三周期高値安値モメンタム取引戦略

概要

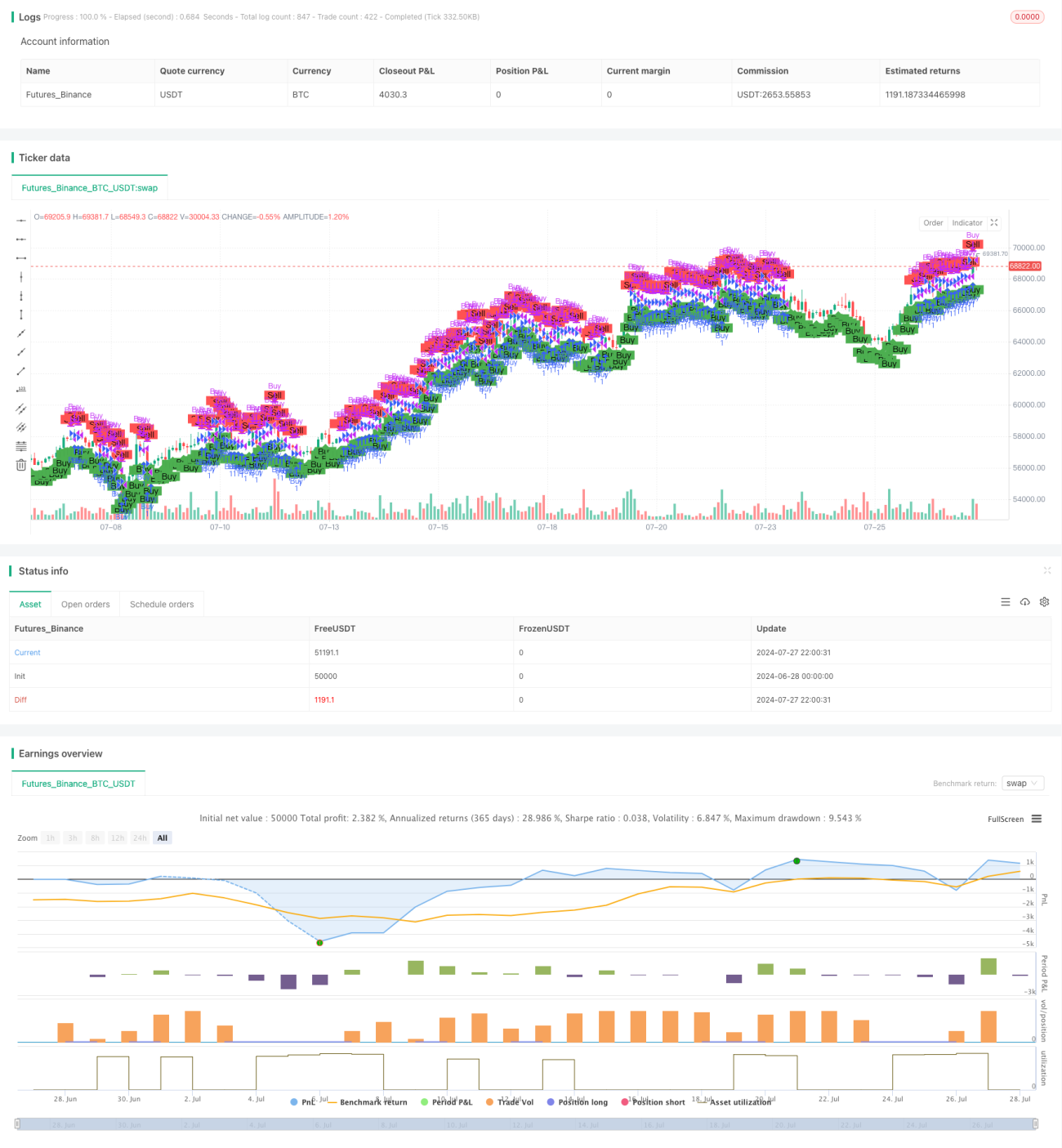

本戦略は、3週間の高値・安値を基にしたモメンタム取引戦略です。直近3週間の価格データを利用して、潜在的な買い・売り機会を特定します。主に、最新高値、最新終値、および3週間前の終値の関係に注目し、これらの価格水準を比較して取引シグナルを生成します。この手法は、短期的な市場ノイズの影響を回避しながら、中期の価格トレンドを捉えることを目的としています。

戦略原理

本戦略の核心原理は、以下の主要要素で構成されます。

-

指標の計算:

