1

Follow

1802

Followers

概要

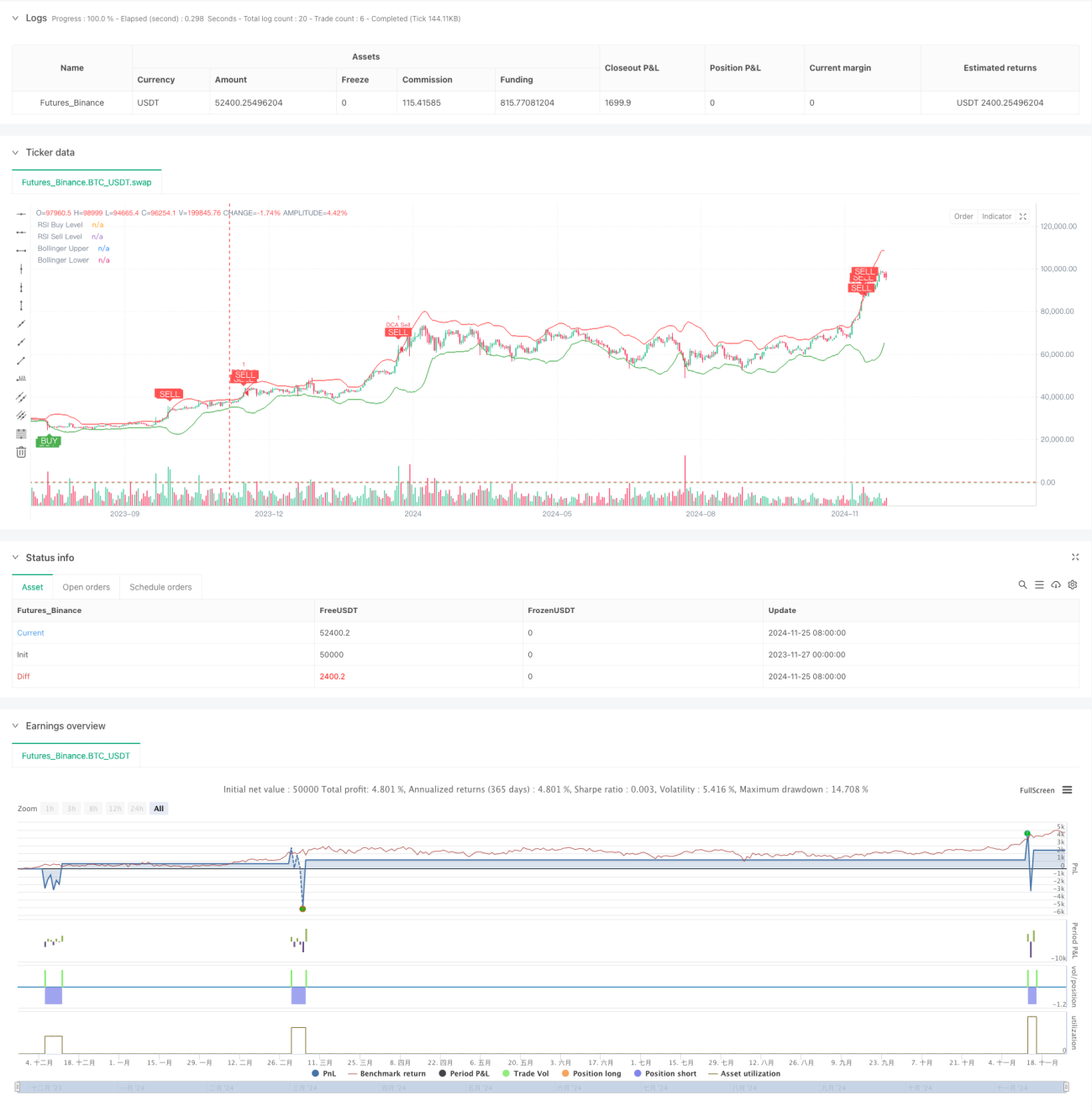

本戦略は、ボリンジャーバンド(Bollinger Bands)、相対力指数(RSI)、およびドルコスト平均法(DCA)を組み合わせた定量取引システムです。資金管理ルールを設定し、市場の変動の中で自動的に段階的なポジション構築を実行するとともに、テクニカル指標を用いて売買シグナルを判断し、リスクをコントロールしながら取引を実行します。また、利益確定ロジックと累積損益トラッキング機能を備えており、取引パフォーマンスを効果的に監視・管理できます。

戦略の原理

本戦略は、主に以下のコアコンポーネントに基づいて動作します。

- ボリンジャーバンドは価格の変動範囲を判断するために使用され、価格が下限に達した場合は買い、上限に達した場合は売りを検討します。

- RSIは市場の買われ過ぎ・売られ過ぎ状態を確認するために使用され、RSIが25未満の場合は売られ過ぎ、75超の場合は買われ過ぎと判断します。

- DCAモジュールは、口座残高に応じて各購入額を動的に計算し、資金の適応的管理を実現します。

- 利益確定モジュールは5%の利益目標を設定し、目標達成時に自動的にポジションをクローズして利益を確保します。

- 市場状態監視モジュールは、90日間の市場変動幅を計算し、全体のトレンド判断に役立てます。

- 累積損益トラッキングモジュールは、各取引の損益状況を記録し、戦略のパフォーマンス評価を容易にします。

戦略の利点

- 複数のテクニカル指標を組み合わせたクロス確認により、シグナルの信頼性が向上します。

- 動的なポジション管理を採用し、固定ポジションによるリスクを回避します。

- 適切な利益確定条件を設定し、利益をタイムリーに確定します。

- 市場トレンド監視機能を備え、大局観を把握しやすくなります。

- 充実した損益追跡システムにより、戦略のパフォーマンス分析が容易です。

- アラート機能が充実しており、取引機会をリアルタイムで通知できます。

戦略のリスク

- レンジ相場ではシグナルが頻繁に発生し、取引コストが増加する可能性があります。

- RSIはトレンド相場において遅延が生じる可能性があります。

- 固定の利益確定率では、強いトレンド相場で早すぎるエグジットにつながる可能性があります。

- DCA戦略は一方的な下落相場において大きなドローダウンを引き起こす可能性があります。

リスク管理として以下の対策が推奨されます。

- 最大保有ポジション制限を設定する

- 市場のボラティリティに応じてパラメータを動的に調整する

- トレンドフィルターを追加する

- 段階的な利益確定戦略を導入する

戦略の最適化方向

-

パラメータ動的最適化:

- ボリンジャーバンドのパラメータをボラティリティに応じて適応調整

- RSIの閾値を市場サイクルに応じて変更

- DCAの資金比率を口座規模に追従して調整

-

シグナルシステムの強化:

- 出来高確認を追加

- トレンドライン分析を追加

- より多くのテクニカル指標のクロス確認を組み合わせる

-

リスク管理の充実:

- 動的ストップロスを実装

- 最大ドローダウンの制御を追加

- 1日の損失制限を設定

まとめ

本戦略は、テクニカル分析と資金管理手法を総合的に活用し、比較的完成度の高い取引システムを構築しています。複数のシグナル確認と充実したリスク管理が利点ですが、実戦で十分なテストと最適化が必要です。パラメータ設定の継続的な改善と補助指標の追加により、本戦略は実際の取引で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

/*backtest

start: 2023-11-27 00:00:00

end: 2024-11-26 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Combined BB RSI with Cumulative Profit, Market Change, and Futures Strategy (DCA)", shorttitle="BB RSI Combined DCA Strategy", overlay=true)

// Input ParametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1