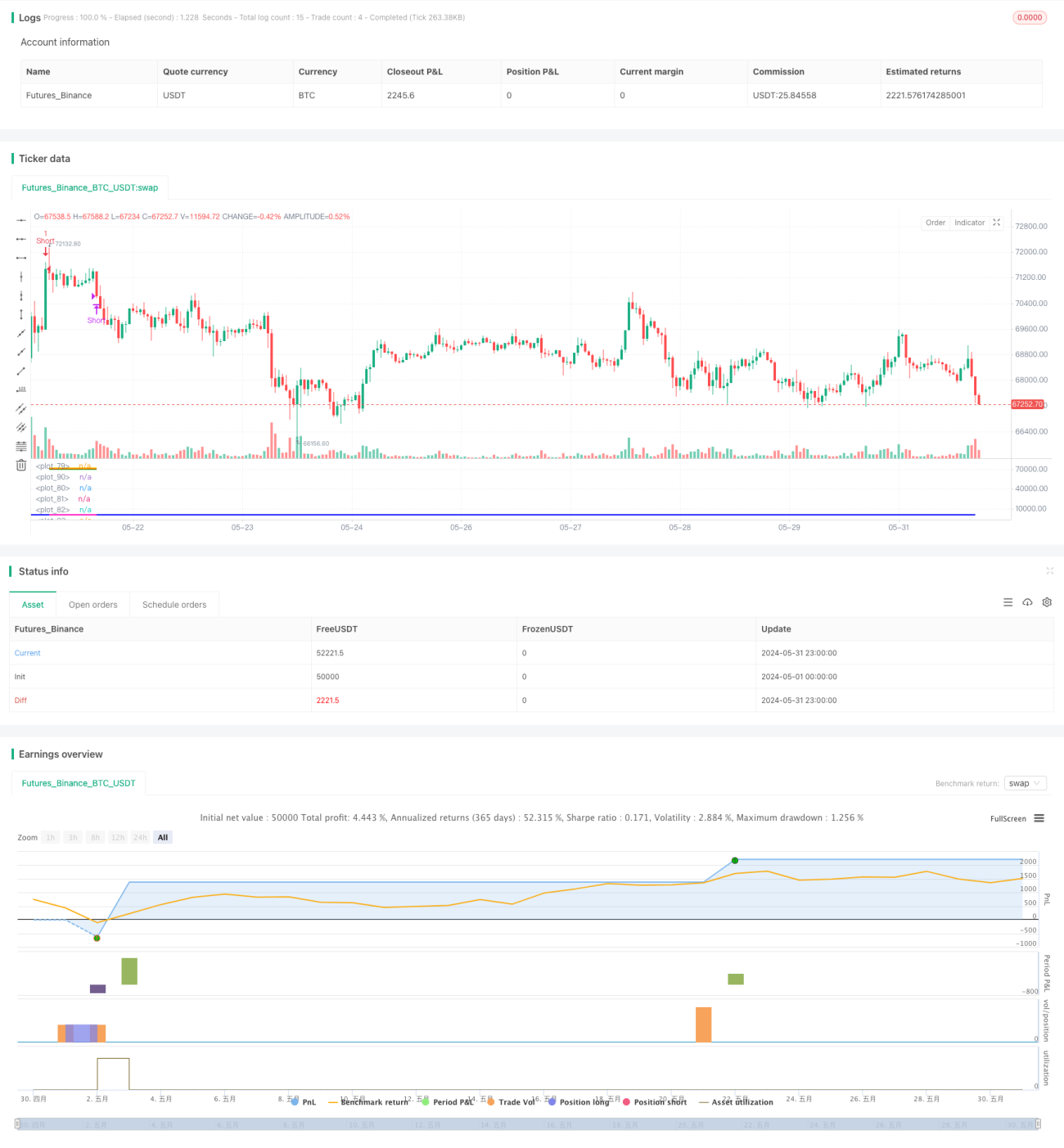

多層級RSI回帰取引戦略と動的ボラティリティ調整

概要

本戦略は、RSI指標と価格のボラティリティに基づく多層的な平均回帰取引システムです。RSIの極端な値と異常に大きな価格変動をエントリーシグナルとして利用し、ピラミッディングによるポジション追加と動的な利確によりリスク管理と収益最適化を図ります。戦略の核心は、市場に極端な変動が発生した際にエントリーし、価格が正常水準に戻ったところで利益確定することにあります。

戦略の原理

-

エントリー条件:

