ダブルMACDプライスアクション・ブレイクアウト追跡戦略

1

Follow

1802

Followers

概要

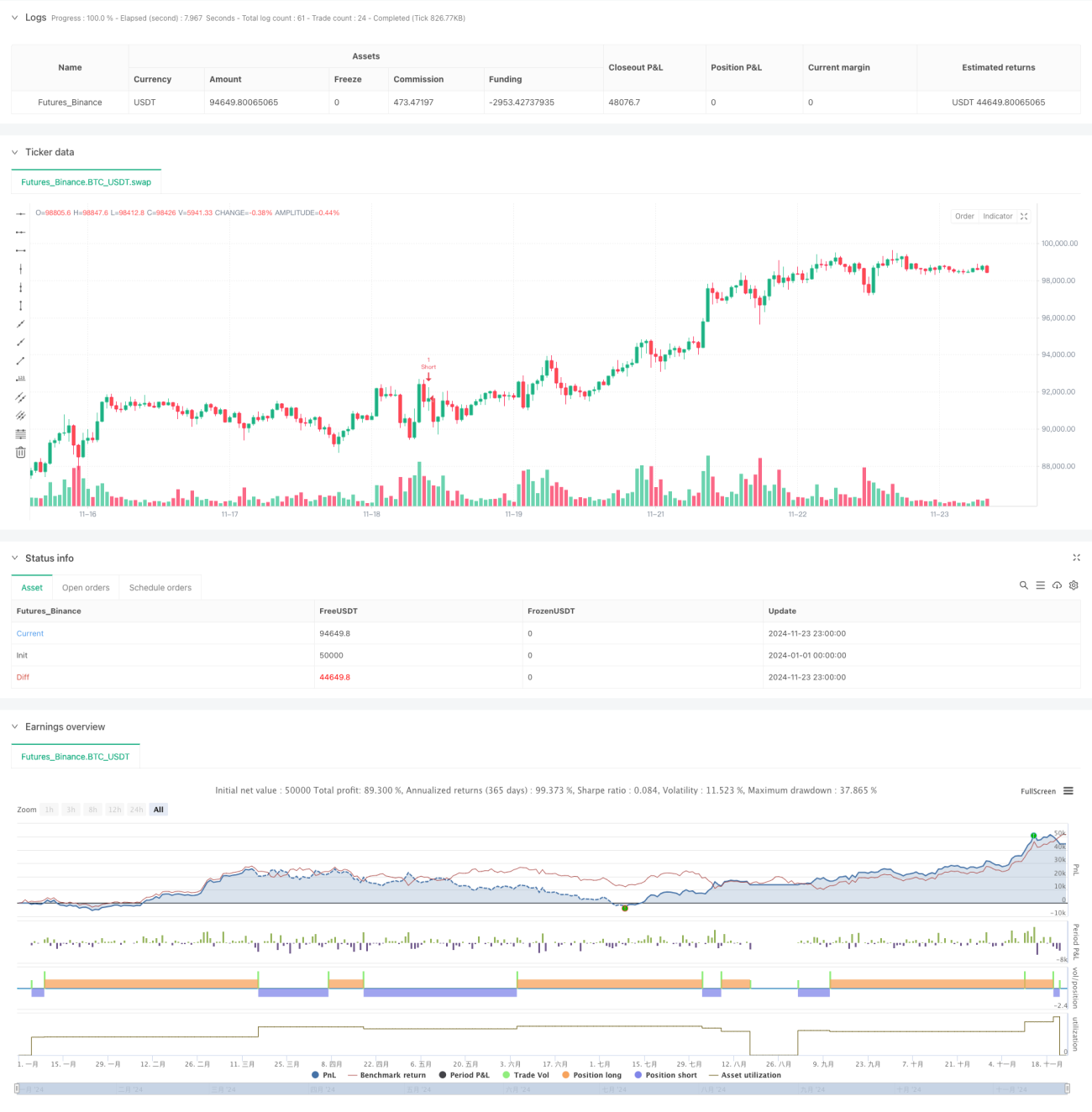

これは、二重MACD指標と価格アクション分析を組み合わせた取引戦略です。この戦略は、15分足での二重MACDヒストグラムの色の変化を観察して市場のトレンドを判断し、同時に5分足で強いローソク足のパターンを探し、1分足でブレイクアウトのシグナルを確認します。ATRに基づく動的ストップロスとトレーリングテイクプロフィットの仕組みを採用し、リスクを効果的に管理しながら利益を最大化します。

戦略の原理

この戦略は、異なるパラメーターを持つ2組のMACD指標(34/144/9および100/200/50)を使用して市場トレンドを確認します。両方のMACDヒストグラムが同じ色のトレンドを示した場合、システムは5分足で強いローソク足パターンを探します。このパターンは、実体がひげの1.5倍以上であることが特徴です。強いローソク足が見つかると、システムは1分足でのブレイクアウトを監視します。上昇トレンドで高値をブレイクするか、下降トレンドで安値をブレイクした場合にポジションを開きます。ストップロスはATR指標に基づいて設定され、同時にATRの1.5倍を動的トレーリングテイクプロフィットとして使用します。

戦略の優位性

- マルチタイムフレーム分析:15分足、5分足、1分足の3つの時間枠を組み合わせ、シグナルの信頼性を向上

- トレンド確認:二重MACDによるクロス確認で偽シグナルを低減

- 価格アクション分析:強いローソク足パターンにより重要な価格水準を識別

- 動的リスク管理:ATRに基づく適応的ストップロスとトレーリングテイクプロフィットの仕組み

- シグナルフィルター:厳格なエントリー条件により誤取引を低減

- 自動化の高さ:完全自動取引により人的介入を削減

戦略のリスク

- トレンド反転リスク:大幅変動市場では偽のブレイクアウトが発生する可能性

- スリッページリスク:1分足での高頻度取引によりスリッページの影響を受ける可能性

- 過剰取引リスク:頻繁なシグナルによる過剰取引の可能性

- 市場環境依存性:レンジ相場ではパフォーマンスが低下する可能性

緩和策:

- トレンドフィルターの追加

- 最小変動閾値の設定

- 取引回数制限の追加

- 市場環境識別メカニズムの導入

戦略の最適化方向性

- MACDパラメーター最適化:市場特性に応じてMACDパラメーターを調整可能

- ストップロス最適化:ボラティリティに基づく動的ストップロスの追加を検討

- 取引時間フィルター:取引時間枠制限の追加

- ポジション管理:分割建てと決済の仕組みの実装

- 市場環境フィルター:トレンド強度指標の追加

- ドローダウン管理:エクイティカーブに基づくリスク制御メカニズムの導入

まとめ

これはテクニカル分析とリスク管理を統合した戦略システムです。マルチタイムフレーム分析と厳格なシグナルフィルターにより取引品質を確保し、同時に動的ストップロスとトレーリングテイクプロフィットでリスクを効果的に管理します。この戦略は高い適応性を持ちますが、市場環境に応じて継続的な最適化が必要です。実運用では、事前に十分なバックテストとパラメーター最適化を行い、市場特性に合わせた調整を行うことを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1