ボリンジャーバンドとDCAを組み合わせた高頻度取引戦略

1

Follow

1802

Followers

概要

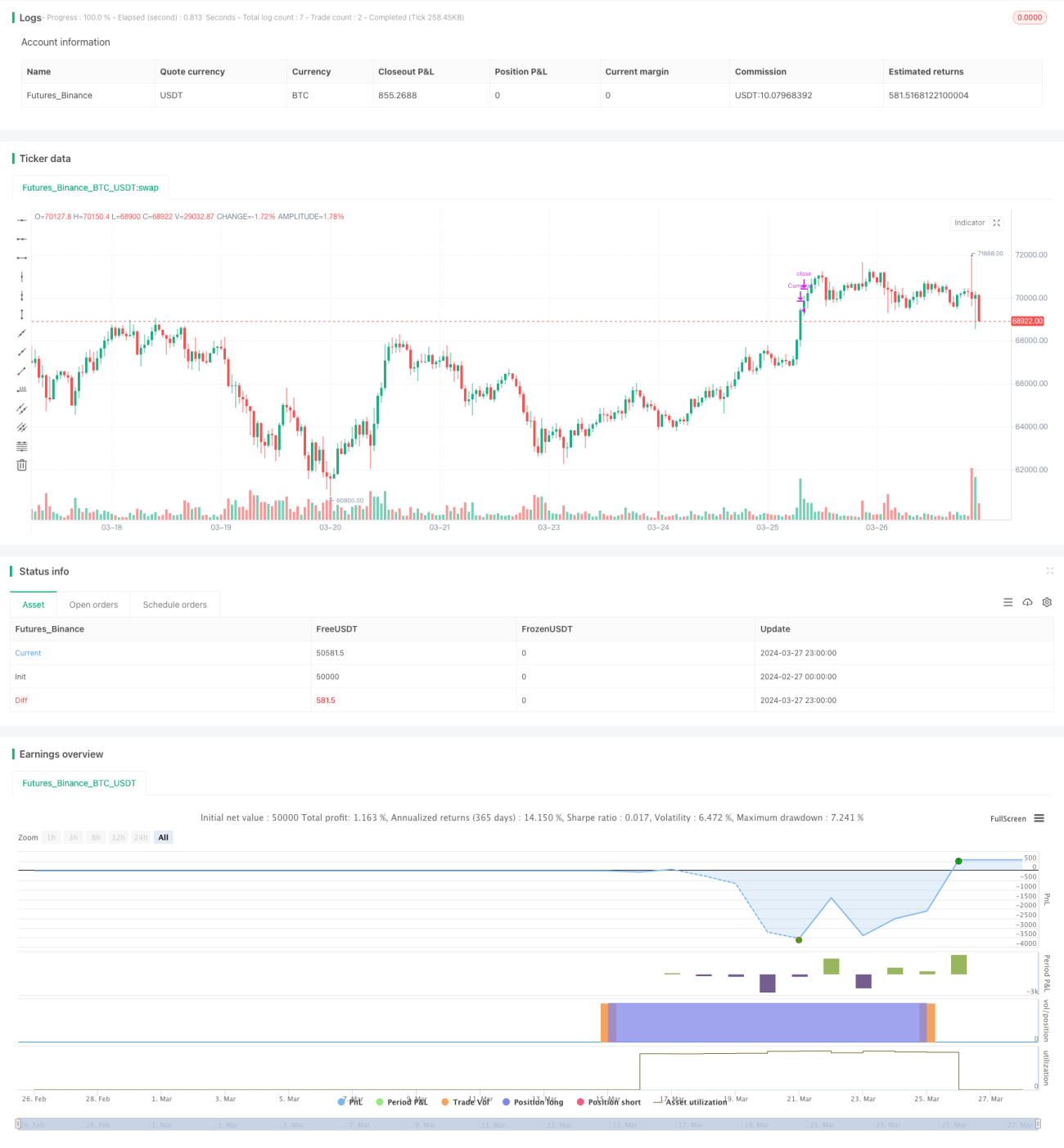

本戦略は「DCA Booster (1 minute)」と称し、1分足の時間枠で動作する高頻度取引戦略です。この戦略はボリンジャーバンドとDCA(ドルコスト平均法)の2つのテクニックを組み合わせ、市場の変動を利用して複数回の売買を行い、利益を得ようとします。主な考え方は、価格が2期間連続でボリンジャーバンドの下限を下回った場合に、DCA方式で分割してポジションを構築し、価格がボリンジャーバンドの上限を上抜けた場合に全ポジションを決済するというものです。また、この戦略はピラミッディング・アプローチを許容しており、価格が下落し続ける場合には追加でポジションを増やします。

戦略の原理

- ボリンジャーバンドの計算:単純移動平均と標準偏差を用いてボリンジャーバンドの上限・下限を算出します。

- DCAパラメータの設定:固定金額を複数に分割し、各ポジション構築時の資金量とします。

- ポジション構築条件:終値が2期間連続でボリンジャーバンドの下限を下回った場合にポジション構築を開始します。価格が下限を下回り続ける限り、最大5つのポジションを保有できます。

- 決済条件:価格がボリンジャーバンドの上限を上抜けた場合に全ポジションを決済します。

- ピラミッディングによる追加ポジション:価格が下落し続ける場合に追加でポジションを構築し、最大5つまで保有できます。

- ポジション管理:各ポジションの構築状況を記録し、決済条件が満たされた時に対応するポジションを決済します。

戦略のメリット

- ボリンジャーバンドとDCAの2つのテクニックを組み合わせることで、市場の変動を効果的に捉え、購入コストを低減できます。

- ピラミッディングによる追加ポジションを許容するため、価格が下落し続ける場合にもポジションを増やし、利益獲得の機会を増やすことができます。

- 決済条件がシンプルで明確であり、迅速に利益を確定できます。

- 1分足などの短い時間枠での使用に適しており、高頻度取引が可能です。

戦略のリスク

- 市場が激しく変動し、価格が急激にボリンジャーバンドの上限を突破した場合、戦略が決済に間に合わず損失が発生する可能性があります。

- ピラミッディングによる追加ポジションは、価格が下落し続ける場合に過度なエクスポージャーを引き起こし、リスクを増大させる可能性があります。

- レンジ相場ではパフォーマンスが低下する可能性があります。頻繁な売買により取引コストが高くなるためです。

戦略の最適化方向性

- 決済条件にストップロスを組み込み、1回の取引における最大損失を制御することを検討できます。

- ピラミッディングのロジックを最適化し、例えば価格下落の幅に応じて追加ポジションの量を調整することで過度なエクスポージャーを回避できます。

- RSIやMACDなどの他の指標と組み合わせ、エントリーとエグジットの精度を向上させることができます。

- ボリンジャーバンドの期間や標準偏差の倍率などのパラメータを最適化し、様々な市場状況に適応させることができます。

まとめ

「DCA Booster (1 minute)」はボリンジャーバンドとDCAを組み合わせた高頻度取引戦略です。価格がボリンジャーバンドの下限を下回った時点で分割してポジションを構築し、価格が上限を上抜けた時点で全ポジションを決済することで、市場の変動を捉えて利益を得ようとします。この戦略はピラミッディングによる追加ポジションを許容しますが、同時に市場の激変動や過度なエクスポージャーのリスクに直面します。ストップロスの導入、追加ポジションのロジック最適化、他の指標との組み合わせ、パラメータ最適化などの方法によって、さらに戦略のパフォーマンスを改善することができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1