1

Follow

1782

Followers

概要

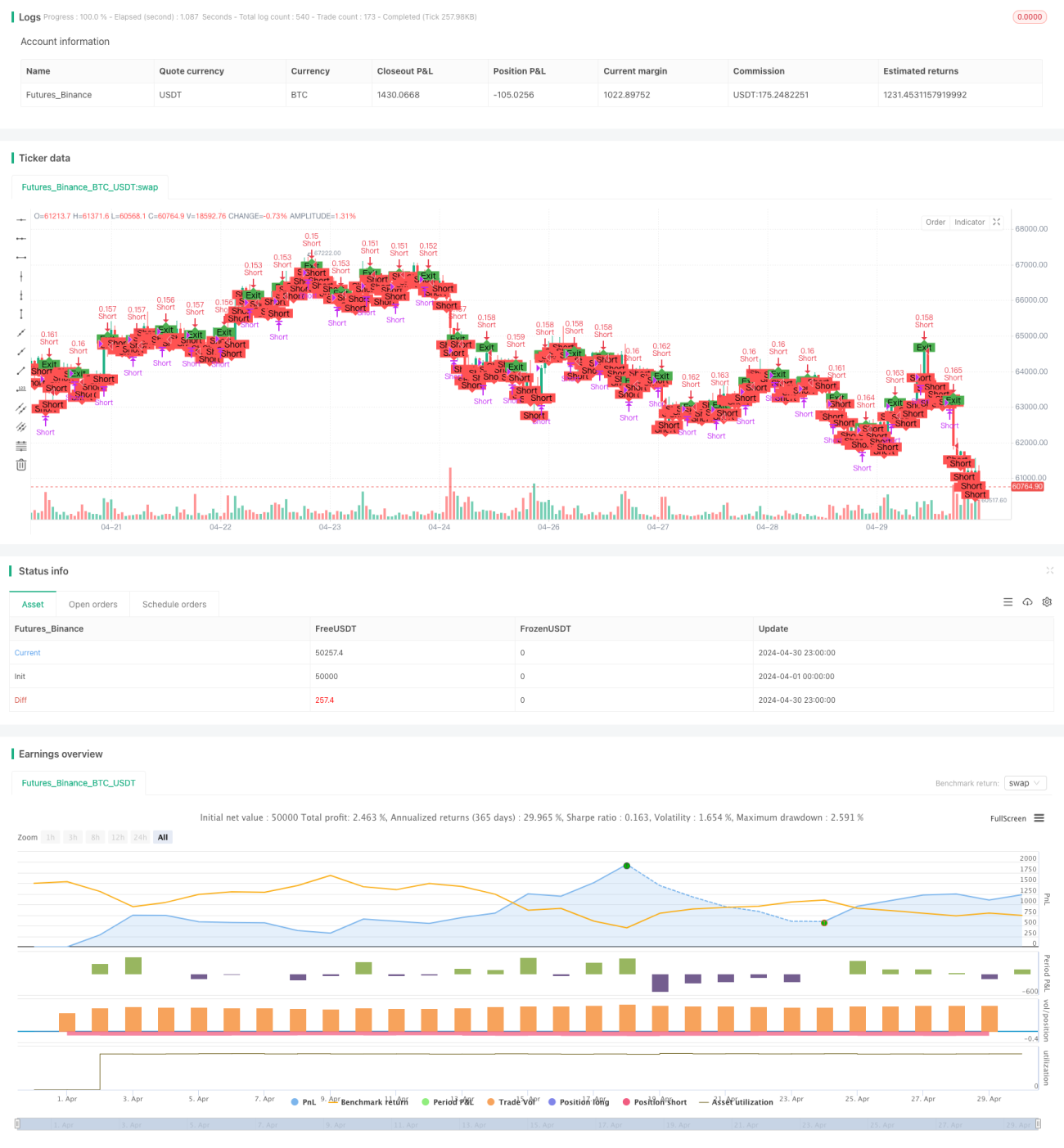

"ショートライン空白高流通通貨ペア戦略"は,高流通通貨ペアの短期的な下落傾向を利用して,価格が下落すると予想される状況で空白取引を行い,利益を得ることを目的としています.この戦略は,特定の条件に応じて空白ポジションに入って,ダイナミックなポジション規模とリスク管理手段を使用してリスクを制御し,利益をロックします.

戦略の基本は以下の通りです.

