スクイーズバックテストトランスフォーマーv2.0

1

Follow

1802

Followers

概要

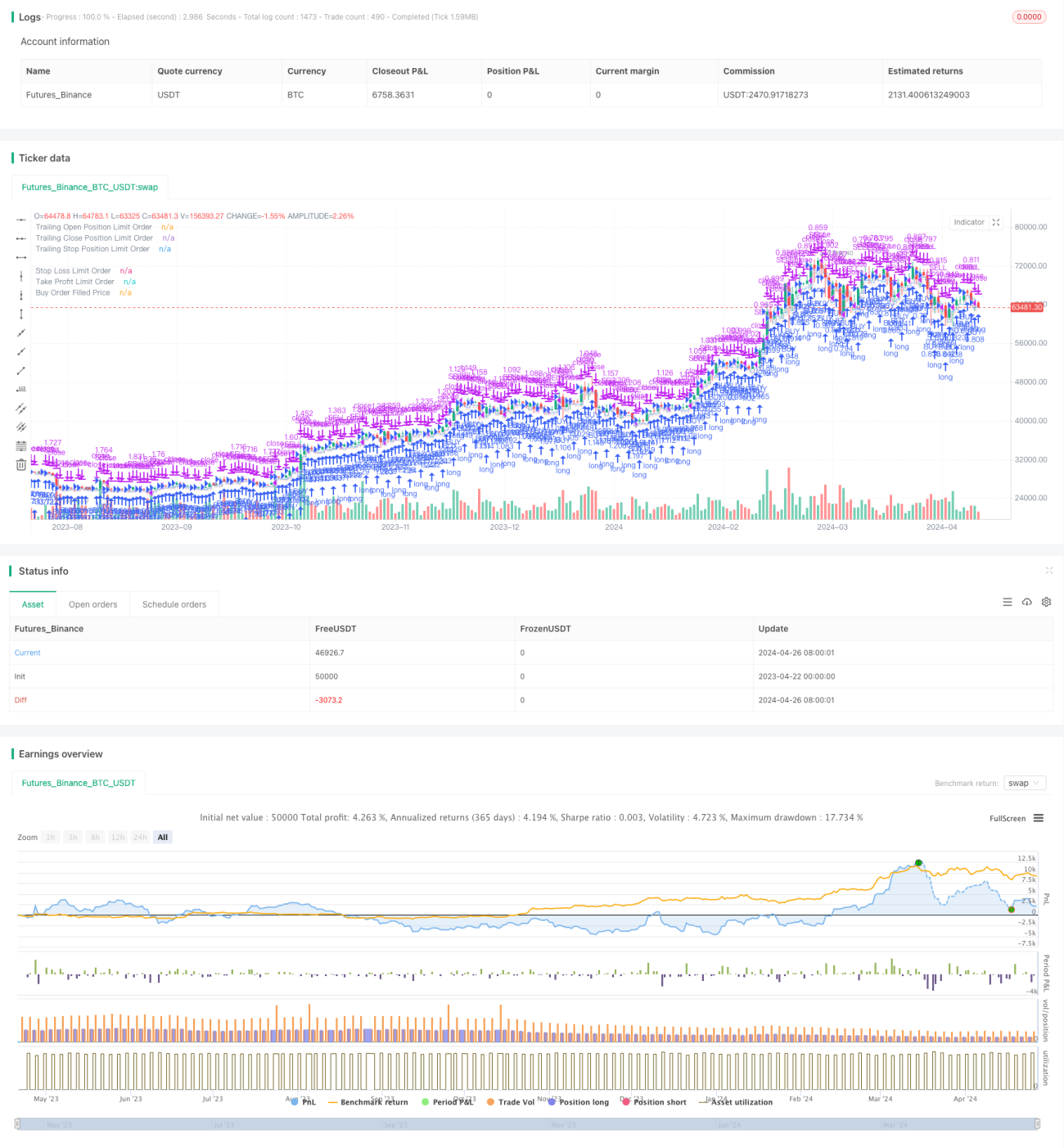

スクイーズバックテスト トランスフォーマー v2.0 は、スクイーズ型戦略に基づく定量取引システムです。エントリー、ストップロス、テイクプロフィットのパーセンテージ、および最大保有時間などのパラメーターを設定することで、特定の時間範囲内で戦略のバックテストを実行します。この戦略は複数の方向の取引をサポートしており、ロングまたはショートの取引方向を柔軟に設定できます。また、バックテスト期間の設定オプションが豊富で、固定期間または最大バックテスト時間を簡単に選択できます。

