ガウスチャネル適応移動平均線戦略

1

Follow

1802

Followers

概要

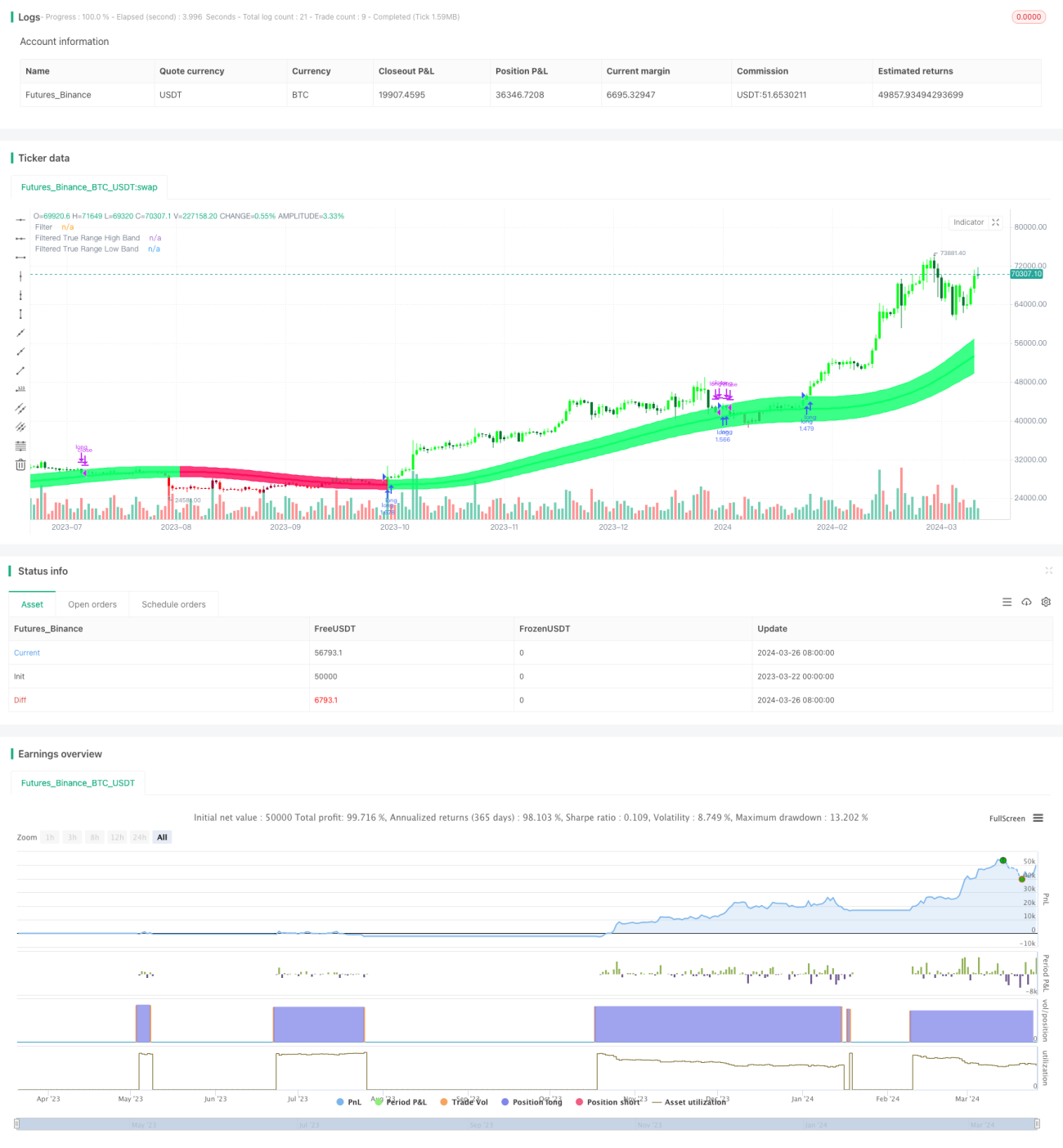

ガウスチャネル適応移動平均線戦略は、ガウスフィルタリング技術と適応パラメータ設定を活用した定量取引戦略です。本戦略はJohn Ehlersが提唱したガウスフィルター理論に基づき、価格データに対して複数回の指数移動平均計算を実行することで、平滑化かつ適応性のある取引シグナルを生成します。戦略の核は動的に調整される価格チャネルの構築であり、上下のバンドはガウスフィルタリング後の価格に真の変動幅を加減して得られます。価格が上バンドを突破した場合に買い、下バンドを突破した場合に売りを行います。同時に、この戦略は期間パラメータを導入しており、戦略の実行開始・終了時間を柔軟に設定できるため、実用性が向上しています。

