1

Follow

1802

Followers

概要

本戦略は、RSI(相対力指数)に基づく適応型取引システムであり、買われ過ぎ・売られ過ぎの閾値を動的に調整することで、取引シグナルの生成を最適化します。戦略の核となる革新は、Bufi適応型閾値(BAT)手法の導入です。この手法は、市場トレンドと価格変動性に応じてRSIのトリガー閾値を動的に調整し、従来のRSI戦略の有効性を高めます。

戦略の原理

本戦略の核心は、従来の固定閾値RSIシステムを動的閾値システムにアップグレードすることです。具体的な実装方法は以下の通りです。

- 短期間のRSIを使用して市場の買われ過ぎ・売られ過ぎ状態を計算

- 線形回帰により価格トレンドの傾きを計算

- 標準偏差を用いて価格変動の程度を測定

- トレンドと変動情報を統合し、RSI閾値を動的に調整

- 上昇トレンドでは閾値を引き上げ、下降トレンドでは閾値を引き下げ

- 価格が平均から大きく乖離した場合、閾値の感度を低下

本戦略には、以下の2つのリスク管理メカニズムも含まれます。

- 固定期間でのポジション決済メカニズム

- 最大損失ストップロスメカニズム

戦略の利点

-

動的な適応性:

- 市場の状態に応じて取引閾値を自動調整

- 異なる市場環境で固定パラメータを使用する欠点を回避

-

リスク管理の充実:

- 最大保有時間制限を設定

- 資金ストップロス保護メカニズムを内包

- パーセンテージベースのポジション管理を採用

-

シグナル品質の向上:

- レンジ相場での偽シグナルを低減

- トレンド相場での捕捉能力を向上

- 感度と安定性のバランスを最適化

戦略のリスク

-

パラメータ感応性:

- BAT係数の選択が戦略のパフォーマンスに影響

- RSIの期間設定には十分なテストが必要

- 適応長パラメータの最適化が必要

-

市場環境への依存:

- 高変動市場では機会を逃す可能性

- 激しい変動時にはストップロスのスリッページが大きくなる可能性

- 市場に応じてパラメータ調整が必要

-

技術的限界:

- 過去データに依存して閾値を計算

- 遅延が生じる可能性

- 取引コストの影響を考慮する必要あり

戦略の最適化方向

-

パラメータ最適化:

- 適応型パラメータ選択メカニズムの導入

- 異なる市場周期に応じた動的パラメータ調整

- パラメータ自動最適化機能の追加

-

シグナル最適化:

- 他のテクニカル指標との組み合わせによる検証

- 市場周期識別機能の追加

- エントリータイミング判断の最適化

-

リスク管理最適化:

- 動的ストップロスメカニズムの導入

- ポジション管理戦略の最適化

- ドローダウン制御メカニズムの追加

まとめ

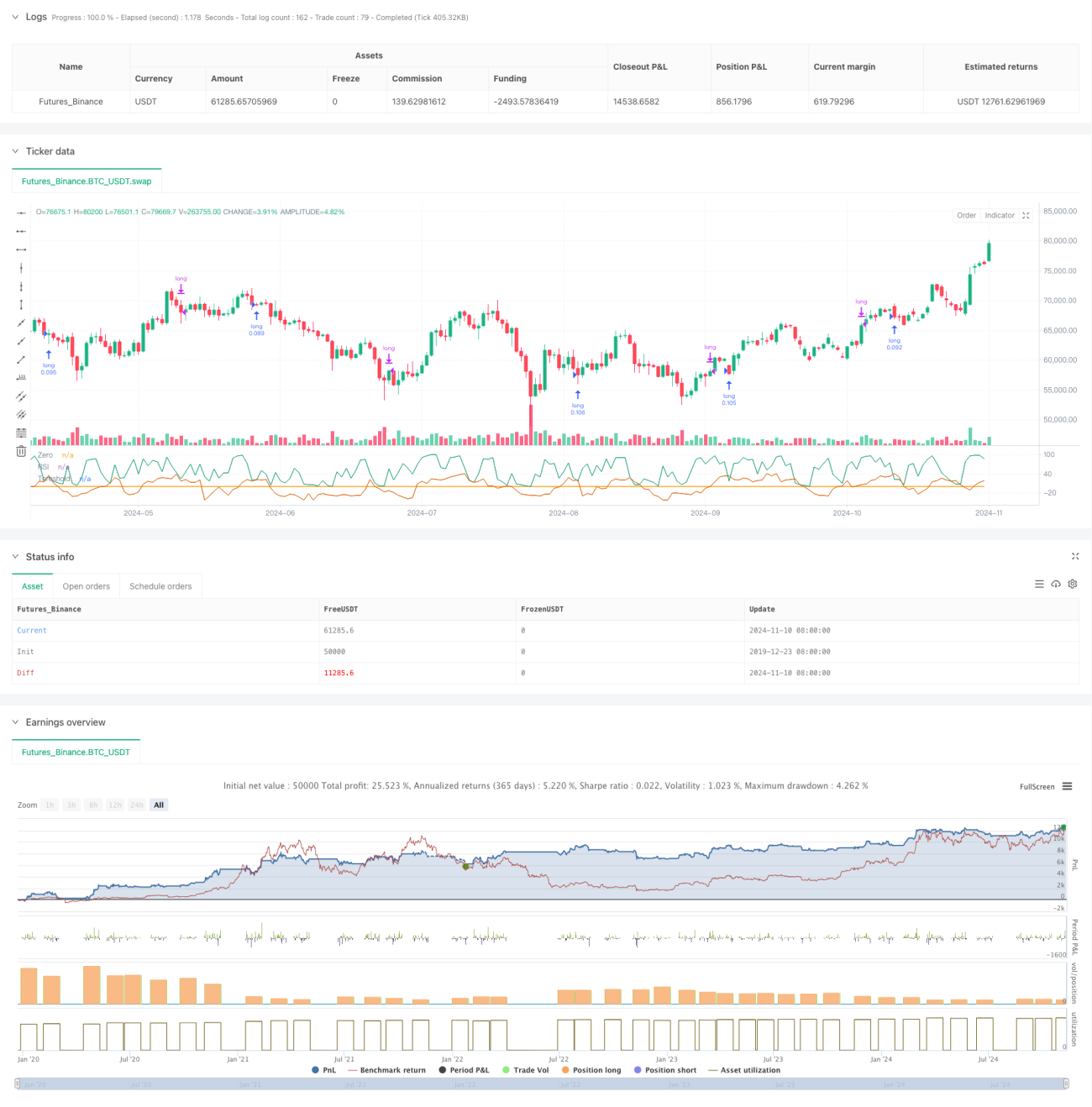

本戦略は、動的閾値最適化により従来のRSI戦略の限界を解決した、革新的な適応型取引戦略です。市場トレンドと変動性を総合的に考慮し、高い適応性とリスク管理能力を備えています。パラメータ最適化などの課題はあるものの、継続的な改善と最適化により、実取引で安定したパフォーマンスを発揮することが期待されます。実運用前に十分なバックテストとパラメータ最適化を行い、各市場の特性に応じて適切に調整することを推奨します。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PineCodersTASC

// TASC Issue: October 2024Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1