- 最新高値:

ta.highest()関数を使用して、直近30取引日(約4週間)の最高値を計算します。 - 最新終値:

close[1]を使用して、前営業日の終値を取得します。 - 3週間前の終値:

close[30]を使用して、30取引日前の終値を取得します。

- 最新高値:

-

買い条件:

- 条件1: 最新高値が3週間前の終値以上であること。

- 条件2: 最新終値が3週間前の終値より大きいこと。

-

売り条件:

- 最新終値が3週間前の終値より大きい場合に売りシグナルをトリガーします。

-

取引執行:

- 買いシグナルがトリガーされた場合、ロングポジションをエントリーします。

- 売りシグナルがトリガーされた場合、現在のロングポジションを決済します。

-

可視化:

plotshape()関数を使用して、チャート上に買い・売りシグナルをマークします。

この設計は、価格が3週間前の水準を突破したときの上昇モメンタムを捉え、価格が戻ったときに迅速にポジションを決済して利益を保護することを目的としています。

戦略の優位性

-

中期トレンドの捕捉: 現在の価格と3週間前の価格水準を比較することで、中期トレンドの形成と継続を効果的に識別できます。

-

ノイズフィルタリング: 3週間の時間枠を使用することで、短期的な市場変動をフィルタリングし、シグナルの信頼性を高めます。

-

動的適応: 最新の価格データに基づいて判断基準を継続的に更新し、市場の変化に動的に適応します。

-

リスク管理: 明確な売り条件を設定することで、市場の転換時に迅速にポジションを決済し、リスクを効果的にコントロールします。

-

シンプルで理解しやすい: 戦略のロジックは直感的で、実装が容易であり、初心者から経験豊富なトレーダーまで適しています。

-

可視化サポート: チャート上に売買シグナルを明確にマークするため、トレーダーは直感的に判断し、バックテスト分析を行うことができます。

戦略のリスク

-

偽ブレイクアウトのリスク: レンジ相場では、頻繁な偽ブレイクアウトが発生し、過剰な取引と不必要な手数料損失を引き起こす可能性があります。

-

ラグ: 3週間の過去データに依存するため、急激な市場変動時にシグナルが遅れ、最適なエントリーのタイミングを逃す可能性があります。

-

単一時間枠の限界: 3週間のデータのみに依存するため、他の時間枠の重要な市場情報を見落とす可能性があります。

-

ストップロスメカニズムの欠如: 現在の戦略には明確なストップロスメカニズムがなく、市場の急激な変動時に大きな損失を被る可能性があります。

-

終値への過度な依存: 主に終値に基づいて判断するため、日中重要価格変動を見逃す可能性があります。

-

出来高確認の欠如: 出来高要因を考慮していないため、低出来高期間に誤ったシグナルが発生する可能性があります。

戦略の最適化方向

-

マルチタイムフレーム分析: 日足、週足、月足など複数の時間枠のデータを統合し、より包括的な市場視点を提供します。

-

出来高指標の導入: 出来高分析を組み合わせることで、特にブレイクアウト確認時のシグナル信頼性を向上できます。

-

動的ストップロスメカニズム: トレーリングストップやATRベースのストップなど、適応型ストップロス戦略を実装し、リスク管理を強化します。

-

シグナルフィルター: RSIやMACDなどの追加テクニカル指標や市場センチメント指標を追加し、誤シグナルを削減します。

-

エントリー最適化: 成行注文ではなく、指値注文や観察レンジの使用を検討し、より良い約定価格を追求します。

-

ポジション管理: 市場ボラティリティとアカウントリスクに応じて、取引ごとのポジションサイズを調整する動的ポジション管理戦略を実装します。

-

市場状態認識: 市場状態(トレンド、レンジ、高ボラティリティ)を識別するロジックを追加し、異なる市場環境で異なる取引パラメータを採用します。

-

バックテストと最適化: 大量の過去データを用いたバックテストを実施し、時間枠や条件閾値などの戦略パラメータを最適化します。

まとめ

3週間高値・安値モメンタム取引戦略は、シンプルでありながら効果的な中期トレンドフォロー手法です。最新高値、最新終値、3週間前の終値を比較することで、価格のブレイクアウトやモメンタム変化を捉えます。その優位性は、短期的なノイズをフィルタリングし、中期トレンドを捉えられること、そしてロジックがシンプルで理解しやすい点にあります。しかし、偽ブレイクアウト、シグナルの遅延、リスク管理の不足といった課題も存在します。

