1

Follow

1802

Followers

概要

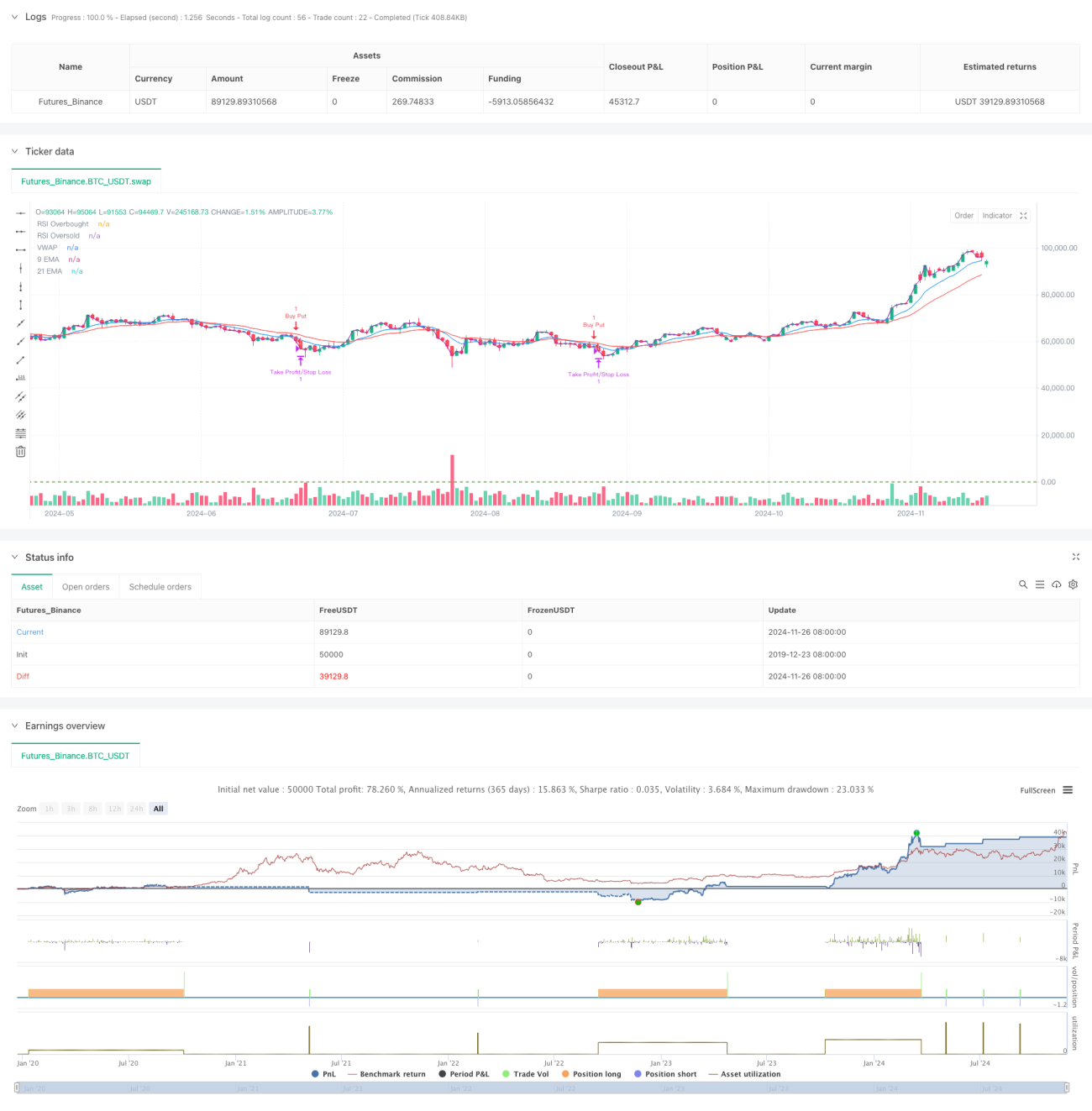

本戦略は、複数のテクニカル指標を組み合わせた高頻度取引システムであり、5分足の時間枠を採用し、移動平均線システム、モメンタム指標、出来高分析を統合しています。市場の変動に適応するために動的な調整を行い、複数のシグナル確認により取引の精度と信頼性を高めます。戦略の中核は、多面的なテクニカル指標の組み合わせにより短期的な市場トレンドを捉え、動的なストップロスでリスクを管理することです。

戦略の原理

本戦略は二重移動平均線システム(9期間と21期間のEMA)を主なトレンド判断ツールとして採用し、RSI指標でモメンタムを確認します。価格が二重移動平均線の上にあり、かつRSIが40~65の範囲にある場合、買いの機会を探ります。価格が二重移動平均線の下にあり、かつRSIが35~60の範囲にある場合、売りの機会を探ります。同時に、出来高確認メカニズムを導入し、現在の出来高が20期間の移動平均出来高の1.2倍以上であることを要求します。VWAPの使用により、取引の方向性が日内の主流トレンドと一致することをさらに保証します。

戦略のメリット

- 複数のシグナル確認メカニズムにより取引の信頼性が大幅に向上

- 動的な利食い・ストップロス設定により様々な市場環境に適応可能

- 保守的なRSI閾値を採用し、極端なエリアでの取引を回避

- 出来高確認メカニズムが偽シグナルを効果的にフィルタリング

- VWAPの使用により、取引方向が主流資金と一致することを保証

- 応答性の高い移動平均線システムが短期的な市場機会の捕捉に適している

戦略のリスク

- レンジ相場では頻繁な偽シグナルが発生する可能性がある

- 複数条件の制限により一部の取引機会を逃す恐れがある

- 高頻度取引では取引コストが高くなる可能性がある

- 市場が急激に方向転換した場合、反応が遅れる可能性がある

- リアルタイムの相場データに対する要求が高い

戦略の最適化方向

- 適応型パラメータ調整メカニズムを導入し、市場状態に応じて指標パラメータを動的に調整する

- 市場環境認識モジュールを追加し、異なる市場条件下で異なる取引戦略を採用する

- 出来高フィルタ条件を最適化し、相対出来高や出来高プロファイル分析を検討する

- ストップロスメカニズムを改善し、トレーリングストップ機能を追加する

- 取引時間フィルタを追加し、値動きの激しい寄り付きや引けの時間帯を避ける

まとめ

本戦略は、複数のテクニカル指標を組み合わせることで、比較的完全な取引システムを構築しています。戦略の強みは、多面的なシグナル確認メカニズムと動的なリスク管理手法にあります。いくつかの潜在的なリスクはあるものの、適切なパラメータ最適化とリスク管理により、戦略は実用的な価値を持っています。トレーダーは実運用前に十分なバックテストを行い、具体的な市場状況に応じて適切なパラメータ調整を行うことを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1