多重テクニカル指標トレンドフォロー戦略と雲図ブレイクアウト及びストップロスシステムの組み合わせ

1

Follow

1802

Followers

概要

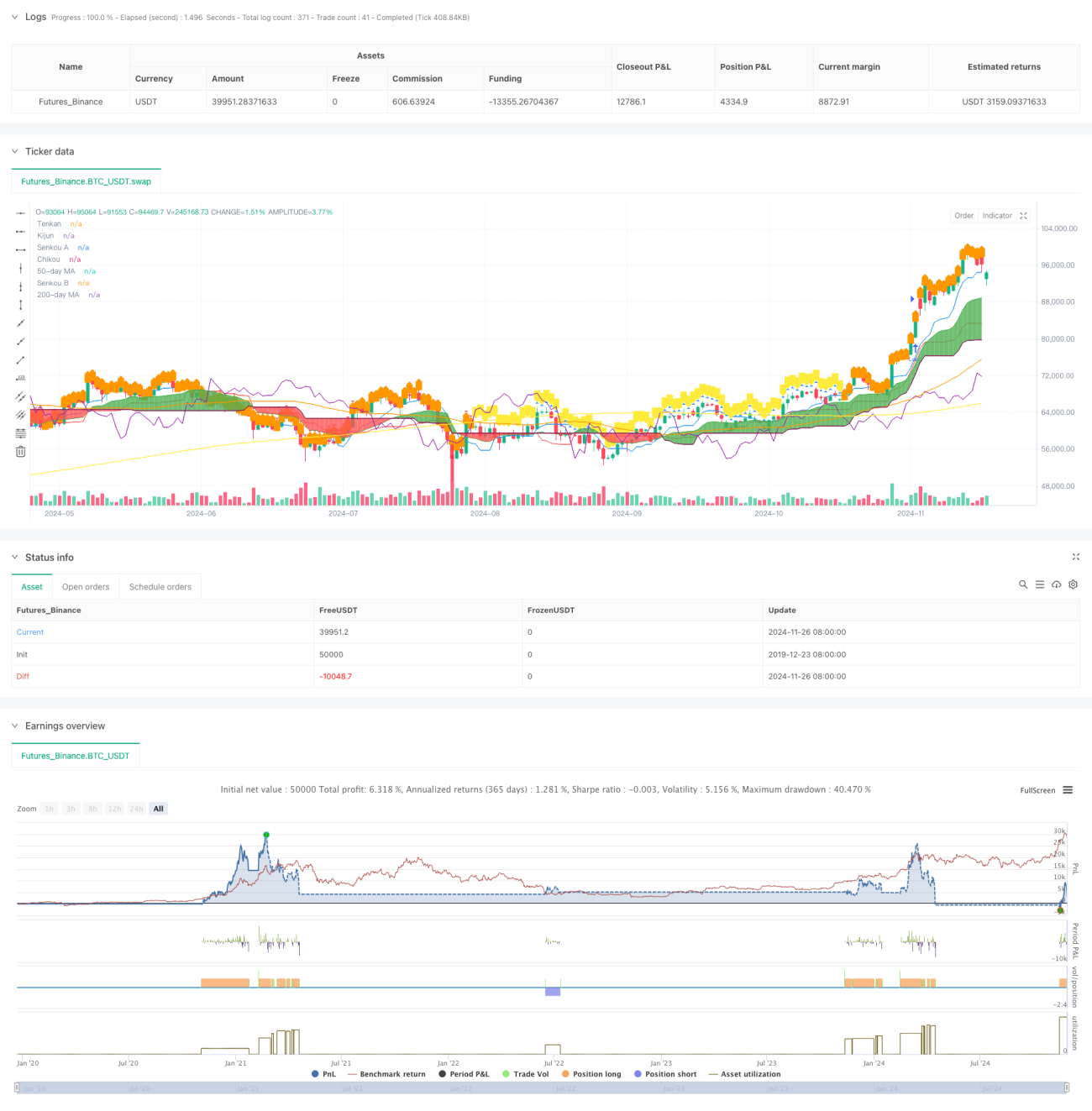

本戦略は、一連のテクニカル指標を組み合わせた完全な取引システムであり、主に一目均衡表(Ichimoku Cloud)を用いて取引判断を行います。システムは、転換線(Tenkan)と基準線(Kijun)のクロスでエントリータイミングを決定し、相対力指数(RSI)と移動平均線(MA)を補助フィルターとして併用します。また、雲(クモ)構成要素を動的ストップロスとして活用し、完全なリスク管理体制を構築しています。

戦略の原理

戦略のコアロジックは、以下の主要要素に基づきます。

- エントリーシグナルは転換線と基準線のクロスにより発生し、上抜けで買いシグナル、下抜けで売りシグナルとなります。

- 価格と雲(Kumo)の位置関係をトレンド確認に用い、価格が雲の上にあれば買い、下にあれば売りとします。

- 50日と200日の移動平均線の位置関係をトレンドフィルターとして使用します。

- 週足RSIを市場の強弱確認に用い、偽シグナルを除去します。

- 雲の上下限を動的ストップロス位置とし、リスクの動的管理を実現します。

戦略の優位性

- 複数のテクニカル指標を組み合わせることで、より信頼性の高い取引シグナルを提供し、偽シグナルの影響を大幅に低減します。

- 雲を動的ストップロスとすることで、市場の変動に応じてストップロス位置を自動調整し、利益を保護しつつ価格に十分な変動幅を与えます。

- 週足RSIによるフィルターにより、過度の買われすぎ・売られすぎゾーンでの不利な取引を効果的に回避します。

- 移動平均線のクロスが追加のトレンド確認を提供し、取引成功率を高めます。

- エントリー、保有、エグジットの各段階を含む完全なリスク管理体制を備えています。

戦略のリスク

- 複数の指標フィルターにより、潜在的な好機を逃す可能性があります。

- レンジ相場では、頻繁な偽ブレイクアウトシグナルが発生する可能性があります。

- 一目均衡表自体に遅延性があり、エントリータイミングに影響を与える可能性があります。

- 急変動相場では、動的ストップロスが緩すぎる場合があります。

- フィルター条件が多すぎると取引機会が減少し、戦略全体の収益に影響を与える可能性があります。

戦略の最適化方向性

- ボラティリティ指標を導入し、市場変動に応じて戦略パラメータを調整します。

- 一目均衡表のパラメータ設定を最適化し、異なる市場環境に適応させます。

- 出来高分析を追加し、シグナルの信頼性を高めます。

- 時間フィルター機構を導入し、変動の大きい時間帯を回避します。

- 適応型パラメータ最適化システムを開発し、戦略の動的調整を実現します。

まとめ

本戦略は、複数のテクニカル指標を組み合わせることで、完全な取引システムを構築しています。シグナルの生成に重点を置くだけでなく、完璧なリスク管理機構も備えています。多重フィルター条件の設定により、取引成功率を効果的に向上させています。また、動的ストップロスの設計により、良好なリスクリターン比を提供します。最適化の余地はあるものの、全体として構造が完全でロジックが明確な戦略システムです。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1