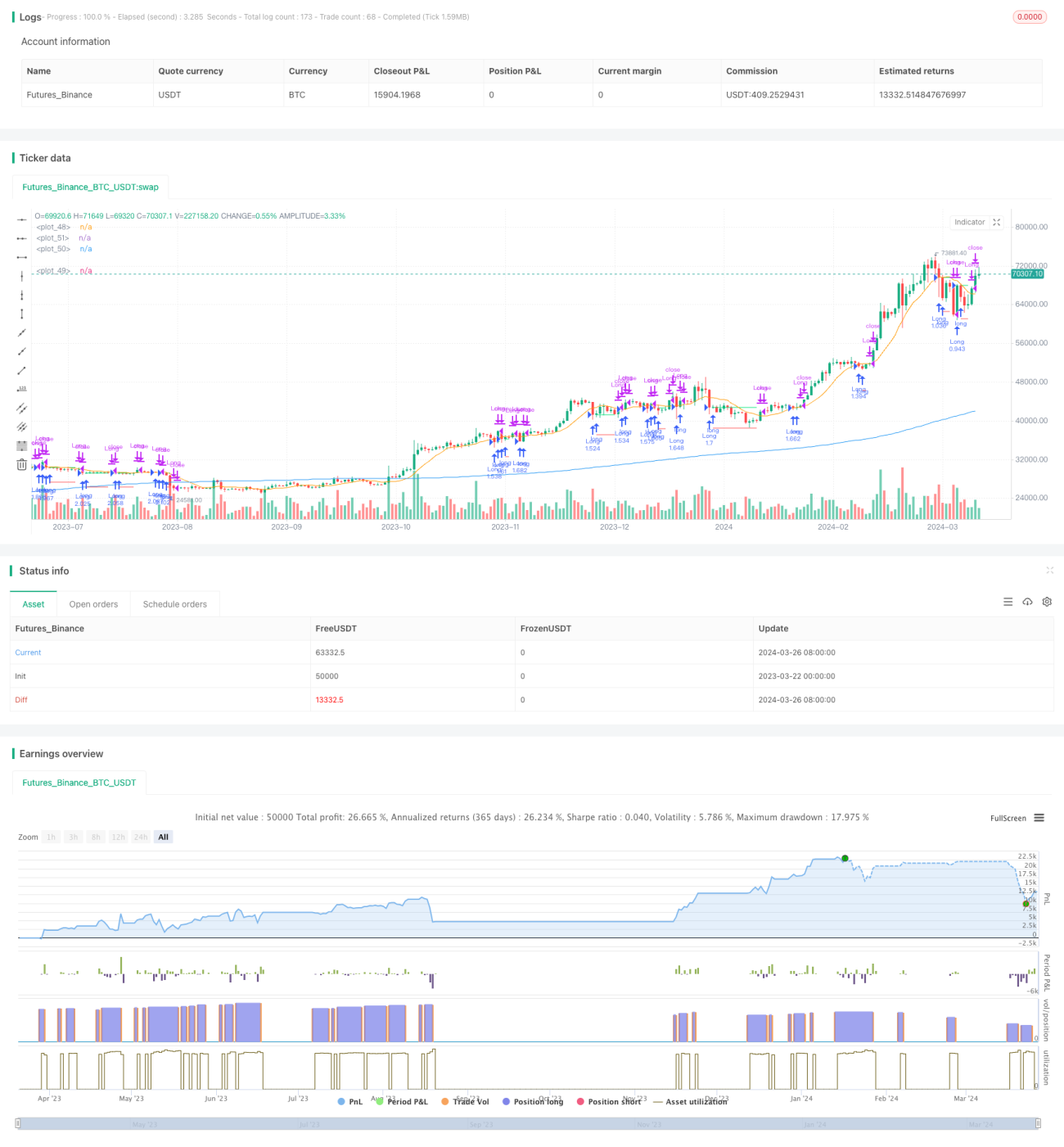

概要

本戦略の主な考え方は、異なる期間の2本の移動平均線を利用して、市場の調整後の反発機会を捉えることです。価格が長期移動平均線よりも上にあり、短期移動平均線に向かって調整した場合、戦略はロングポジションを建て、価格が再び短期移動平均線を上回るか、またはストップロス価格に達したときにポジションをクローズします。この戦略は、トレンドの中で調整買いの機会を探し、トレンド相場での利益獲得を目指します。

