ZLSMA-拡張型シャンデリアエグジット戦略と出来高パルス検出

1

Follow

1802

Followers

概要

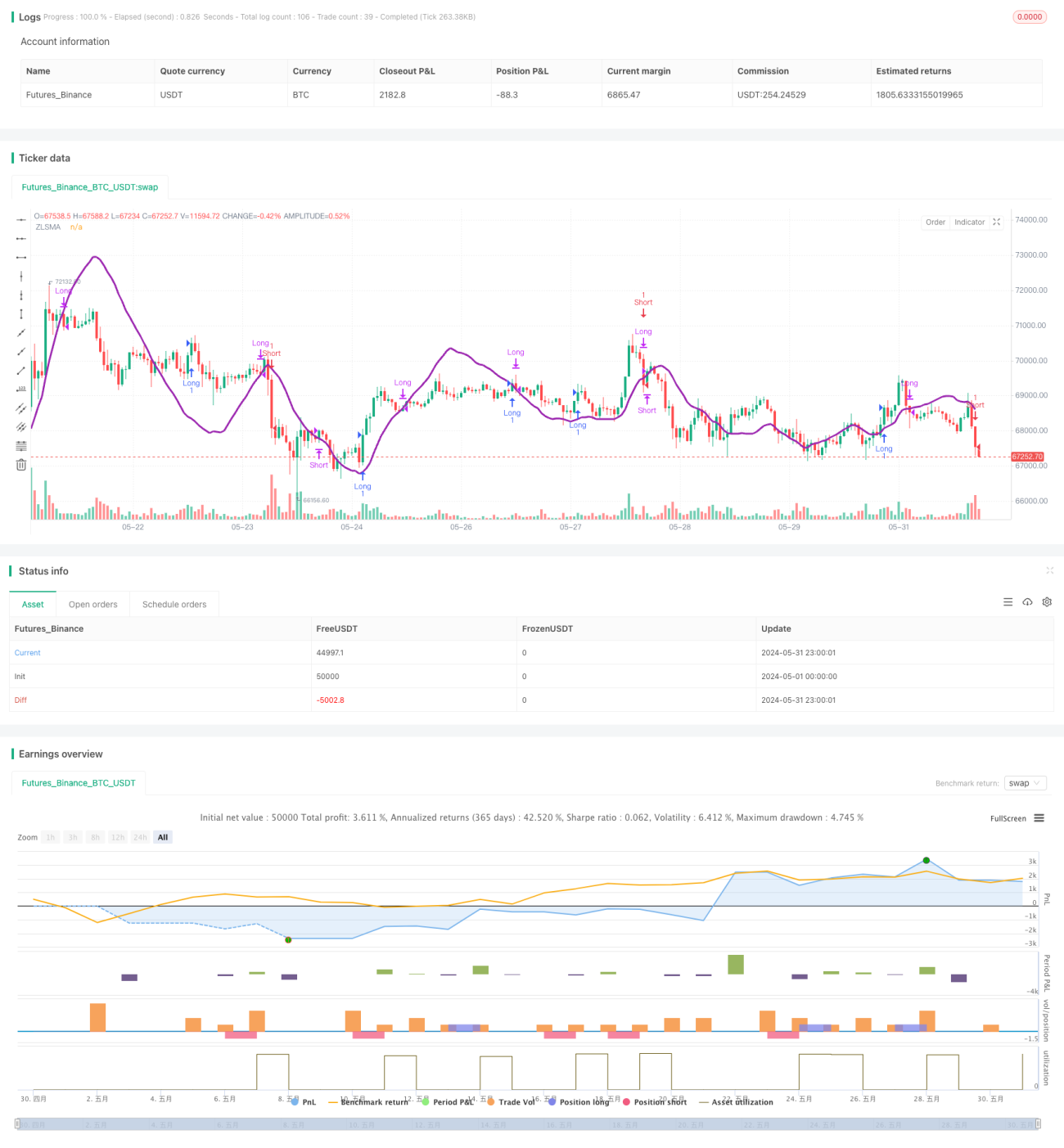

本戦略は、シャンデリア・イグジット(Chandelier Exit)、ゼロラグ移動平均線(ZLSMA)、および相対出来高(RVOL)パルス検出を組み合わせた、完全な取引システムです。シャンデリア・イグジットは真の変動幅(ATR)を用いてストップロス位置を動的に調整し、市場の変化に適応します。ZLSMAは価格トレンドを正確に捉え、取引の方向性を示します。RVOLパルス検出は、ボラティリティの低いレンジ相場を回避し、取引の質を向上させるのに役立ちます。