戦略の原理

ガウスチャネル適応移動平均線戦略の原理は以下の通りです:

- 価格のガウスフィルタリング値を計算します。ユーザーが設定したサンプリング周期と極点数に基づいてBetaおよびAlphaパラメータを算出し、価格データに対して段階的にガウスフィルタリングを施し、平滑化された価格系列を取得します。

- 真の変動幅のガウスフィルタリング値を計算します。価格の真の変動幅に対して同様のガウスフィルタリング処理を行い、平滑化された変動幅系列を取得します。

- ガウスチャネルを構築します。ガウスフィルタリング後の価格を中央バンドとし、上バンドは中央バンドに真の変動幅とユーザー設定の倍数の積を加えた値、下バンドは中央バンドからその値を引いた値とすることで、動的なチャネルを形成します。

- 取引シグナルを生成します。価格がチャネルの上バンドを上方に突破した場合に買いシグナルが発生し、価格がチャネルの下バンドを下方に突破した場合に売りシグナルが発生します。

- 期間パラメータを導入します。ユーザーは戦略の実行開始・終了時間を設定でき、その時間範囲内でのみ戦略が取引シグナルに基づいて操作を行います。

優位性分析

ガウスチャネル適応移動平均線戦略には以下の利点があります:

- 適応性が高い。動的に調整されるパラメータを採用しており、異なる市場状況や取引銘柄に適応できるため、頻繁な手動調整が不要です。

- トレンド追従性が良好。価格チャネルを構築することで、市場のトレンドを効果的に捉え追従し、レンジ相場における偽シグナルを回避できます。

- 平滑性が高い。ガウスフィルタリング技術を用いて価格データを複数回平滑化することで、市場ノイズの大部分を除去し、取引シグナルの信頼性を高めます。

- 柔軟性が高い。ユーザーは必要に応じて、サンプリング周期、極点数、変動倍率などの戦略パラメータを調整し、戦略のパフォーマンスを最適化できます。

- 実用性が高い。期間パラメータが導入されているため、指定した時間範囲内で戦略を実行でき、実運用やバックテスト研究に便利です。

リスク分析

ガウスチャネル適応移動平均線戦略には多くの利点があるものの、以下のリスクも存在します:

- パラメータ設定リスク。不適切なパラメータ設定により戦略が機能しなかったり、パフォーマンスが低下する可能性があるため、実運用において繰り返しテストと最適化が必要です。

- 突発的イベントリスク。特定の重大な突発イベントに対して、戦略が適時正しい反応を示せず損失を被る可能性があります。

- オーバーフィッティングリスク。パラメータ設定が過去のデータに過度に適合している場合、将来のパフォーマンスが低下するリスクがあり、サンプル内外のパフォーマンスを考慮する必要があります。

- 逆行リスク。本戦略は主にトレンド相場に適しており、レンジ相場で頻繁に取引を行うと大きな逆行リスクに直面する可能性があります。

最適化の方向性

ガウスチャネル適応移動平均線戦略の最適化の方向性は以下の通りです:

- 動的パラメータ最適化。機械学習などの技術を導入し、戦略パラメータの自動最適化と動的調整を実現することで適応性を高めます。

- マルチファクター統合。他の有効なテクニカル指標やファクターをガウスチャネルと組み合わせることで、より頑健な取引シグナルを形成します。

- ポジション管理の最適化。戦略に合理的なポジション管理および資金管理ルールを追加し、ドローダウンとリスクを抑制します。

- 複数銘柄の連携。戦略を複数の異なる取引銘柄に拡張し、資産配分と相関分析によってリスクを分散します。

まとめ

ガウスチャネル適応移動平均線戦略は、ガウスフィルタリングと適応パラメータに基づく定量取引戦略であり、動的な価格チャネルを構築することで平滑で信頼性の高い取引シグナルを生成します。本戦略は適応性が高く、トレンド追従性に優れ、平滑性が高く、柔軟性と実用性が高いという利点を持つ一方、パラメータ設定、突発的イベント、オーバーフィッティング、逆行などのリスクも抱えています。今後は動的パラメータ最適化、マルチファクター統合、ポジション管理の最適化、複数銘柄の連携などの面から戦略をさらに改良・向上させることが期待されます。

Source

Pine

/*backtest

start: 2023-03-22 00:00:00

end: 2024-03-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Gaussian Channel Strategy v1.0", overlay=true, calc_on_every_tick=false, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.1)

// Date condition inputsStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1