二重コーラルトレンドクロス戦略

1

Follow

1802

Followers

概要

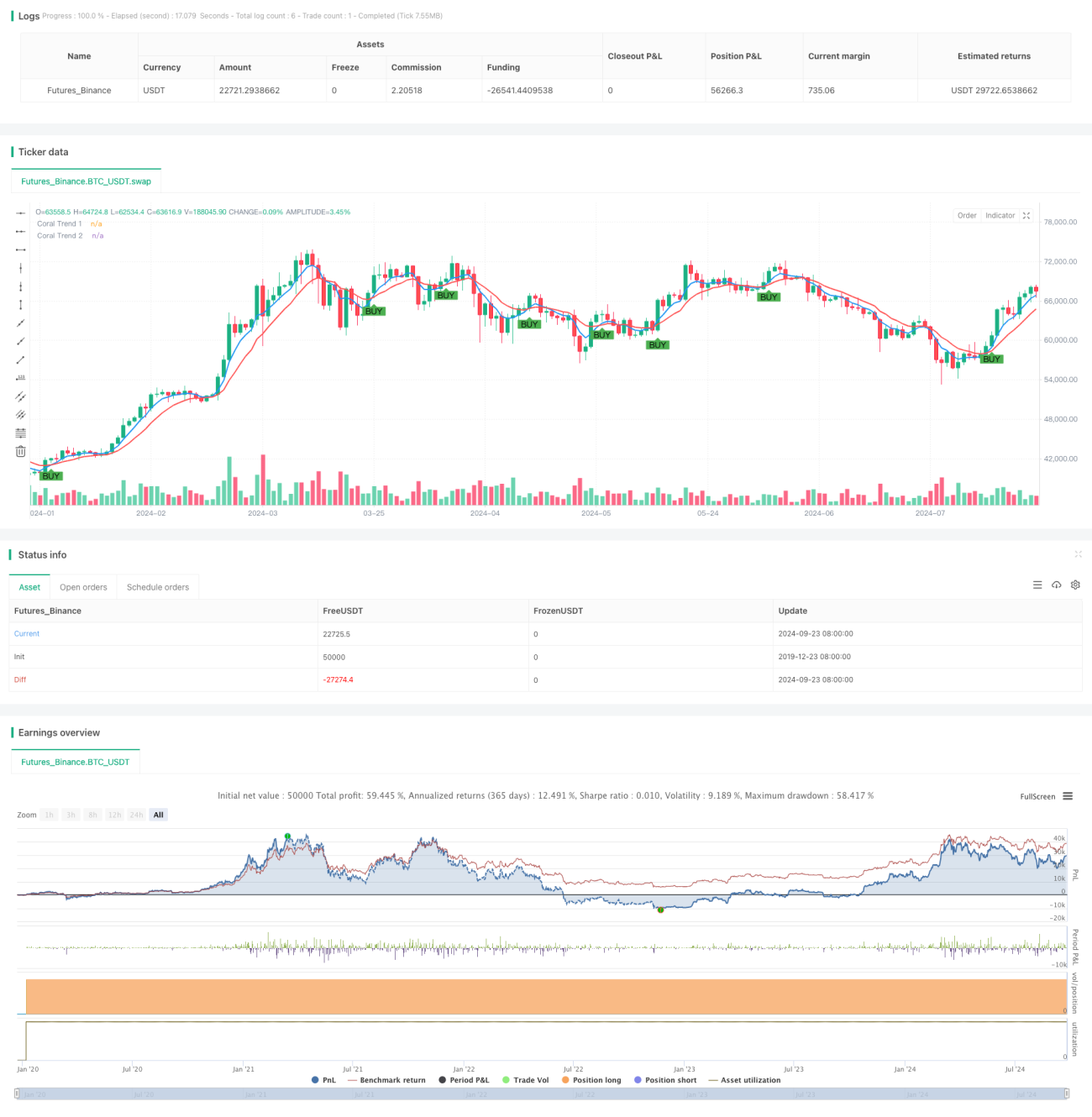

本戦略は、コーラルトレンド指標のクロスに基づく中期・長期取引戦略です。異なるパラメータを持つ2本のコーラルトレンドラインを利用して、潜在的な買い機会を識別します。この戦略は主に1か月足や3か月足などの長期チャートに適用し、大きなトレンドの中での有利な買いポイントを捉えることを目的としています。

戦略の原理

戦略の核は、Coral Trend 1とCoral Trend 2と呼ばれる2本のコーラルトレンドラインを使用することです。各トレンドラインは指数移動平均(EMA)に基づいて計算され、さらに追加の平滑化処理が施されています。Coral Trend 1ラインがCoral Trend 2ラインを下から上にクロスしたとき、システムは買いシグナルを生成します。このクロスは、潜在的な上昇トレンドの始まりと見なされます。

戦略の主要パラメータは以下の通りです:

- 2本のコーラルトレンドラインの平滑化周期

- トレンドラインの感度を調整するための定数D値

これらのパラメータを調整することで、トレーダーはさまざまな市場状況や個人の好みに応じて戦略のパフォーマンスを最適化できます。

戦略の利点

- トレンドフォロー:この戦略は中長期的なトレンドを効果的に捉え、短期的な市場ノイズの影響を軽減します。

- 適応性:コーラルトレンド指標は優れた適応性を持ち、さまざまな市場環境で安定性を維持できます。

- 視認性:戦略はチャート上に買いシグナルを明確に表示するため、トレーダーは取引機会を素早く識別できます。

- パラメータの柔軟性:トレーダーは個人のニーズに応じてパラメータを調整し、異なる取引スタイルや市場環境に対応できます。

- 変動の把握:トレンドラインの変動パターンを観察することで、トレーダーは最適なエントリーのタイミングを選択できます。

戦略のリスク

- 遅延性:トレンドフォロー戦略であるため、トレンド反転の初期段階で遅れが生じる可能性があります。

- 偽のブレイクアウト:レンジ相場では、頻繁な偽のブレイクアウトシグナルが発生する可能性があります。

- パラメータ感度:戦略のパフォーマンスはパラメータ設定に敏感であり、不適切なパラメータは過剰取引や機会損失につながる可能性があります。

- 市場環境への依存:急激な変動や急速な反転が発生する市場では、戦略のパフォーマンスが低下する可能性があります。

戦略の最適化方向性

- フィルターの追加:追加のテクニカル指標や市場心理指標を導入し、偽シグナルを減らします。

- 動的パラメータ調整:市場のボラティリティに応じてパラメータを自動調整する適応メカニズムを開発します。

- マルチタイムフレーム分析:より短い時間足とより長い時間足のシグナルを組み合わせて、エントリーの精度を向上させます。

- ストップロスとテイクプロフィットの追加:合理的なリスク管理メカニズムを設計し、利益を保護し損失を制限します。

- バックテストの最適化:異なる市場や期間について包括的なバックテストを実施し、最適なパラメータの組み合わせを特定します。

まとめ

デュアルコーラルトレンドクロス戦略は、中長期的な市場トレンドを捉えるための効果的なツールです。異なるパラメータを持つ2本のコーラルトレンドラインのクロスを利用することで、安定性を維持しながらさまざまな市場環境に適応できます。遅延性や偽のブレイクアウトなどの固有のリスクはありますが、注意深いパラメータ最適化と追加のリスク管理措置により、トレーダーは戦略の信頼性と収益性を大幅に向上させることができます。今後の最適化の方向性としては、シグナル品質の向上、適応性の強化、リスク管理の完成に重点を置き、より包括的で堅牢な取引システムを構築することが重要です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1