RSI動的ストップロススマートトレーディング戦略

1

Follow

1802

Followers

概要

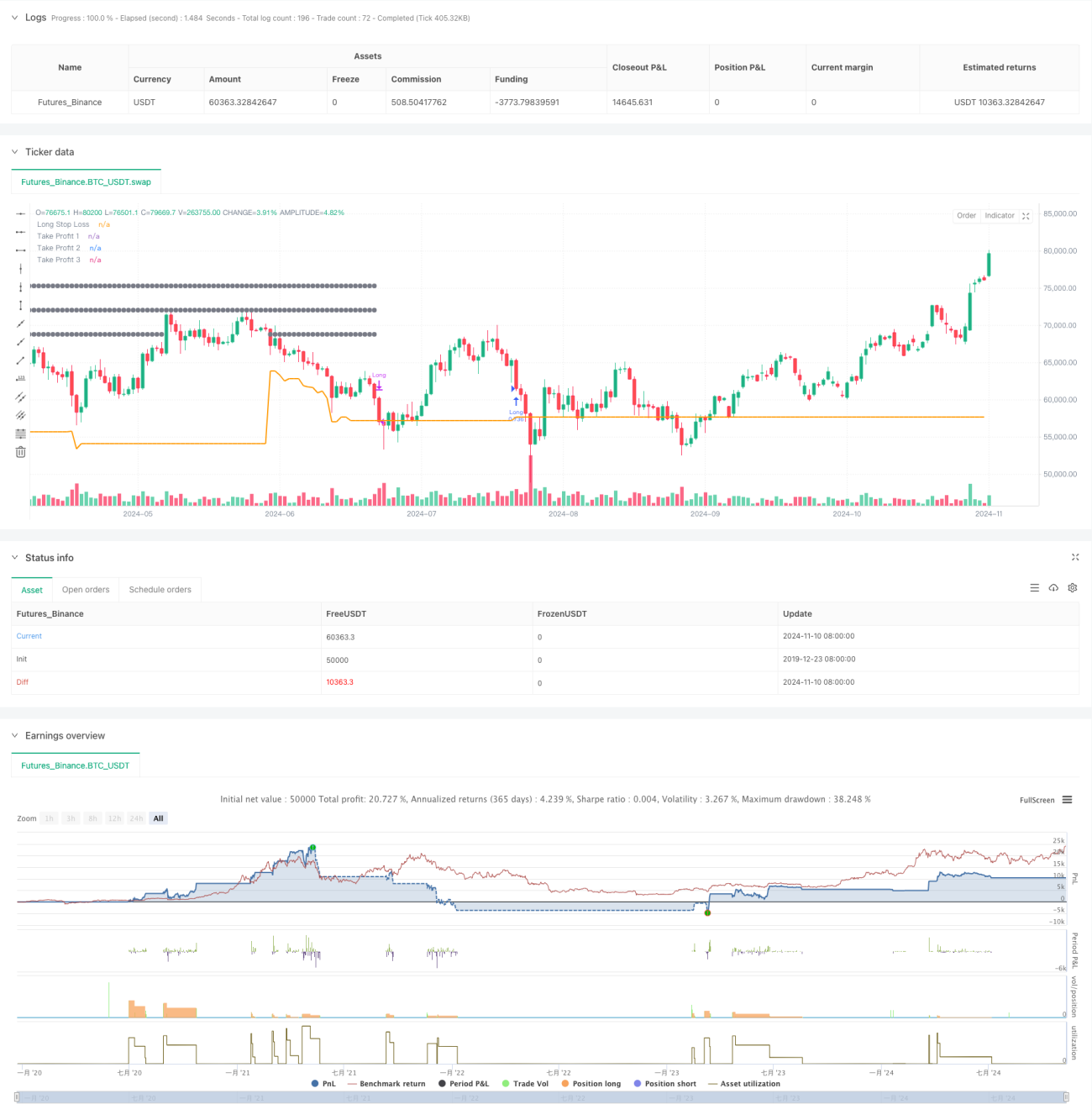

本戦略は、RSI指標に基づく動的ストップロストレーディングシステムであり、SMA移動平均線とATRボラティリティ指標を組み合わせて取引判断を最適化します。戦略は多層的な利確プランを採用し、ピラミッド型のポジション決済によって利益を最大化すると同時に、ATR動的ストップロスでリスクをコントロールします。市場の変動に応じて取引パラメータを自動調整する高い適応性を備えています。

戦略原理

本戦略は主にRSIの売られ過ぎゾーン(RSI<30)をエントリーシグナルとし、価格が200日移動平均線より上にあることを条件に、上昇トレンドにあることを確認します。システムは3段階の利確目標(5%、10%、15%)とATR動的ストップロスを組み合わせています。具体的には:

- エントリー条件:RSIが30未満、かつ価格がSMA200より上

- ポジション管理:1回のエントリーで資金の75%を使用

- ストップロス設定:1.5倍ATR値に基づく動的ストップロス

- 利確戦略:それぞれ5%、10%、15%の位置に3段階の利確ポイントを設定し、33%、66%、100%の割合で段階的に決済

戦略の優位性

- 動的リスク管理:ATRによる市場変動への適応

- 段階的利確:感情の影響を軽減し、利益を得る確率を向上

- トレンド確認:移動平均線を利用した偽シグナルのフィルタリング

- 資金管理:割合ベースのポジションサイジングにより、異なる口座規模に対応

- 手数料最適化:取引コストを考慮し、実際の取引に近い形を実現

戦略のリスク

- 移動平均線の遅延性によりエントリーが遅れる可能性

- RSIの売られ過ぎが必ずしも反転を意味しない

- 大口ポジションは大きなドローダウンを招く可能性

- 頻繁な段階的利確により取引コストが増加する可能性

これらのリスクは、パラメータ調整やフィルター条件の追加により管理することが推奨されます。

戦略の最適化方向

- 出来高確認シグナルの追加

- トレンド強度指標の導入

- 利確比率配分の最適化

- 時間周期フィルターの追加

- ボラティリティ適応型ポジション管理の検討

まとめ

本戦略は、テクニカル指標と動的リスク管理を組み合わせることで、比較的完成度の高いトレーディングシステムを構築しています。その優位性は適応性の高さとリスクのコントロール性にありますが、実際の市場状況に応じたパラメータ最適化が必要です。本戦略は中長期の投資家に適しており、システムトレードの良い出発点となり得ます。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA/4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © wielkieef

//@version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1