1

Follow

1802

Followers

概要

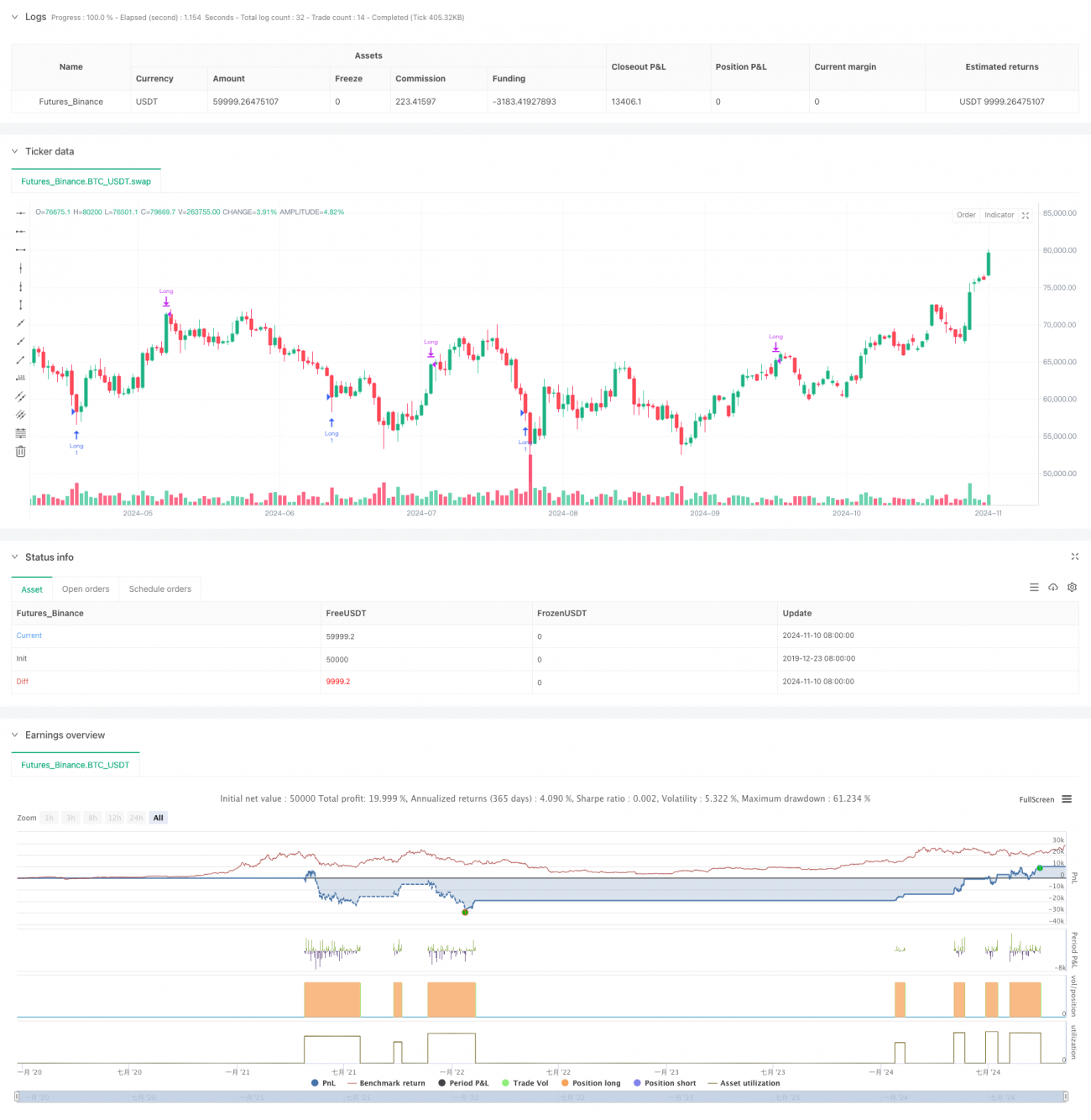

本戦略は、ボリンジャーバンド、RSIインジケーター、移動平均線を組み合わせた総合取引システムです。ボリンジャーバンドによる価格変動範囲、RSIの買われすぎ・売られすぎ水準、EMAトレンドフィルターを活用して潜在的な取引機会を特定します。ロングとショートの両方の取引をサポートし、資金を保護するための複数のエグジットメカニズムを提供します。

戦略の原理

戦略は主に以下のコアコンポーネントに基づいています:

- 1.8倍標準偏差のボリンジャーバンドを使用して価格変動範囲を特定

- 7期間のRSIインジケーターで買われすぎ・売られすぎを判断

- オプションの500期間EMAをトレンドフィルターとして使用

- エントリー条件:

- ロング: RSIが25未満、かつ価格がボリンジャーバンド下限を突破

- ショート: RSIが75超、かつ価格がボリンジャーバンド上限を突破

- エグジット方式はRSI閾値またはボリンジャーバンドの逆突破に対応

- オプションのパーセンテージストップロスによる保護

戦略のメリット

- 複数のテクニカル指標の連携によりシグナルの信頼性が向上

- 柔軟なパラメーター設定により様々な市場環境に対応可能

- 双方向取引をサポートし、市場機会を十分に捉える

- 異なる取引スタイルに適応する複数のエグジットメカニズムを提供

- トレンドフィルター機能により偽シグナルを効果的に低減

- ストップロスメカニズムにより優れたリスク管理を実現

戦略のリスク

- レンジ相場では頻繁な偽シグナルが発生する可能性がある

- 複数の指標によりシグナルが遅延する可能性がある

- 固定されたRSI閾値は市場環境によっては柔軟性に欠ける

- ボリンジャーバンドのパラメーターは市場のボラティリティに応じて調整が必要

- 急激な価格変動時にストップロスが容易に発動される可能性がある

戦略の最適化方向性

- 市場のボラティリティに応じて動的に調整する適応型ボリンジャーバンド乗数の導入

- 出来高インジケーターを補助確認として追加

- 特定時間帯の取引を避ける時間フィルターの追加を検討

- 動的RSI閾値システムの開発

- より多くのトレンド確認インジケーターの統合

- 動的ストップロスを考慮したストップロスメカニズムの最適化

まとめ

これは設計が整った定量取引戦略であり、複数のテクニカル指標を組み合わせて市場機会を捉えます。戦略の設定柔軟性が高く、様々な取引ニーズに対応できます。固有のリスクは存在するものの、パラメーター最適化や補助インジケーターの追加により、その安定性と信頼性をさらに向上させることができます。体系的な取引方法を求める投資家にとって、参考となる戦略フレームワークです。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1