戦略の原理

- 異なる期間の2本の移動平均線(MA1とMA2)を計算します。MA1は長期移動平均線、MA2は短期移動平均線です。

- 終値がMA1よりも上にあり、かつMA2よりも下にある場合、かつ現在ポジションがない場合、かつ現在時刻が設定された取引時間範囲内にある場合、戦略はロングポジションを建てます。

- 建て値buyPriceを記録し、ストップロス価格stopPrice(建て値からi_stopPercent%下落した価格)を計算します。

- 終値が再びMA2を上回り、かつi_lowerCloseがfalseの場合、または終値がストップロス価格stopPriceを下回った場合、戦略はポジションをクローズします。

- i_lowerCloseがtrueの場合、終値がMA2よりも高く、かつ前のローソク足の終値がMA2よりも低いときにポジションをクローズします。

戦略の優位性

- トレンドフォロー:価格と長期移動平均線の位置関係を判断することで、現在の全体的なトレンドを把握し、トレンド内でのエントリー機会を探します。

- 調整買い:上昇トレンドの中で、価格が短期移動平均線まで調整した買い機会を捉えることで、買いポジションのコストパフォーマンスを向上させます。

- ストップロス保護:ストップロス価格を設定し、価格が逆方向に一定の幅動いた場合に自動的にポジションをクローズし、下落リスクを効果的にコントロールします。

- 柔軟なパラメータ:ユーザーは自分の好みに応じて、移動平均期間、ストップロス率、前のローソク足の終値が短期移動平均線を下回った場合にポジションをクローズするかどうかなどのパラメータを柔軟に設定できます。

戦略のリスク

- パラメータ最適化:異なるパラメータ設定が戦略のパフォーマンスに大きな影響を与えるため、さまざまな市場環境でパラメータ最適化とバックテストを行い、最適なパラメータの組み合わせを見つける必要があります。

- レンジ相場:レンジ相場では、価格が長期・短期移動平均線の間で頻繁に変動するため、戦略が頻繁にポジションを建てたりクローズしたりし、取引コストが増加する可能性があります。

- トレンド転換:市場のトレンドが転換した場合、戦略は連続して損失を出す可能性があります。この場合は、他の指標やシグナルを組み合わせてトレンド転換を判断し、戦略を適時に調整する必要があります。

- ブラックスワンイベント:予測不可能な重大な突発事象が発生した場合、価格が急激に変動し、ストップロスが発動した後に戦略が大きな損失を被る可能性があります。

戦略の改善方向

- トレンド判断:ポジションを建てる前に、ADXなどのトレンド判断指標をさらに導入し、現在のトレンドの強さと方向を確認し、エントリーシグナルの精度を向上させます。

- 動的ストップロス:価格のボラティリティやATRなどの指標に基づいてストップロス価格を動的に調整し、価格変動が大きいときはストップロスを適度に緩め、価格変動が小さいときはストップロスを引き締めます。

- ポジション管理:市場のトレンドの強さや価格のボラティリティなどの要因に基づいて、毎回のポジションサイズを動的に調整し、トレンドが強くボラティリティが適度な場合はポジションを増やし、トレンドが弱いまたはボラティリティが高すぎる場合はポジションを減らします。

- ロング・ショートのヘッジ:ロングとショートの両方のシグナルを同時に監視し、異なる市場やサイクルでヘッジポジションを建てることで、戦略全体のリスクを低減することを検討します。

まとめ

移動平均調整フォロースルー戦略は、異なる期間の2本の移動平均線の相対的な位置関係を利用して、上昇トレンドにおける価格の調整買いの機会を捉えます。この戦略はトレンド市場に適しており、適切なパラメータとストップロスを設定することで、トレンド相場で安定した収益を得ることができます。ただし、レンジ相場やトレンド転換時には、この戦略は一定のリスクに直面します。より多くの指標を導入したり、ポジション管理や動的ストップロスを最適化したりすることで、戦略のパフォーマンスと安定性をさらに向上させることができます。

Source

Pine

/*backtest

start: 2023-03-22 00:00:00

end: 2024-03-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © contapessoal_ivan

// @version=5

strategy("Pullback Strategy", Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1