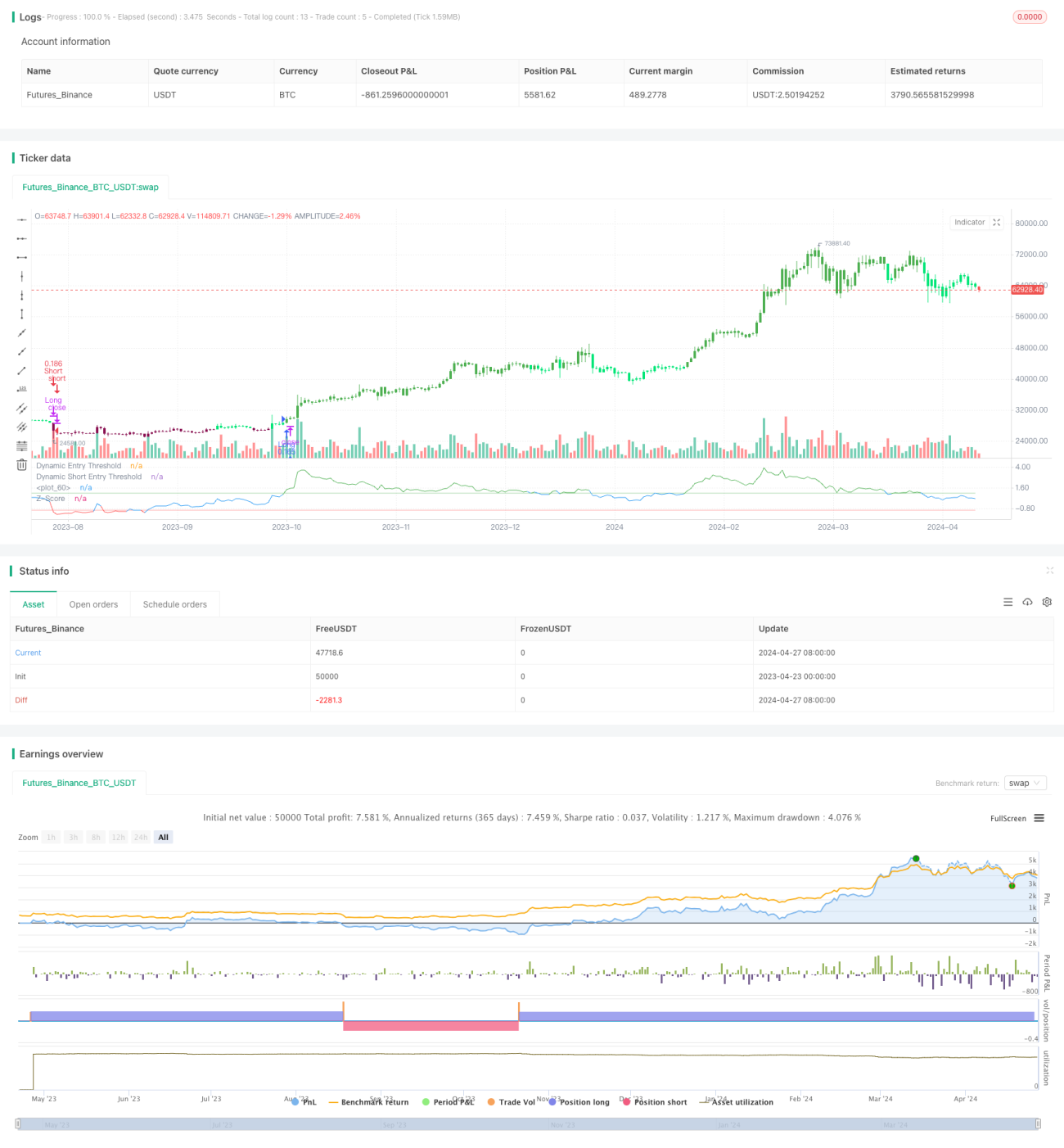

Z値に基づくトレンドフォロー戦略

1

Follow

1802

Followers

概要

「Z値に基づくトレンド追従戦略」は、統計指標であるZ値を活用し、価格が移動平均線から乖離する度合いを標準偏差で正規化することで、トレンドの機会を捉えます。この戦略は、価格がしばしば平均に回帰する市場において、その簡潔さと有効性で知られています。複数の指標に依存する複雑なシステムとは異なり、「Z値トレンド戦略」は明確で統計的に有意な価格変動に焦点を当てており、簡素でデータ駆動型のアプローチを好むトレーダーに適しています。

戦略の原理

この戦略の核心はZ値の計算にあります。Z値は、現在価格とユーザー定義の期間に基づく指数平滑移動平均線(EMA)との差を、同じ期間の価格の標準偏差で除算して求めます:

z = (x - μ) / σ

ここで、xは現在価格、μはEMAの平均値、σは標準偏差です。

取引シグナルは、Z値が事前に設定した閾値を超えたときに生成されます:

- ロングエントリー:Z値が正の閾値を上抜けたとき。

- ロングエグジット:Z値が負の閾値を下抜けたとき。

- ショートエントリー:Z値が負の閾値を下抜けたとき。

- ショートエグジット:Z値が正の閾値を上抜けたとき。

戦略の利点

- 簡潔で効果的:少数のパラメータのみを使用するため、理解と実装が容易でありながら、トレンドの機会を捉えるのに優れています。

- 統計的根拠:Z値は確立された統計ツールであり、この戦略に強固な理論的基盤を提供します。

- 適応性が高い:閾値、EMAおよび標準偏差の計算期間などのパラメータを調整することで、さまざまな取引スタイルや市場環境に柔軟に対応できます。

- 明確なシグナル:Z値の閾値超過に基づく取引シグナルは単純明快であり、迅速な意思決定と実行に役立ちます。

戦略のリスク

- パラメータ感度:不適切なパラメータ設定(閾値が高すぎる、または低すぎるなど)は、取引シグナルの歪みを引き起こし、機会を逃したり損失を招いたりする可能性があります。

