二重移動平均クロスストッププロフィットおよびストップロス戦略

1

Follow

1781

Followers

概要

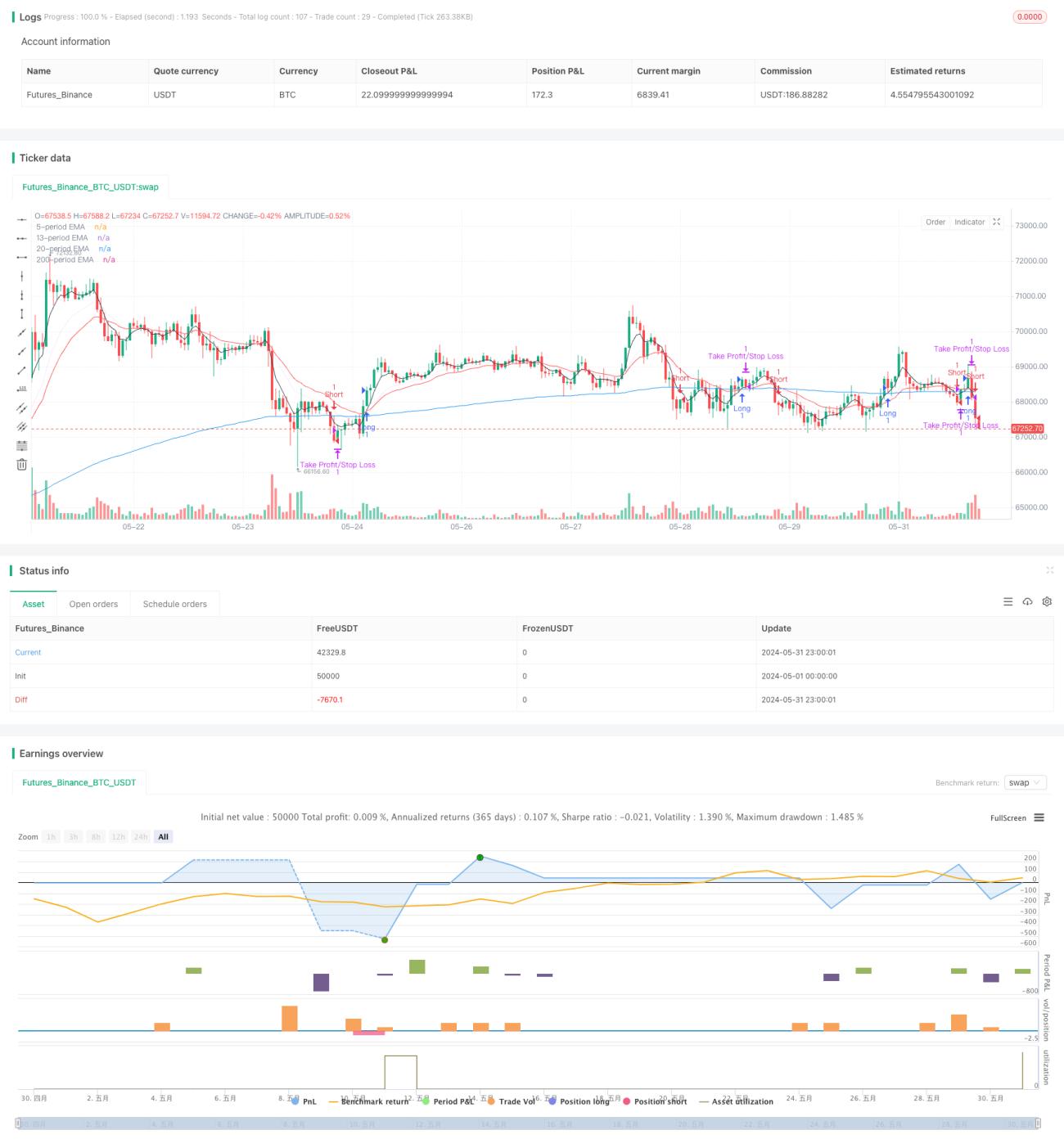

この戦略は,2つの異なる周期の指数移動平均 ((EMA) の交差を取引信号として使用し,同時に固定ポイントのストップとストップを設定する.短期EMAが下から上へと長期EMAを横切るときは,ポジションを多く開く.短期EMAが上から下へと長期EMAを横切るときは,ポジションを空にする.リスクを制御し,利益をロックするために取引時に固定ポイントのストップとストップを設定する.

戦略原則

- 2つの異なる周期のEMAを計算し,5周期と200周期をデフォルトとする.

- 5周期EMAが下から上へ200周期EMAを横切るときは多行信号を生成し,5周期EMAが上から下へ200周期EMAを横切るときは空白信号を生成する.

- ポジション開設後,ストップ・ロスのポイント (デフォルト50ポイント) とストップ・ストップのポイント (デフォルト200ポイント) を設定します.

- 価格がストップまたはストップ・ロスの点に触れたり,または200の取引サイクルに達したときに,平仓を終了します.

- グラフの取引量に応じてストップ・ストラスト・ポイントの数を調整することができます.

戦略的優位性

- シンプルで理解しやすい: 戦略の論理は明確で,理解しやすく,実行しやすい.

- トレンド追跡: EMAのトレンド特性を活用して,市場のトレンドをよりよく捉える.

- リスク管理:固定ポイントストップを設定し,単一取引のリスクを効果的に管理する.

- 柔軟性: ストップ・ストップ・ロスのポイントは,市場の波動性や個人のリスクの好みに応じて調整できます.

戦略リスク

- 偽信号: EMAの交差は偽信号を生じ,頻繁に取引し,資金の損失を引き起こす可能性があります.

- トレンド遅延:EMAは遅れの指標で,トレンドが形成された後に信号を発信し,最良の入場機会を逃す可能性があります.

- 整合市場:整合市場では,頻繁にEMAが交差すると,連続した損失取引が起こる可能性があります.

- 固定ポイントストップ: 固定ポイントストップは,市場の変動率の変化に適応できない可能性があり,ストップポジションの設定が不適切になります.

戦略最適化の方向性

- MACD,RSIなどの他の技術指標と組み合わせて,信号の信頼性を向上させる.

- 最適化パラメータ: EMA周期,ストップ・ストラップ・ポイントなどのパラメータを最適化して,戦略のパフォーマンスを向上させる.

- ダイナミックストップ:市場の波動に合わせてストップポイントを動的に調整し,市場の変化にうまく適応する.

- ポジション管理:リスクに基づくポジション調整などのポジション管理ルールを導入し,リスク調整後の収益を向上させる.

- フィルター:取引量,価格形態などの取引信号フィルタ条件を追加し,信号品質を向上させる.

要約する

双均線交差ストップ・ロスト戦略は,EMA交差によって取引シグナルを生成し,固定ポイント数ストップ・ロストを設定してリスクを制御する簡単な取引戦略である.この戦略の優点は,論理的に明確で,実行しやすいこと,市場トレンドをうまく捉えることができるという点にある.しかし,同時に,偽信号,トレンドの遅延,市場と固定ストップを調整するなどのリスクもある.最適化方向は,より多くの指標の最適化パラメータ,ダイナミックストップ,ポジション管理,フィルターの追加などの導入を含む.トレーダーは,自分のリスク好みと市場の特徴に応じて,この戦略を適切に最適化し,調整して,戦略の安定性と収益性を向上させることができる.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1