AlphaTradingBot 取引戦略

1

Follow

1802

Followers

概要

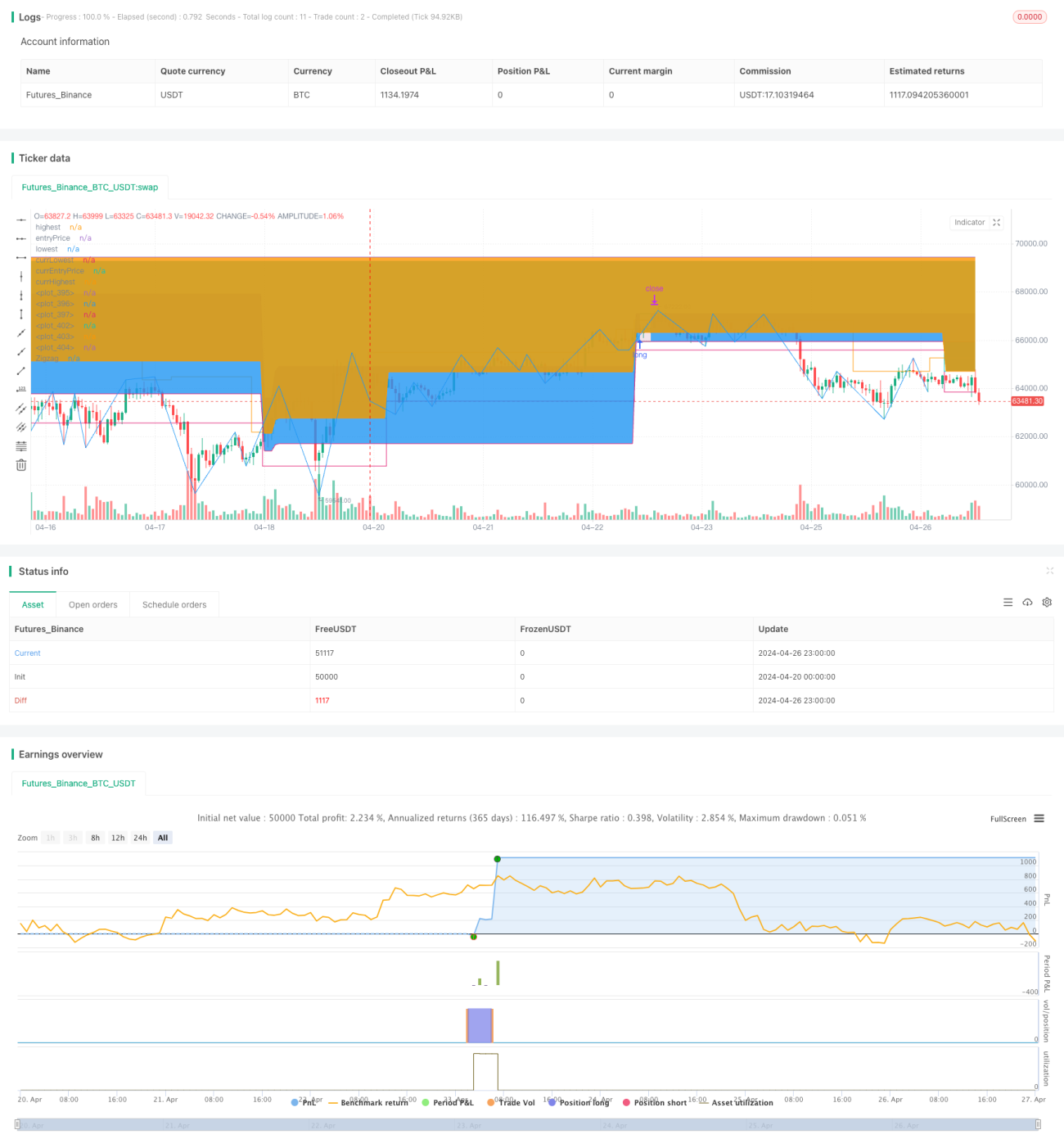

AlphaTradingBotは、Zigzag指標とフィボナッチ数列に基づいた日中取引戦略です。この戦略は、市場の高値(HH)と安値(LL)を識別してトレンドを判断し、フィボナッチ・リトレースメントとエクスパンションを組み合わせてエントリーポイント、利確、ストップロスを設定します。この戦略は設定された日付範囲内でのみ稼働し、ロングとショートをそれぞれ行うことができ、一定のトレンド把握能力とリスクリワード比の管理を備えています。