- トレンド識別:レンジ相場やもみ合い相場では、この戦略は頻繁な偽シグナルに直面し、パフォーマンスが低下する可能性があります。

- ラグ効果:トレンド追従戦略であるため、エントリーとエグジットのシグナルにはいずれも一定のラグが生じ、最適なタイミングを逃す可能性があります。

上記のリスクは、継続的な市場分析、パラメータ最適化、およびバックテストに基づく慎重な実施によって、管理および緩和することができます。

戦略の最適化方向

- 動的閾値:ボラティリティに関連する動的閾値を導入することで、異なる市場状態に効果的に適応し、シグナルの質を向上させることができます。

- 複合指標:RSIやMACDなどの他のテクニカル指標を組み合わせて取引シグナルを二次確認し、信頼性を高めることができます。

- ポジション管理:ATRなどのポジション管理メカニズムを組み込み、レンジ相場では適時に減らし、トレンド相場では適時に増やすことで、リスク・リターン比を最適化します。

- 複数時間枠:複数の時間枠でZ値を計算し、異なるレベルのトレンドを捉えて戦略の次元を豊かにします。

まとめ

「Z値に基づくトレンド追従戦略」は、その簡潔さ、堅牢性、柔軟性により、トレンドの機会を捉える独自の視点を提供します。適切なパラメータ設定、慎重なリスク管理、および継続的な最適化を通じて、この戦略は定量トレーダーの強力なツールとなり、変動の激しい市場で安定して前進することが期待されます。

Source

Pine

/*backtest

start: 2023-04-23 00:00:00

end: 2024-04-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy employs a statistical approach by using a Z-score, which measures the deviation of the price from its moving average normalized by the standard deviation.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1