シンプルコンビネーション戦略:ピボットポイントスーパートレンドと二重指数移動平均線

1

Follow

1802

Followers

概要

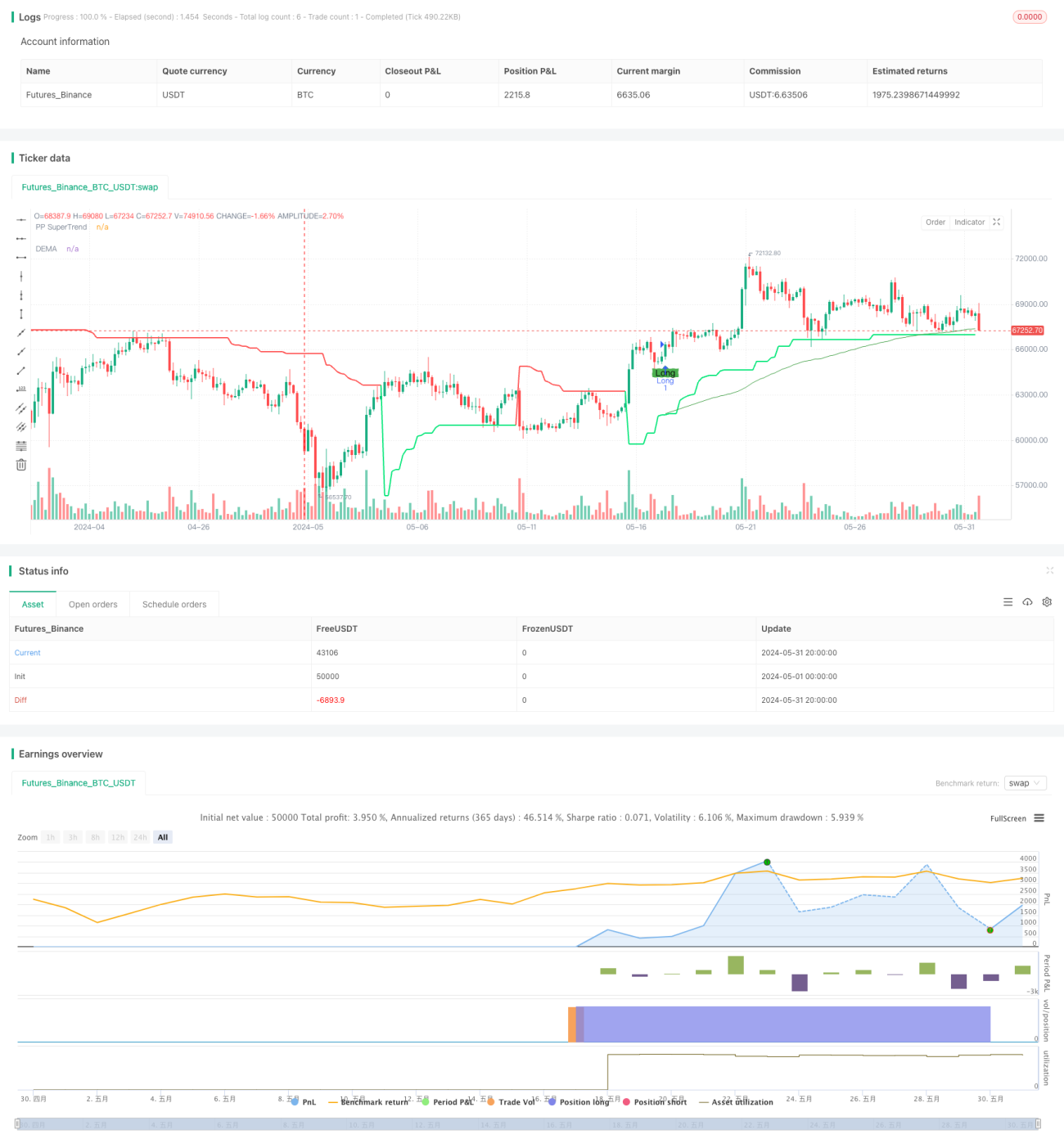

本戦略は、ピボットポイントスーパートレンド指標とダブル指数移動平均(DEMA)指標を組み合わせ、これらの2つの指標に対する価格の位置関係を分析して売買シグナルを判定する。価格がピボットポイントスーパートレンド指標を上抜け、かつDEMA指標より高い場合に買いシグナルが発生し、価格がピボットポイントスーパートレンド指標を下抜け、かつDEMA指標より低い場合に売りシグナルが発生する。本戦略は市場の中長期的なトレンドを捉えると同時に、短期的な価格変動にも対応できる。

