高度なダブル移動平均線モメンタムトレンドフォロートレーディングシステム

1

Follow

1802

Followers

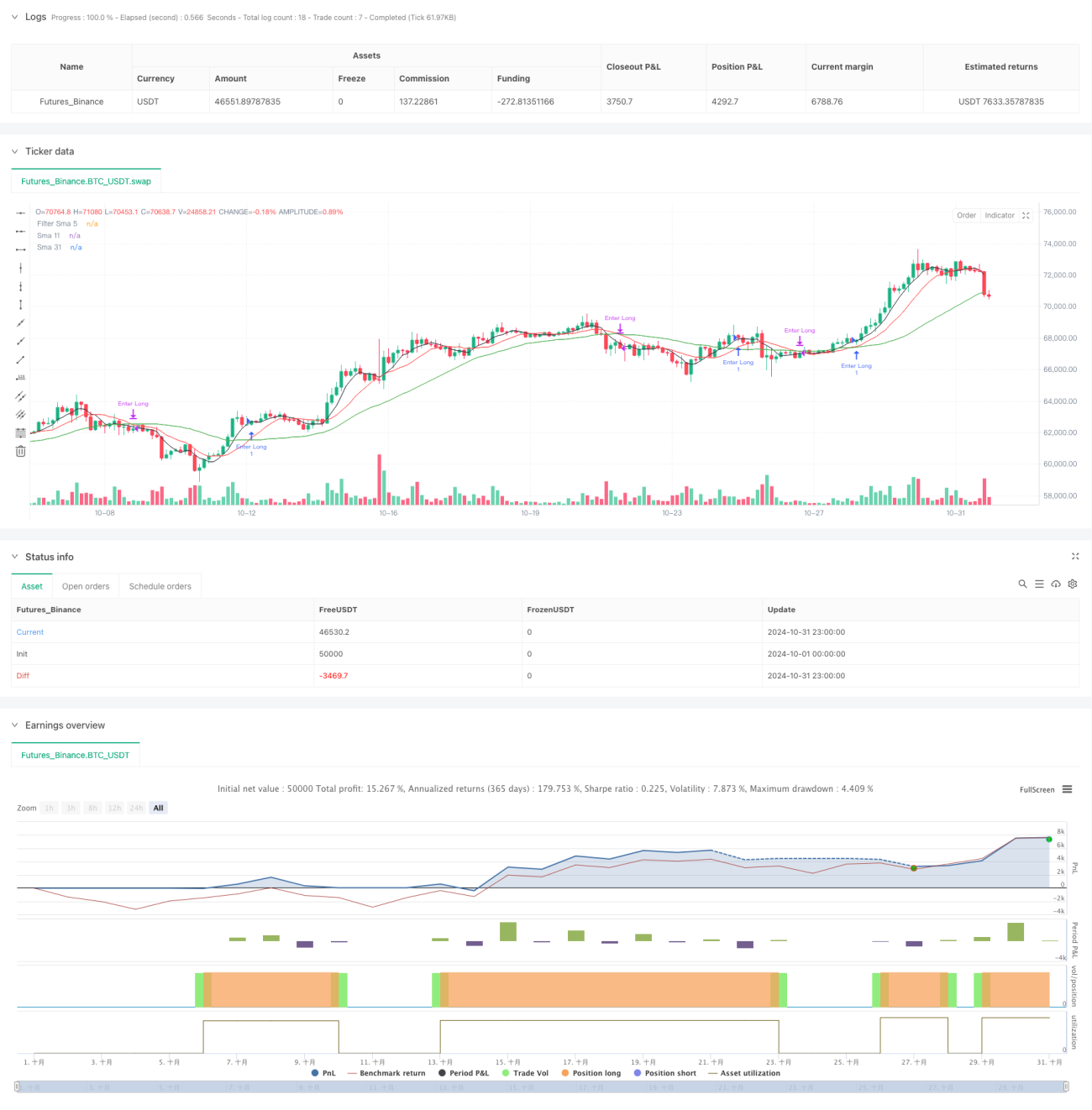

本戦略は、二重移動平均線システムに基づくモメンタム・トレンド追従戦略であり、短期移動平均線と長期移動平均線のクロスシグナルを組み合わせ、さらにフィルター用移動平均線を導入してエントリータイミングを最適化し、資金管理とリスクコントロールにより安定した取引効果を実現します。

戦略の原理

本戦略では、11期間と31期間の単純移動平均線(SMA)を主要なシグナルシステムとして採用し、同時に5期間移動平均線をフィルターとして使用します。短期線(SMA11)が長期線(SMA31)を上抜け、かつ価格がフィルター移動平均線より上にある場合に買いシグナルが発生し、短期線が長期線を下抜けた場合にポジションをクローズします。本戦略は、固定資金量を設定することで各取引の規模を制御し、リスク管理を実現します。

戦略のメリット

- シグナルシステムがシンプルかつ明確で、理解・実行が容易

- 複数移動平均線による確認で、偽シグナルを効果的に除去可能

- 固定資金量での取引により、リスクをコントロール可能

- 優れたトレンド追従能力を備える

- エントリーとエグジットのロジックが明確で、判断に迷いが生じにくい

- 様々な市場環境に適応可能

戦略のリスク

- レンジ相場では取引頻度が高くなる可能性がある

- 移動平均線システムには一定の遅延が存在する

- 固定資金量での取引では、資金効率を十分に活用できない可能性がある

- 市場のボラティリティ変化を考慮していない

- ストップロス機構がなく、大きなドローダウンリスクに直面する可能性がある

戦略の改善方向

- 適応型移動平均線期間を導入し、市場のボラティリティに応じて動的に調整

- ボラティリティフィルターを追加し、高ボラティリティ環境でポジションサイズを調整

- 動的な資金管理システムを設計し、資金使用効率を向上

- ストップロスとテイクプロフィットの仕組みを追加し、1回の取引リスクを管理

- トレンド強度指標を導入し、エントリータイミングを最適化

- 取引時間フィルターを追加し、不利な時間帯の取引を回避

まとめ

本戦略は、複数の移動平均線システムを用いて比較的安定したトレンド追従システムを構築しています。いくつかの固有の限界はあるものの、適切な最適化と改善により、戦略の安定性と収益性をさらに高めることができます。トレーダーは実運用にあたり、市場の具体的な状況を考慮してパラメータを調整することを推奨します。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1