今後の最適化の方向性としては、マルチタイムフレーム分析、出来高確認、動的リスク管理、市場状態認識などに注目すべきです。これらの改善により、戦略は様々な市場環境でより安定的に機能し、トレーダーに信頼性の高い意思決定サポートを提供できる可能性があります。

全体として、本戦略は定量取引の良い出発点を提供し、継続的な最適化と改善により、強力な取引ツールとなる可能性があります。ただし、投資家は実際の応用に際して慎重に行動し、市場リスクを十分に認識し、自身のリスク許容度と投資目標に基づいて戦略を使用する必要があります。

-

リスク管理:明確な売却条件により、市場が反転した際にポジションを迅速にクローズし、リスクを効果的にコントロールできます。

-

シンプルでわかりやすい:戦略のロジックは直感的で、理解と実装が容易であり、初心者から経験豊富なトレーダーまで適しています。

-

視覚的サポート:買いシグナルと売りシグナルがチャート上に明確に表示され、トレーダーが直感的に判断し、バックテスト分析を行うのに便利です。

戦略のリスク

-

偽ブレイクアウトのリスク:レンジ相場では、頻繁な偽ブレイクアウトが発生する可能性があり、過剰な取引や不要な取引手数料の損失につながります。

-

遅延性:3週間の履歴データを使用するため、シグナルに遅延が生じる可能性があり、急激な市場変動時に最適なエントリーポイントを逃す恐れがあります。

-

単一時間枠の制限:3週間のデータのみに依存すると、他の時間枠の重要な市場情報を見落とす可能性があります。

-

ストップロスメカニズムの欠如:現在の戦略には明確なストップロスメカニズムがなく、市場の激しい変動時に大きな損失を被る可能性があります。

-

終値への過度な依存:戦略は主に終値に基づいて判断しており、重要な日中価格変動を無視する可能性があります。

-

出来高確認の欠如:出来高要因を考慮していないため、取引量が少ない期間に偽のシグナルが発生する可能性があります。

戦略の最適化方向性

-

マルチタイムフレーム分析:日足、週足、月足など複数の時間枠のデータを統合し、より包括的な市場展望を提供します。

-

出来高指標の組み込み:出来高分析を組み合わせることで、特にブレイクアウトの確認において、シグナルの信頼性を向上させることができます。

-

動的ストップロスメカニズム:トレーリングストップやATRベースのストップなど、適応型のストップロス戦略を導入し、リスク管理を改善します。

-

シグナルフィルター:RSIやMACDなどの追加のテクニカル指標や市場センチメント指標を追加し、偽シグナルを減らします。

-

エントリー最適化:成行注文ではなく、指値注文や観察ゾーンを使用してエントリーすることで、より良い執行価格を得ることを検討します。

-

ポジション管理:市場のボラティリティやアカウントリスクに基づいて各取引のサイズを調整する、動的なポジションサイジング戦略を実装します。

-

市場状態認識:市場状態(トレンド、レンジ、高ボラティリティ)を識別するロジックを追加し、異なる市場環境に応じて異なる取引パラメーターを採用します。

-

バックテストと最適化:広範な履歴データのバックテストを実施し、期間や条件のしきい値などの戦略パラメーターを最適化します。

まとめ

3週間高値安値モメンタム取引戦略は、中期トレンドフォローにおけるシンプルながら効果的な手法です。最新の高値、最新の終値、および3週間前の終値を比較することで、価格のブレイクアウトとモメンタムの変化を捉えることができます。その強みは、短期的なノイズをフィルタリングし、中期トレンドを捉え、ロジックがシンプルで理解しやすい点にあります。しかし、この戦略は偽ブレイクアウト、シグナルの遅延、リスク管理の不十分さなどの課題にも直面しています。

今後の最適化方向性は、マルチタイムフレーム分析、出来高確認、動的リスク管理、市場状態認識に焦点を当てるべきです。これらの改善を通じて、戦略はさまざまな市場環境でより堅牢に機能し、トレーダーに信頼性の高い意思決定サポートを提供できる可能性があります。

全体として、この戦略は定量取引の良い出発点を提供します。継続的な最適化と改良により、強力な取引ツールとなる可能性があります。ただし、投資家は実践で適用する際には慎重を期し、市場リスクを十分に認識し、自身のリスク許容度と投資目的に合わせて戦略を使用する必要があります。

- 1