戦略の仕組み

- ピボットポイントスーパートレンド指標の計算:一定期間の最高値と最安値の平均を中心点とし、平均真のレンジ(ATR)に基づいて上限ラインと下限ラインを計算し、動的なサポート・レジスタンスラインを形成する。

- DEMA指標の計算:まず終値の指数移動平均(EMA)を計算し、次にそのEMAに対してさらに指数移動平均を計算し、最後に2倍のEMAからDEMAを差し引いて最終的なDEMA指標を得る。

- 売買シグナルの生成:終値がピボットポイントスーパートレンドの上限ラインを上抜け、かつDEMA指標より高い場合に買いシグナルが発生し、終値がピボットポイントスーパートレンドの下限ラインを下抜け、かつDEMA指標より低い場合に売りシグナルが発生する。

- ストップロスとテイクプロフィットの設定:ピップ値(Pip Value)と事前設定されたストップロスピップ数(Stop Loss Pips)およびテイクプロフィットピップ数(Take Profit Pips)に基づいて、具体的なストップロス価格とテイクプロフィット価格を計算する。

戦略の優位性

- トレンド追随能力が高い:ピボットポイントスーパートレンド指標は市場のトレンドを効果的に捉えることができ、DEMA指標は価格のノイズを除去し、より平滑なトレンド判断の根拠を提供する。両者を組み合わせることで、市場の主要トレンドを正確に把握できる。

- 適応性が高い:ピボットポイントスーパートレンド指標の上限・下限ラインを動的に調整することで、異なる市場の変動状況に適応でき、戦略の適応性が向上する。

- リスク管理能力が高い:明確なストップロスとテイクプロフィットの水準を設定することで、1回の取引のリスクエクスポージャーを効果的にコントロールし、同時に獲得済みの利益を適時に確定できる。

戦略のリスク

- パラメータ設定リスク:戦略のパフォーマンスは、ピボットポイント期間、ATR係数、DEMA長さなどの複数のパラメータ設定に依存する。異なるパラメータの組み合わせによって戦略のパフォーマンスが大きく異なる可能性があり、慎重な選択と最適化が必要である。

- レンジ相場リスク:レンジ相場においては、頻繁な売買シグナルにより取引過多となり、取引コストとスリッページリスクが増加する可能性がある。

- トレンド転換リスク:市場トレンドが転換する場合、戦略が連続して損失を出す可能性があり、他の分析手段と組み合わせて戦略を適時調整する必要がある。

戦略の最適化の方向性

- パラメータ最適化:異なる時間足や取引商品に対してパラメータ最適化テストを実施し、最適なパラメータ組み合わせを見つけることで、戦略の安定性と収益性を向上させる。

- シグナルフィルタリング:売買シグナルが発生した際に、他のテクニカル指標や価格行動の特性と組み合わせて二次確認を行い、シグナルの信頼性を高め、偽シグナルによる損失を低減する。

- ポジション管理:市場の変動状況と口座のリスク許容度に基づいて、取引ごとのポジションサイズを動的に調整し、全体的なリスクエクスポージャーをコントロールする。

- 組み合わせ最適化:本戦略を他の戦略や取引システムと組み合わせることで、リスクを分散し安定性を強化し、戦略の長期的なパフォーマンスを向上させる。

まとめ

本戦略は、ピボットポイントスーパートレンド指標とDEMA指標を組み合わせることで、市場トレンドを良好に捉えるとともに、短期的な変動にも対応できる。戦略には強いトレンド追随能力、適応性の高さ、リスク管理能力の強さといった利点がある一方、パラメータ設定、レンジ相場、トレンド転換などのリスクも存在する。パラメータ最適化、シグナルフィルタリング、ポジション管理、組み合わせ最適化などの手段を通じて、戦略の安定性と収益性をさらに向上させ、さまざまな市場環境により適応することが可能である。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1