戦略の原理

- まず、ユーザーが設定したバックテスト期間パラメーターに基づき、バックテストの開始時間と終了時間を決定します。

- バックテスト期間中、現在ポジションがなく、価格がエントリー価格(オープンパーセンテージに基づいて計算)に達した場合、ポジションを開き、同時にストップロスとテイクプロフィットの価格(ストップロスとテイクプロフィットのパーセンテージに基づいて計算)を設定します。

- すでにポジションを保有している場合、以前のストップロス・テイクプロフィット注文をキャンセルし、新しいストップロス・テイクプロフィット価格(現在の保有平均価格に基づいて計算)を再設定します。

- 最大保有時間が設定されている場合、保有時間が最大値に達した時点で強制決済します。

- この戦略はロングとショートの両方向の取引をサポートします。

戦略のメリット

- パラメーター設定が柔軟で、さまざまな市場状況や取引ニーズに応じて調整できます。

- 複数方向の取引をサポートし、さまざまな市場環境で収益を得ることができます。

- バックテスト期間の設定オプションが豊富で、過去データのバックテストや分析を簡単に行えます。

- ストップロスとテイクプロフィットの設定によりリスクを効果的に管理し、資金効率を向上させます。

- 最大保有時間の設定により、長期保有による市場リスクを回避できます。

戦略のリスク

- エントリー価格、ストップロス価格、テイクプロフィット価格の設定は戦略の収益に大きな影響を与え、不適切なパラメーター設定は損失につながる可能性があります。

- 市場が激しく変動する場合、ポジションを開いた直後にストップロスがトリガーされ、損失が発生する可能性があります。

- 保有中に最大保有時間による強制決済が発生すると、その後の利益機会を逃す可能性があります。

- 特定の相場(例えばレンジ相場)では戦略のパフォーマンスが低下する可能性があります。

戦略の最適化方向

- より多くのテクニカル指標や市場センチメント指標を導入し、エントリー、ストップロス、テイクプロフィットの条件を最適化することで、戦略の安定性と収益性を向上させることを検討できます。

- 最大保有時間の設定については、市場の変動性やポジションの損益状況に応じて動的に調整し、固定時間での決済による機会費用を回避できます。

- レンジ相場の特性に対応するため、レンジブレイクアウトやトレンド転換の確認などのロジックを追加し、頻繁な取引によるコストを低減できます。

- ポジション管理や資金管理戦略を追加し、1回の取引のリスクエクスポージャーを制御することで、資金効率と安定性を向上させることを検討します。

まとめ

スクイーズバックテスト トランスフォーマー v2.0 は、スクイーズ型戦略に基づく定量取引システムであり、柔軟なパラメーター設定と複数方向の取引サポートにより、さまざまな市場環境で取引を行うことができます。また、充実したバックテスト期間の設定オプションとストップロス・テイクプロフィット設定により、過去データの分析やリスク管理が容易になります。ただし、戦略のパフォーマンスはパラメーター設定に大きく依存するため、市場の特性や取引ニーズに応じて最適化と改善を行い、戦略の堅牢性と収益性を高める必要があります。将来の最適化として、より多くのテクニカル指標の導入、最大保有時間の動的調整、レンジ相場戦略の改善、ポジション管理・資金管理の強化などが考えられます。

Source

Pine

/*backtest

start: 2023-04-22 00:00:00

end: 2024-04-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Squeeze Backtest by Shaqi v2.0", overlay=true, pyramiding=0, currency="USD", process_orders_on_close=true, commission_type=strategy.commission.percent, commission_value=0.075, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=100, backtest_fill_limits_assumption=0)

R0 = "6 Hours"Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1