- 高流通通貨ペアを取引標として選択する.

- 値下がりパーセントの条件で空頭ポジションに入ります.

- ポジションの規模を動的に計算し,口座の利得の一定比率に基づいてリスクを制御する.

- ストップ&ストップ条件を設定し,潜在的な損失を制限し,利益をロックします.

- 取引期間や価格変動により退出する.

戦略原則

この戦略は,高流通通貨ペアの短期間の下落傾向を利用する.価格が特定の条件を満たしたときに,戦略は空頭ポジションに入る.具体的原理は以下の通りである.

- 取引を継続する際には,その取引が未開期であることを確認します.

- 設定した空頭取引の持続時間は,デフォルトで7日.

- 価格が入場価格から下落して設定されたパーセント (デフォルトは30%) に達すると空頭ポジションに入ります.

- アカウント権益の予測リスクパーセントに基づいてポジションサイズを動的に計算し,各取引の資金配分と全体リスクを制御します.

- ストップ・ロスとストップ・ストップの条件を設定し,価格が不利な方向に動くと,戦略は取引を終了して損失を最小限に抑える.価格が有利な方向に動くと,戦略は取引を終了して利益をロックする.

- 取引期間や価格変動により退出する.

戦略的優位性

- 短期取引:この戦略は,高流通通貨ペアの短期的な下落傾向を捕捉することに焦点を当てており,取引周期は比較的短く,利益目標の迅速な達成に役立ちます.

- 動的ポジション規模:口座権益の予測リスクパーセントに基づいて動的にポジション規模を計算し,各取引のリスクエッジを効果的に制御し,異なる市場条件に適応する.

- リスク管理: ストップ・ロズとストップ・ストップの条件を設定し,価格が不利な方向に動けば,取引を早期に終了し,潜在的な損失を最小限に抑え,価格が有利な方向に動けば,利益をロックし,既得利益を保護する.

- シンプルで使いやすい:この戦略の条件と論理は比較的シンプルで,理解しやすく,実行しやすく,さまざまな経験レベルのトレーダーに適しています.

戦略リスク

- 市場リスク: 通貨ペアの価格の変化は不確実であり,短期間に突発的な出来事や意外な動きが起こり,戦略が予想通りに機能しない可能性があります.

- スライドポイントリスク:市場の変動が激しい場合や流動性が不足している場合,実際の取引価格が予想価格と異なる可能性があり,戦略の収益性に影響する.

- パラメータ最適化リスク:この戦略のパフォーマンスは,空頭持続時間,価格下落パーセント,ストップダストストップパーセントなど,複数のパラメータの選択に依存する.不適切なパラメータ設定は,戦略の不良パフォーマンスを引き起こす可能性があります.

戦略最適化の方向性

- より多くの技術指標を導入する. 入場および出場条件に移動平均,相対強弱指数 (RSI) などなどの他の技術指標を導入し,入場信号の信頼性と正確性を向上させる.

- 最適化パラメータ選択:空頭持続時間,価格下落パーセント,ストップダストパーセントなどの重要なパラメータの最適化および感受性分析を行い,最適なパラメータの組み合わせを見つけ,戦略の収益性と安定性を向上させる.

- 市場情緒分析に加入:パニック指数 ((VIX)) や取引量などの市場情緒指標を組み合わせて,市場情緒を判断し,市場が極度に悲観的または取引量が大幅縮小したときに入場を避け,戦略の適応性を向上させる.

- 多通貨ペアポートフォリオ:この戦略を複数の流通率の高い通貨ペアに適用し,多元化されたポートフォリオを構築し,単一の通貨ペアのリスクを分散させ,全体的な収益の安定性を高める.

要約する

"ショートライン空調高流通通貨ペア戦略"は,高流通通貨ペアの短期的な下落傾向を捕捉し,特定の条件下で空頭取引を行い,動的なポジション規模とリスク管理措置を採用して,利益を得てリスクをコントロールする.この戦略の優点は,短期取引,動的なポジション規模と簡単な使いやすさにあるが,同時に,市場リスク,滑り点リスクおよびパラメータ最適化リスクにも直面する.さらなる最適化策として,より多くの技術指標の導入,最適化パラメータの選択,市場情緒分析の加入および複数の通貨ペアに適用することを考慮することができる.この戦略は,継続的な最適化と改善により,通貨市場で安定した利益を達成することが期待されている.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1