MACDとR:R比率の日内制限収束戦略

1

Follow

1802

Followers

概要

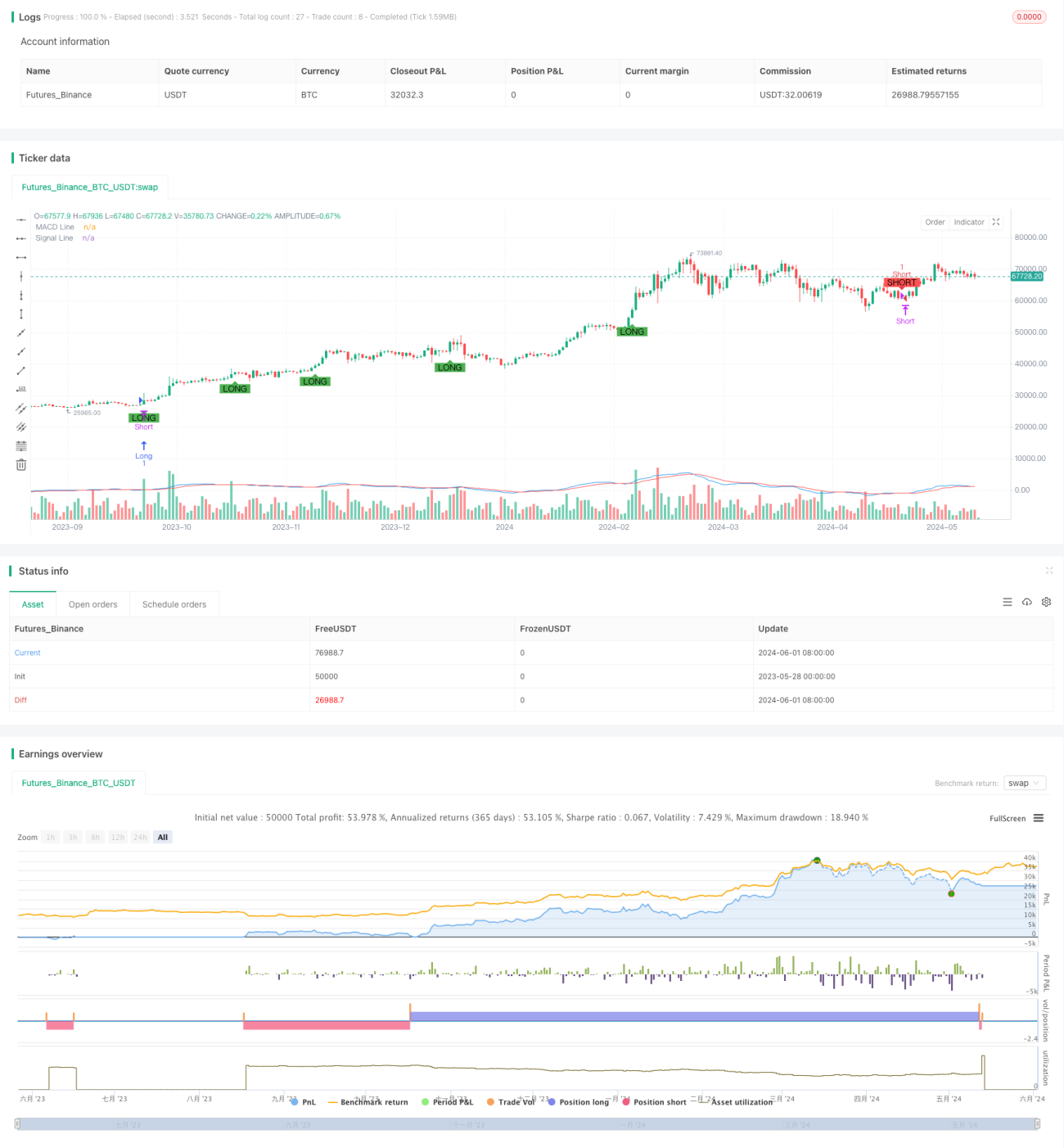

本戦略は、MACD指標の収束と発散に基づいて取引シグナルを判断します。MACD線とシグナル線がクロスし、かつMACD線の値が1.5を超える、または-1.5未満の場合に、それぞれ買いシグナルと売りシグナルが発生します。同時に、固定された利食い・損切りのポイントを設定し、リスクリワード比(R:R)の概念を導入しています。さらに、本戦略では日内最大損失・最大利益制限、およびより厳格なトレーリングストップを採用し、リスク管理を強化しています。

戦略の原理

- MACD指標のMACD線とシグナル線を計算します。

- MACD線とシグナル線のクロス状況を判断し、同時にMACD線の値が一定の閾値(1.5および-1.5)を超えているかを考慮します。

- 買いシグナルが発生した場合、買いポジションを建て、利食い価格を「現在の最高値+600最小変動単位」、損切り価格を「現在の最安値-100最小変動単位」に設定します。

- 売りシグナルが発生した場合、売りポジションを建て、利食い価格を「現在の最安値-600最小変動単位」、損切り価格を「現在の最高値+100最小変動単位」に設定します。

- トレーリングストップロジックを導入します。価格が建値から(買いの場合は上昇、売りの場合は下落)300最小変動単位を超えた場合、損切り価格を「建値+(終値-建値-300)」(買いの場合)または「建値-(建値-終値-300)」(売りの場合)に移動させます。

- 日内最大損失・最大利益制限を設定します。当日の損失が600最小変動単位に達した場合、または利益が1800最小変動単位に達した場合、すべてのポジションを決済します。

優位性分析

- MACD指標と価格閾値条件を組み合わせることで、ノイズシグナルの一部を効果的に除去します。

- 固定リスクリワード比(R:R)により、各取引のリスクとリターンが管理可能です。

- トレーリングストップロジックは、トレンド形成後に利益を保護し、ドローダウンを低減します。

- 日内の最大損失・最大利益制限は、1日あたりのリスクエクスポージャーを管理し、過度な損失や利益後のドローダウンを防ぎます。

リスク分析

- MACD指標には遅延性があり、シグナルの遅延や誤ったシグナルが発生する可能性があります。

- 固定された利食い・損切りポイントは、異なる市場状況に適応できない可能性があり、レンジ相場では頻繁に損切りが発生する恐れがあります。

- トレーリングストップロジックは、トレンドが反転した際に適時損切りできず、利益を吐き出す可能性があります。

- 日内の最大損失・最大利益制限により、トレンドが明確な日に早期に決済され、潜在的な利益を逃す可能性があります。

最適化の方向性

- 複数の時間枠のMACD指標を使用してシグナルを確認し、シグナルの精度を高めることを検討します。

- 市場のボラティリティに応じて利食い・損切りポイントを動的に調整し、異なる市場状況に適応させます。

- トレーリングストップロジックを最適化します。例えば、ATR指標に基づいてトレーリングストップの距離を設定し、価格変動により適応させます。

- 日内の最大損失・最大利益制限のパラメータを最適化し、適切な制限値を見つけることで、リスクを管理しながらトレンド相場を捉えられるようにします。

まとめ

本戦略は、MACD指標の収束と発散に基づいて取引シグナルを判断し、リスクリワード比、トレーリングストップ、日内制限などのリスク管理措置を導入しています。戦略は一定の範囲でトレンド相場を捉え、リスクを管理できますが、まだ最適化と改善の余地があります。今後は、シグナル確認、利食い・損切り、トレーリングストップ、日内制限などの観点から最適化を図り、より安定したリターンを目指すことが考えられます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1