- 主指標として20期間RSI(RSI20)を使用

- 複数のRSI閾値(35/65、30/70、25/75、20/80)と対応するボラティリティ閾値を設定

- RSIがいずれかの閾値に達し、かつ現在のローソク足の実体サイズが対応するボラティリティ閾値を超えた場合にエントリーシグナルが発生

- 追加条件: 価格が最近の高値/安値のサポート/レジスタンスラインを一定割合だけブレイクしていること

-

ポジション追加メカニズム:

- 最大5回のエントリー(初回エントリー+4回の追加)を許可

- 追加エントリーごとに、より厳しいRSIおよびボラティリティ条件を満たす必要がある

-

エグジットメカニズム:

- 5段階の異なる利確ポイントを設定

- 利確ポイントはエントリー時のサポート/レジスタンスラインに基づいて動的に計算

- 保有ポジション数が増加するにつれて、利確目標は徐々に低下

-

リスク管理:

- パーセンテージ・リスクモデルを使用。各取引のリスクは口座総額の20%に固定

- 同時保有ポジションの最大数を5に設定し、総リスクエクスポージャーを制限

戦略の利点

-

多層的なエントリー: 複数のRSIとボラティリティ閾値を設定することで、戦略はさまざまな度合いの市場の極端な状況を捉え、取引機会を増やします。

-

動的な利確: サポート/レジスタンスラインに基づいて計算された利確ポイントは、市場構造に合わせて適応的に調整され、利益を保護しつつ早期の離脱を防ぎます。

-

ピラミッディングによるポジション追加: トレンドが継続する際にポジションを増やすことで、収益の可能性を大幅に高めます。

-

リスク管理: 固定パーセンテージのリスクと最大保有ポジション数の制限により、各取引および総合的なリスクを効果的に管理します。

-

柔軟性: 多くの調整可能なパラメータにより、異なる市場環境や取引銘柄に戦略を適応させることができます。

-

平均回帰+トレンドフォロー: 平均回帰とトレンドフォローの長所を組み合わせ、短期的な反転を捉えつつ大きなトレンドも見逃しません。

戦略のリスク

-

過剰取引: 高ボラティリティ市場では取引シグナルが頻繁に発生し、手数料が高くなる可能性があります。

-

偽のブレイクアウト: 一時的な極端な変動の後に価格が急反発し、誤ったシグナルとなる可能性があります。

-

連続損失: 市場が一方向に動き続けると、ポジション追加により大きな損失が発生する可能性があります。

-

パラメータ感度: 戦略のパフォーマンスはパラメータ設定に大きく依存し、過学習のリスクがあります。

-

スリッページの影響: 激しい変動期には深刻なスリッページが発生し、戦略のパフォーマンスに影響を与える可能性があります。

-

市場環境依存: 低ボラティリティや強いトレンド相場など、特定の市場環境では戦略のパフォーマンスが低下する可能性があります。

戦略の最適化方向性

-

動的パラメータ調整: 市場状態に応じてRSI閾値とボラティリティ閾値を動的に調整する適応メカニズムを導入。

-

マルチタイムフレーム分析: より長期の市場トレンド判断を組み合わせ、エントリーの質を向上。

-

ストップロスの最適化: トレーリングストップやATRベースの動的ストップロスを追加し、リスクをさらに抑制。

-

市場状態フィルター: トレンド強度やボラティリティサイクルなどのフィルター条件を追加し、不適切な市場環境での取引を回避。

-

資金管理の最適化: シグナルのレベルに応じて取引サイズを調整するなど、より細かなポジション管理を実現。

-

機械学習の統合: 機械学習アルゴリズムを利用してパラメータ選択とシグナル生成プロセスを最適化。

-

相関分析: 他の資産との相関分析を追加し、戦略の安定性と分散性を向上。

まとめ

本多層RSI回帰取引戦略は、テクニカル分析、動的リスク管理、ピラミッディングによるポジション追加技術を巧みに組み合わせた綿密に設計された定量取引システムです。市場の極端な変動を捉え、価格が戻る際に利益を得ることで、強い収益可能性を示しています。しかし、過剰取引や市場環境依存などの課題にも直面しています。今後の最適化方向は、戦略の適応能力とリスク管理能力の向上に焦点を当て、様々な市場環境に対応できるようにすべきです。総じて、これは良好な基盤を持つ戦略フレームワークであり、さらなる最適化とバックテストを経て、堅牢な取引システムへと発展する可能性を秘めています。

- 1