1

Follow

1802

Followers

概要

本戦略は、Elder's Force Index(EFI)に基づく定量取引システムであり、標準偏差と移動平均線を組み合わせてシグナルを判定し、ATRを用いてストップロスと利食いの位置を動的に調整します。高速と低速のEFI指標を計算し、それらを標準化した後にクロスシグナルを判定することで、完全な取引システムを構築しています。動的ストップロスとトレーリング利食いの仕組みを採用し、リスクを効果的に管理しながらより大きな利益を追求します。

戦略原理

戦略は主に以下のコア要素に基づいて構築されています:

- 2つの異なる期間(13と50)のEFI指標を使用して、高速と低速のフォースインデックスを計算

- 両期間のEFIを標準偏差で正規化し、シグナルに統計的な意味を持たせる

- 高速と低速のEFIが同時に上方の標準偏差を突破した場合、買いシグナルを発動

- 高速と低速のEFIが同時に下方の標準偏差を突破した場合、売りシグナルを発動

- ATRを使用してストップロスの位置を動的に設定し、価格変動に応じて調整

- ATRに基づくトレーリング利食い機構を採用し、利益を保護しながら成長を促す

戦略の優位性

- シグナルシステムはモメンタムとボラティリティ特性を組み合わせ、取引の信頼性を向上

- 標準偏差による正規化処理により、統計的に意味のあるシグナルを生成し、偽シグナルを低減

- 動的ストップロス機構はリスクを効果的に管理し、大きなドローダウンを回避

- トレーリング利食い機構は既存の利益を保護しつつ、さらなる成長を許容

- 戦略ロジックは明確でパラメータ調整の柔軟性が高く、さまざまな市場に最適化可能

戦略のリスク

- 激しい変動市場では偽シグナルが発生する可能性があり、追加のフィルター機構が必要

- パラメータ選択が過度に敏感だと過剰取引につながり、取引コストが増加

- トレンド転換点でラグが発生し、戦略パフォーマンスに影響を与える可能性

- ストップロスの設定が不適切だと早期エグジットや過大な損失を招く恐れ

- 取引コストが戦略収益に与える影響を考慮する必要がある

戦略の最適化方向性

- 市場環境の判断機構を追加し、異なる市場状況で異なるパラメータ設定を使用

- 出来高フィルターを導入し、シグナルの信頼性を向上

- ストップロス・利食いパラメータを最適化し、市場変動への適応性を高める

- トレンドフィルターを追加し、レンジ相場での頻繁な取引を回避

- 時間フィルターを組み込み、不利な時間帯の取引を避ける

まとめ

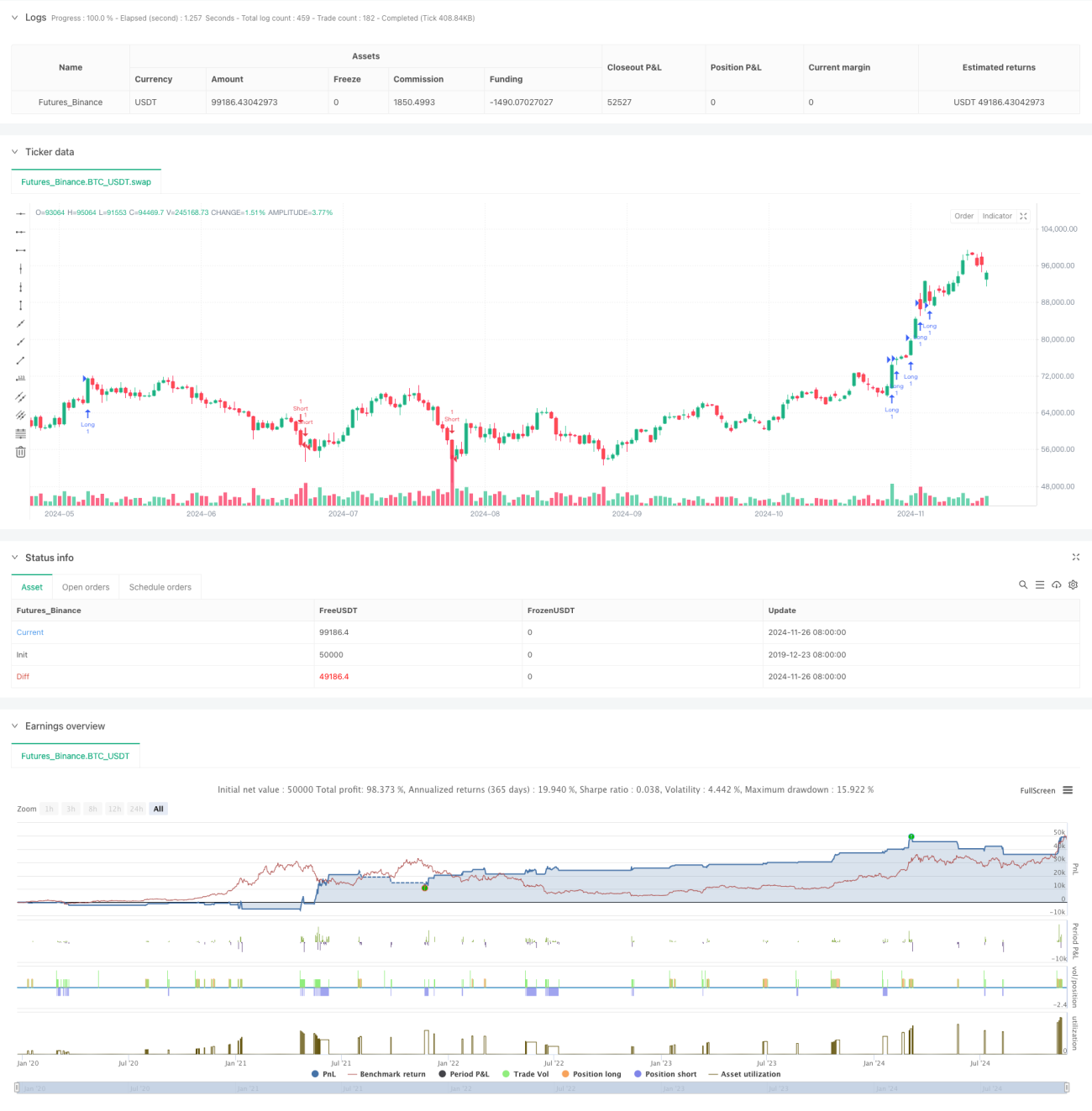

本戦略は、EFI指標、標準偏差、ATRを組み合わせることで、完全な取引システムを構築しています。シグナルシステムの信頼性が高く、リスク管理が合理的である一方、市場環境に応じた最適化が必要です。市場環境の判断や出来高フィルターなどのメカニズムを追加することで、戦略の安定性と収益性をさらに向上させることができます。全体として、本戦略は実用的な定量取引フレームワークを提供し、優れた実用価値を備えています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1