戦略の原理

- ATRを計算し、ATRと最高値/最安値に基づいて買いと売りのストップロス位置を計算します。

- ZLSMAを計算し、トレンド方向を判断する基準とします。

- RVOLを計算し、RVOLと設定された閾値を比較して出来高にパルスが発生したかどうかを判断します。

- 買いエントリー:現在の終値がZLSMAを上抜け、かつRVOLが閾値より大きい場合、買いポジションを建て、ストップロス位置は直近の安値とします。

- 売りエントリー:現在の終値がZLSMAを下抜け、かつRVOLが閾値より大きい場合、売りポジションを建て、ストップロス位置は直近の高値とします。

- 買いイグジット:現在の終値がZLSMAを下抜けた場合、買いポジションを決済します。

- 売りイグジット:現在の終値がZLSMAを上抜けた場合、売りポジションを決済します。

戦略の優位性

- シャンデリア・イグジットはストップロス位置を動的に調整できるため、固定ストップロスによるリスクを低減します。

- ZLSMAは価格変動に素早く反応し、信頼性の高いトレンド判断を提供します。

- RVOLパルス検出は、ボラティリティの低いレンジ相場を回避し、取引の質を向上させます。

- 戦略ロジックは明確で、理解・実装が容易です。

戦略のリスク

- トレンドがはっきりしない、または頻繁にレンジ相場となる市場では、取引回数が増加し、手数料コストが上昇する可能性があります。

- 戦略のパラメータ設定(ATR期間、ZLSMA期間、RVOL閾値など)は戦略のパフォーマンスに大きな影響を与え、不適切なパラメータは戦略のパフォーマンス低下につながる可能性があります。

- 本戦略はポジション管理とリスクコントロールを考慮しておらず、実際の適用には資金管理の原則を組み合わせる必要があります。

戦略の最適化方向

- トレンド確認指標(移動平均線システムやモメンタム指標など)を導入し、トレンド判断の精度をさらに高めます。

- RVOLパルス検出のロジックを最適化します(例:連続して複数のRVOLパルスが発生した場合のみ取引を行うなど)し、シグナルの質をさらに向上させます。

- イグジット条件に利食いロジックを追加し、一定の利益目標に達したらポジションを決済して、獲得した利益を確定します。

- 市場特性や取引銘柄に応じて戦略パラメータを最適化し、最適なパラメータの組み合わせを見つけます。

- ポジション管理とリスクコントロールの原則を組み合わせて戦略を改善し、戦略の堅牢性と信頼性を高めます。

まとめ

ZLSMA強化型シャンデリア・イグジット戦略と出来高パルス検出は、トレンドフォロー型戦略であり、動的ストップロス、トレンド判断、出来高パルス検出を通じて、トレンドの機会を捉えつつ取引リスクをコントロールします。戦略ロジックは明確で、理解・実装が容易ですが、実際の適用には特定の市場特性や取引銘柄に応じた最適化と改善が必要です。より多くのシグナル確認指標の導入、イグジット条件の最適化、適切なパラメータ設定、そして厳格なポジション管理とリスクコントロールにより、本戦略は堅牢で効率的な取引ツールとなる可能性があります。

Source

Pine

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Chandelier Exit Strategy with ZLSMA and Volume Spike Detection", shorttitle="CES with ZLSMA and Volume", overlay=true, process_orders_on_close=true, calc_on_every_tick=false)

// Chandelier Exit Inputs

lengthAtr = input.int(title='ATR Period', defval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1