GトレンドEMA ATRスマートトレード戦略

1

Follow

1802

Followers

概要

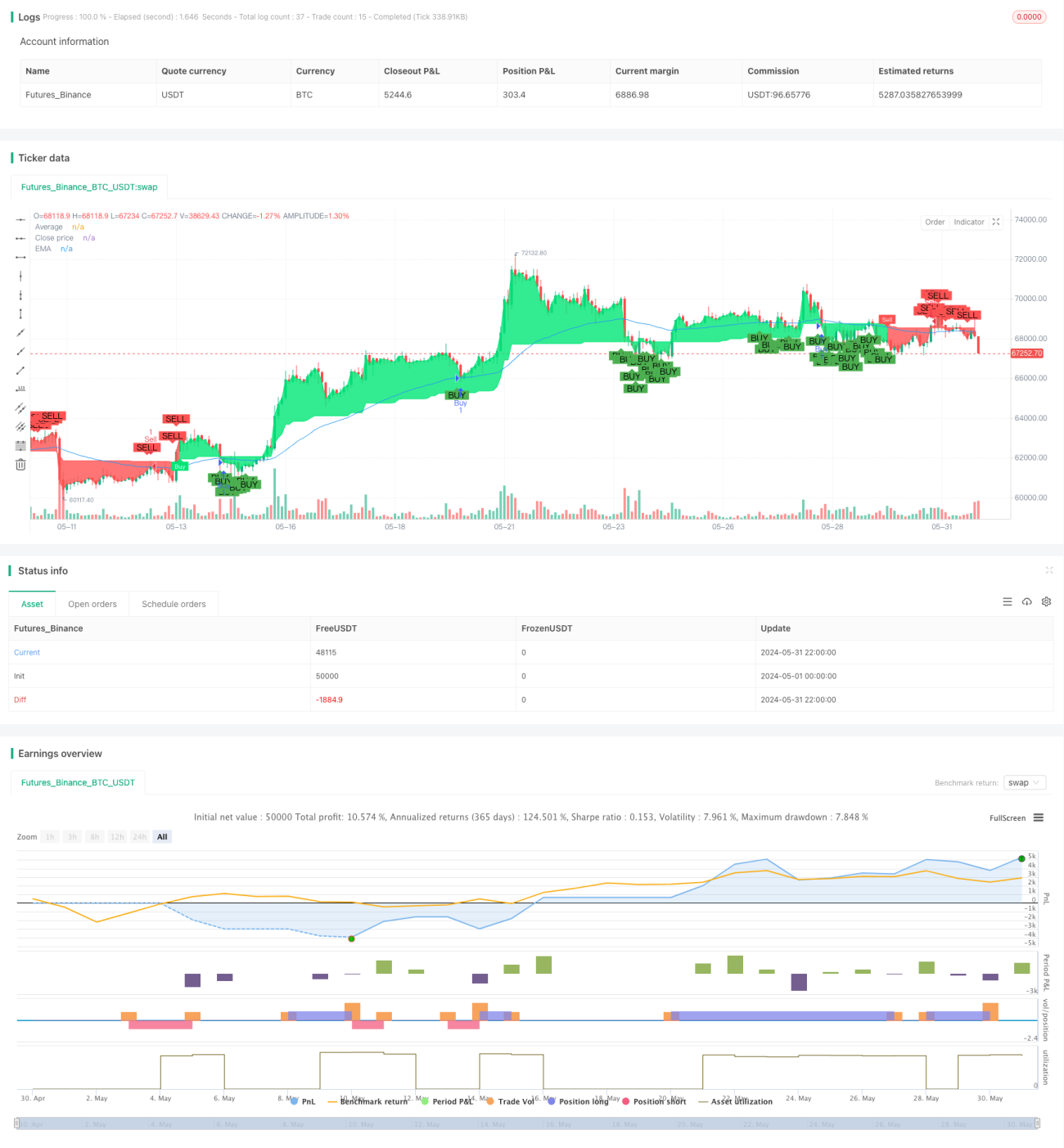

この戦略はGチャネルインジケーターを利用して市場のトレンド方向を識別し、同時にEMAとATRインジケーターを組み合わせてエントリーおよびエグジットポイントを最適化します。戦略の主な考え方は、価格がGチャネルの上限を突破し、かつEMAを下回っているときにロング、下限を突破し、かつEMAを上回っているときにショートするというものです。同時にATRを利用して動的なストップロスと利確を設定し、ストップロスはATRの2倍、利確はATRの4倍とします。この方法により、トレンド相場でより多くの利益を得ると同時に、リスクを厳密に管理できます。

戦略の原理

- Gチャネルの上限・下限の計算:現在の終値と過去の最高値・最安値を使用してGチャネルの上限・下限を計算します。

- トレンド方向の判断:価格とGチャネルの上限・下限の関係から、強気トレンドか弱気トレンドかを判断します。

- EMAの計算:指定期間のEMA値を計算します。

- ATRの計算:指定期間のATR値を計算します。

- 売買条件の判断:価格がGチャネルの上限を突破し、かつEMAを下回っているときにロング、下限を突破し、かつEMAを上回っているときにショートのトリガーとなります。

- ストップロス・利確の設定:ロングの場合、ストップロスはエントリー価格-ATR×2、利確はエントリー価格+ATR×4;ショートの場合、ストップロスはエントリー価格+ATR×2、利確はエントリー価格-ATR×4とします。

- 戦略トリガー:売買条件を満たした時に対応するポジションを建て、ストップロス・利確を設定します。

戦略のメリット

- トレンドフォロー:Gチャネルを活用して市場トレンドを効果的に捉え、トレンド相場に適しています。

- 動的なストップロス・利確:ATRを使用してストップロス・利確を動的に調整し、市場の変動に適応しやすくなります。

- リスク管理:ストップロスをATRの2倍に設定することで、各取引のリスクを厳格に管理します。

- シンプルで使いやすい:戦略ロジックが明確で、多くの投資家が利用しやすいです。

戦略のリスク

- レンジ相場:揉み合い相場では頻繁な売買シグナルにより損失が拡大する可能性があります。

- パラメータ最適化:銘柄や時間足によって適切なパラメータが異なるため、パラメータをそのまま流用するとリスクが生じる可能性があります。

- ブラックスワンイベント:極端な相場環境では価格変動が激しく、ストップロスが機能しない場合があります。

戦略の最適化方向

- トレンドフィルター:MAクロスやDMIなどのトレンドフィルター条件を追加し、レンジ相場での取引を減らします。

- パラメータ最適化:異なる銘柄や時間足に合わせてパラメータを最適化し、最適なパラメータ組み合わせを見つけます。

- ポジション管理:市場のボラティリティに応じてポジションサイズを動的に調整し、資金効率を高めます。

- コンビネーション戦略:本戦略を他の有効な戦略と組み合わせ、安定性を向上させます。

まとめ

この戦略はGチャネル、EMA、ATRなどの指標を使用して、シンプルかつ効果的なトレンドフォロー取引システムを構築しています。トレンド相場では良好な結果が期待できますが、レンジ相場ではパフォーマンスが平凡です。今後はトレンドフィルター、パラメータ最適化、ポジション管理、コンビネーション戦略などの観点から戦略を最適化し、堅牢性と収益性をさらに向上させることができます。

Source

Pine

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Full credit to AlexGrover: https://www.tradingview.com/script/fIvlS64B-G-Channels-Efficient-Calculation-Of-Upper-Lower-Extremities/

strategy ("G-Channel Trend Detection with EMA Strategy and ATR", shorttitle="G-Trend EMA ATR Strategy", overlay=true)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1