EMA指標に基づくクロス市場のロング・ショートトレンド・オーバーナイトポジション戦略

1

Follow

1802

Followers

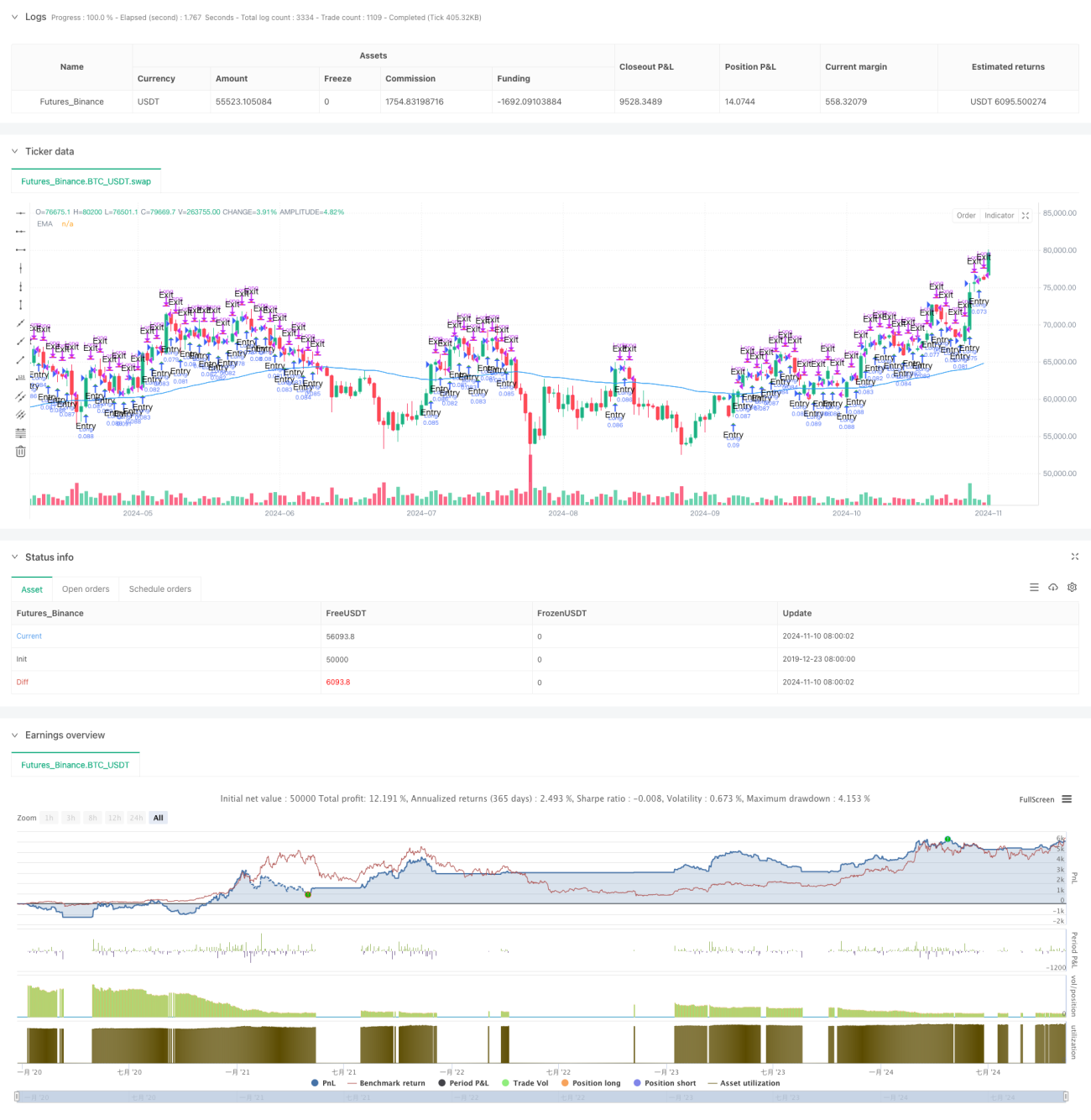

本戦略は、EMAテクニカル指標に基づいたクロスマーケットのオーバーナイトホールド戦略であり、市場の引け前と寄付後の取引機会を捉えることを目的としています。戦略は、精密な時間制御とテクニカル指標フィルタリングにより、異なる市場環境下でのスマートな取引を実現します。

戦略概要

この戦略は、主に市場の引け前の特定の時間にエントリーし、翌日の寄付後の特定の時間にエグジットすることで収益を得ます。EMA指標をトレンド確認として組み合わせ、複数のグローバル市場で取引機会を探ります。また、自動売買機能を統合し、無人運用を実現しています。

戦略原理

- 時間制御:各市場の取引時間に応じて、引け前の固定時間にエントリー、寄付後の固定時間にエグジットします。

- EMAフィルタリング:オプションのEMA指標を使用してエントリーシグナルを検証します。

- 市場選択:米国、アジア、欧州の3大市場の取引時間に適応可能です。

- 週末保護:金曜日の引け前に強制的にポジションをクローズし、週末のポジション保有リスクを回避します。

戦略の利点

- マルチマーケット適応性:異なる市場特性に応じて取引時間を柔軟に調整できます。

- リスク管理の充実:週末のポジションクローズ保護メカニズムを含みます。

- 自動化レベルの高さ:自動売買インターフェースとの接続をサポートします。

- パラメータの柔軟な調整:取引時間とテクニカル指標のパラメータをカスタマイズ可能です。

- 取引コストの考慮:手数料とスリッページ設定を含みます。

戦略リスク

- 市場変動リスク:オーバーナイトホールドはギャップ変動リスクに直面する可能性があります。

- 時間依存性:戦略効果は市場時間帯の選択に影響されます。

- テクニカル指標の限界:単一のEMA指標は遅れる可能性があります。

推奨:ストップロスを設定し、より多くのテクニカル指標で検証を追加すること。

戦略最適化の方向性

- より多くのテクニカル指標の組み合わせを追加

- ボラティリティフィルタリングメカニズムを導入

- エントリー・エグジット時間の選択を最適化

- 適応型パラメータ調整機能を追加

- リスク管理モジュールを強化

まとめ

本戦略は、精密な時間制御とテクニカル指標フィルタリングにより、信頼性の高いオーバーナイト取引システムを実現しています。戦略設計では、マルチマーケット適応、リスク管理、自動売買などの実戦ニーズを総合的に考慮し、実用性の高い価値を備えています。継続的な最適化と改善により、本戦略は実取引において安定した収益を上げることが期待されます。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy, titled "Overnight Market Entry Strategy with EMA Filter," is designed for entering long positions shortly before Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1