戦略の原理

- Zigzag指標を用いて市場の高値(HH)、安値(LL)、より高い安値(HL)、より低い高値(LH)を識別します。

- HHが出現した場合は上昇トレンドの開始とみなし、ロング機会の探索を開始します。LLが出現した場合は下降トレンドの開始とみなし、ショート機会の探索を開始します。

- 上昇トレンドにおいてHLが出現した場合、HLとその前のLLで形成されるレンジをロングのフィボナッチ・リトレースメント区間とします。価格が前の高値を突破した場合、リトレースメント23.6%~38.2%(設定可能)の範囲でロングエントリーし、ストップロスはリトレースメント61.8%に設定し、利確はRR値(設定可能)で計算します。

- 下降トレンドにおいてLHが出現した場合、LHとその前のHHで形成されるレンジをショートのフィボナッチ・リトレースメント区間とします。価格が前の安値を突破した場合、リトレースメント61.8%~76.4%(設定可能)の範囲でショートエントリーし、ストップロスはリトレースメント38.2%に設定し、利確はRR値(設定可能)で計算します。

- 注文管理:各シグナルにつき1回のみエントリーし、そのポジションが決済されるまで新たなエントリーは行いません。1回の損失が口座総額のX%(設定可能)に達した場合、戦略は停止します。

優位性分析

- トレンド追従能力が高い。Zigzagにより効果的にトレンドを識別し、トレンド初期段階で介入できます。

- リトレースメントのロジックが明確。フィボナッチ・リトレースメントを用いてエントリー範囲を設定し、トレンドのリトレース時に介入するため、勝率が比較的高くなります。

- リスクを管理可能。1回あたりの最大損失比率を設定することで各取引のリスクをコントロールし、厳格なストップロス制度により全体リスクも管理可能です。

- リスクリワード比を最適化可能。市場特性や個人の好みに応じてRR値を調整し、戦略のリスクリワード比を最適化できます。

リスク分析

- 頻繁な取引。Zigzagの感度が高いため、シグナルが頻繁に発生し、過度な取引につながる可能性があります。

- トレンド把握の精度が不十分。Zigzagによるトレンド判断にズレが生じ、エントリーのタイミングが理想的でない場合があります。

- レンジ相場でのパフォーマンスが劣る。レンジ相場では、この戦略で多くの損失取引が発生する可能性があります。

- 稼働期間が限定的。戦略は指定された日付範囲内でのみ稼働するため、一部の相場機会を逃す可能性があります。

最適化の方向性

- MAやMACDなど、より多くのテクニカル指標を導入し、トレンド判断の精度を高める。

- ATRなどの指標に基づいてポジションサイズを動的に調整するなど、ポジション管理を最適化する。

- 市場のボラティリティに応じてストップロスを動的に調整するなど、利確・ストップロスのロジックを最適化する。

- 市場センチメント指標を導入し、極度の楽観または悲観時にはエントリーを避ける。

- 日付制限を緩和し、戦略の汎用性を高める。

まとめ

AlphaTradingBotは、Zigzag指標とフィボナッチ・リトレースメントに基づいたトレンド追従型の日中戦略です。高値・安値でトレンドを判断し、トレンドのリトレース時にエントリーすることで、より高い勝率とリスクリワード比を追求します。この戦略の利点は、トレンド把握能力が高く、リトレースメントのロジックが明確で、リスクが測定可能な点です。一方で、過剰取引、トレンド判断の誤差、レンジ相場でのパフォーマンス低下などのリスクも存在します。今後はテクニカル指標、ポジション管理、利確・ストップロス、市場センチメントなどの観点から戦略を最適化し、戦略の堅牢性と収益性を向上させることが可能です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1