1

Follow

1802

Followers

概要

本戦略は、複数の移動平均線(VWMA)、平均方向性指数(ADX)、および方向性指標(DMI)を活用し、ビットコイン市場におけるロングポジションの機会を捉えます。価格のモメンタム、トレンド方向、取引量など複数のテクニカル指標を組み合わせることで、上昇トレンドが強く、モメンタムが十分なエントリーポイントを見つけつつ、リスクを厳格に管理することを目的としています。

戦略の原理

- 9日と14日のVWMAを使用してロングトレンドを判断し、短期移動平均線が長期移動平均線を上抜けた場合にロングシグナルを発生させます。

- 89日最高価格と最低価格のVWMAから構築された適応型移動平均線をトレンドフィルターとして導入し、終値または始値がこの線を上回っている場合のみポジションを検討します。

- ADXとDMIによるトレンドの強さの確認を行い、ADXが18より大きく、かつ+DIと-DIの差が15より大きい場合にのみ、トレンドが十分に強いと判断します。

- 取引量のパーセンタイル関数を利用し、取引量が60%~95%の範囲にあるバーをフィルタリングし、低取引量の時間帯を避けます。

- ストップロスは前のローソク足の高値の0.96~0.99倍に設定し、時間枠が大きくなるにつれて減少させることでリスクを管理します。

- 所定の保有時間に達したか、価格が適応型移動平均線を下回った場合にポジションをクローズします。

優位性分析

- 複数のテクニカル指標を組み合わせ、トレンド、モメンタム、取引量など複数の次元から市場の状態を評価するため、シグナルの信頼性が向上します。

- 適応型移動平均線と取引量のフィルタリングメカニズムにより、偽のシグナルを効果的に除去し、無駄な取引を減らします。

- 厳格なストップロス設定と保有時間制限により、戦略全体のリスクエクスポージャーを大幅に低減します。

- コードはモジュール化されており、可読性とメンテナンス性が高く、さらなる最適化や拡張が容易です。

リスク分析

- 相場がレンジ相場やトレンドが明確でない場合、本戦略は多くの偽のシグナルを発生させる可能性があります。

