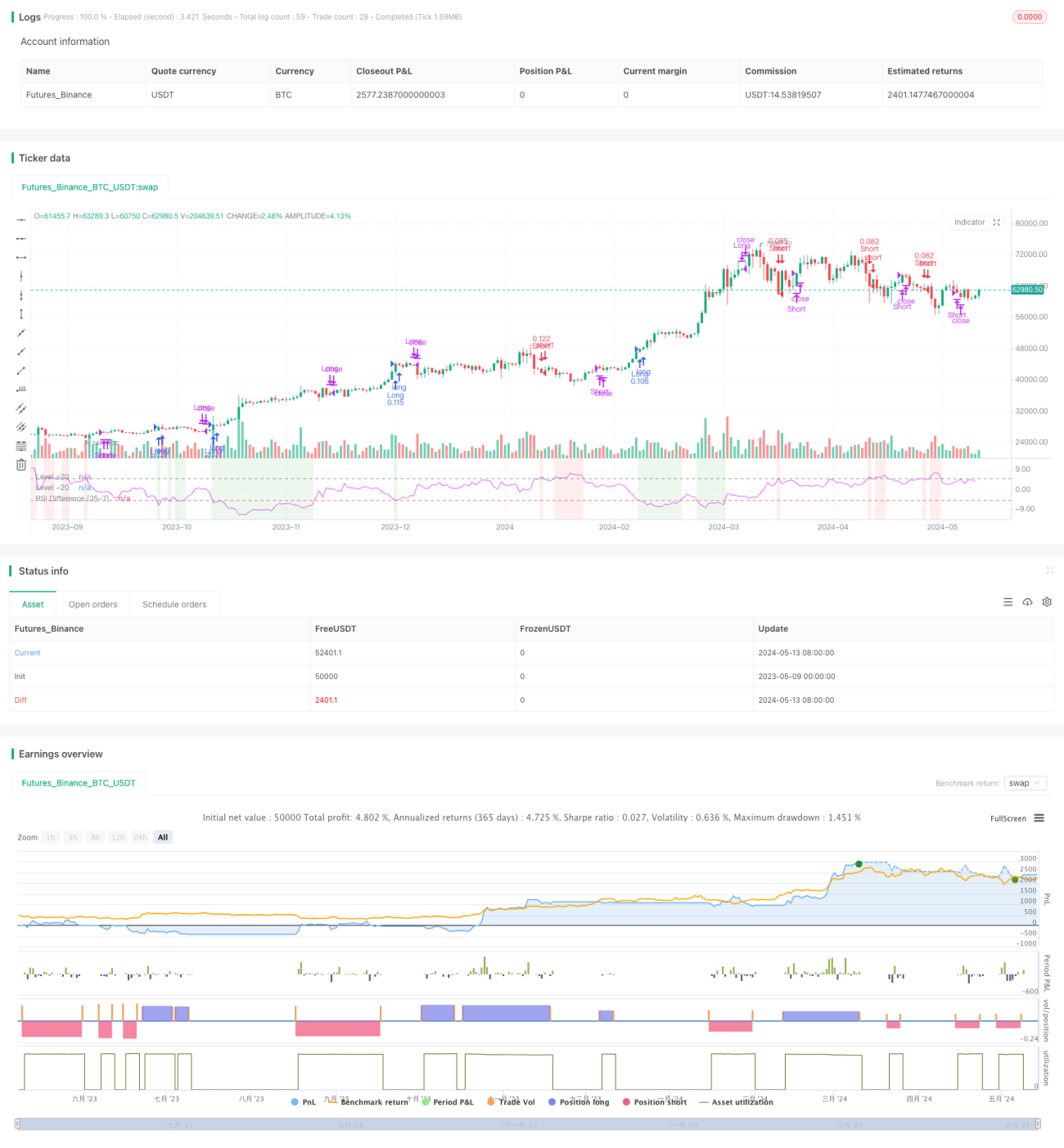

RSI二重差分戦略

概要

RSI二重差分戦略は、2つの異なる期間の相対力指数(RSI)の差を利用して取引判断を行う戦略です。従来の単一RSI戦略とは異なり、この戦略は短期RSIと長期RSIの差を分析することで、より細やかな市場動向分析手法を提供します。これにより、トレーダーは買われすぎや売られすぎの市場状況をより正確に捉え、より精度の高い取引判断を下すことができます。

戦略の原理

この戦略の核心は、異なる期間の2つのRSI指標を計算し、それらの差を分析することです。具体的には、短期RSI(デフォルトは21日)と長期RSI(デフォルトは42日)を使用します。長期RSIから短期RSIを引いた差を計算することで、RSI差分指標を得ます。RSI差分指標が-5を下回った場合、短期的なモメンタムが強まっていることを示し、ロングを検討します。RSI差分指標が+5を上回った場合、短期的なモメンタムが弱まっていることを示し、ショートを検討します。

戦略の利点

RSI二重差分戦略の利点は、より細やかな市場分析方法を提供する点にあります。異なる期間のRSIの差を分析することで、市場のモメンタム変化をより正確に捉え、トレーダーに信頼性の高い取引シグナルを提供できます。また、保有日数や利益確定・損切りの設定を導入することで、トレーダーはリスクエクスポージャーをより柔軟にコントロールできます。

戦略のリスク

RSI二重差分戦略には多くの利点があるものの、潜在的なリスクも存在します。まず、この戦略はRSI差分指標の正しい解釈に依存しており、トレーダーが指標を誤解すると誤った取引判断につながる可能性があります。次に、ボラティリティの高い市場環境では多くの偽シグナルが発生し、頻繁な取引や高い取引コストを招く恐れがあります。これらのリスクを軽減するために、トレーダーは他のテクニカル指標やファンダメンタル分析を組み合わせて、RSI二重差分戦略の取引シグナルを検証することを検討できます。

戦略の最適化方向性

RSI二重差分戦略のパフォーマンスをさらに向上させるために、以下の観点から戦略を最適化することが考えられます。

-

パラメータ最適化:RSI期間、RSI差分閾値、保有日数などのパラメータを最適化することで、現在の市場環境に最も適したパラメータ組み合わせを見つけ、戦略の収益性と安定性を高めます。

-

シグナルフィルタリング:他のテクニカル指標や市場センチメント指標を導入し、RSI二重差分戦略の取引シグナルを二次確認することで、偽シグナルの発生を減らします。

-

リスク管理:利益確定・損切りの設定を最適化するか、動的なリスク管理メカニズムを導入し、市場のボラティリティ変化に応じてポジションサイズを動的に調整することで、戦略のリスクエクスポージャーをより適切に管理します。

-

複数市場への適応:RSI二重差分戦略を外国為替、商品、債券などの他の金融市場に拡張し、戦略の汎用性と頑健性を検証します。

まとめ

RSI二重差分戦略は、相対力指数に基づくモメンタム取引戦略であり、異なる期間のRSIの差を分析することで、トレーダーに細やかな市場分析方法を提供します。この戦略には潜在的なリスクが存在しますが、適切な最適化と改善により、そのパフォーマンスをさらに向上させ、より信頼性が高く効果的な取引ツールにすることができます。

/*backtest

start: 2023-05-09 00:00:00

end: 2024-05-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy stands out by using two distinct RSI lengths, analyzing the differential between these to make precise trading decisions. - 1