- ストップロスが比較的近い位置にあるため、相場の変動が大きい場合、早期にストップロスがトリガーされ、損失が拡大する恐れがあります。

- マクロ経済情勢や大きなイベントに対する考慮が欠けており、「ブラックスワン」イベントに直面すると機能しなくなる可能性があります。

- パラメータ設定が比較的固定されており、適応性に欠けるため、市場環境が異なるとパフォーマンスが不安定になる可能性があります。

最適化の方向性

- 相対力指数(RSI)やボリンジャーバンドなど、市場環境をより詳細に描写する指標を追加し、シグナルの信頼性を高めます。

- ストップロスの位置を動的に最適化する(例えばATRやパーセンテージストップロスを採用)ことで、異なる市場のボラティリティ状況に対応します。

- マクロ経済データやセンチメント分析を組み合わせ、戦略のリスク管理モジュールを強化します。

- 機械学習アルゴリズムを使用してパラメータを自動最適化し、戦略の適応性と安定性を高めます。

まとめ

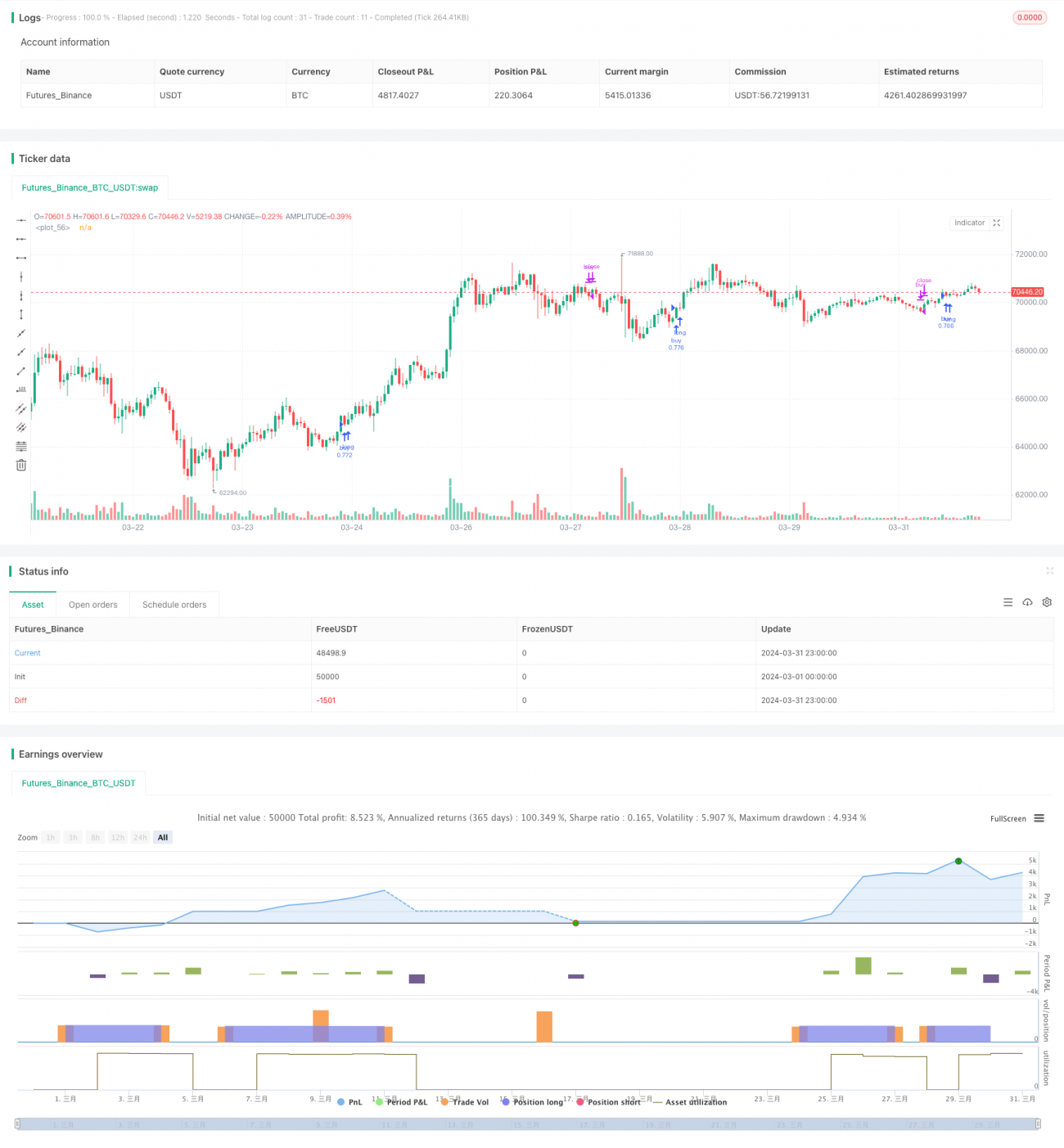

VWMA-ADX ビットコイン・ロング戦略は、価格トレンド、モメンタム、取引量など複数のテクニカル指標を総合的に考慮することで、ビットコイン市場における上昇の機会を効果的に捉えることができます。また、厳格なリスク管理と明確なポジションクローズ条件により、リスクは適切にコントロールされています。ただし、市場環境の変化への適応性不足やストップロス戦略の改善の余地など、いくつかの限界も存在します。今後はシグナルの信頼性、リスク管理、パラメータ最適化などの面から、戦略の堅牢性と収益性をさらに向上させることが可能です。総じて、VWMA-ADX ビットコイン・ロング戦略は、モメンタムとトレンドに基づいた体系的な取引アプローチを投資家に提供しており、さらなる探求と改良に値します。

Source

Pine

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Q_D_Nam_N_96

//@version=5Related strategies

Comment

All comments (1)

- 1