1

Follow

1802

Followers

概要

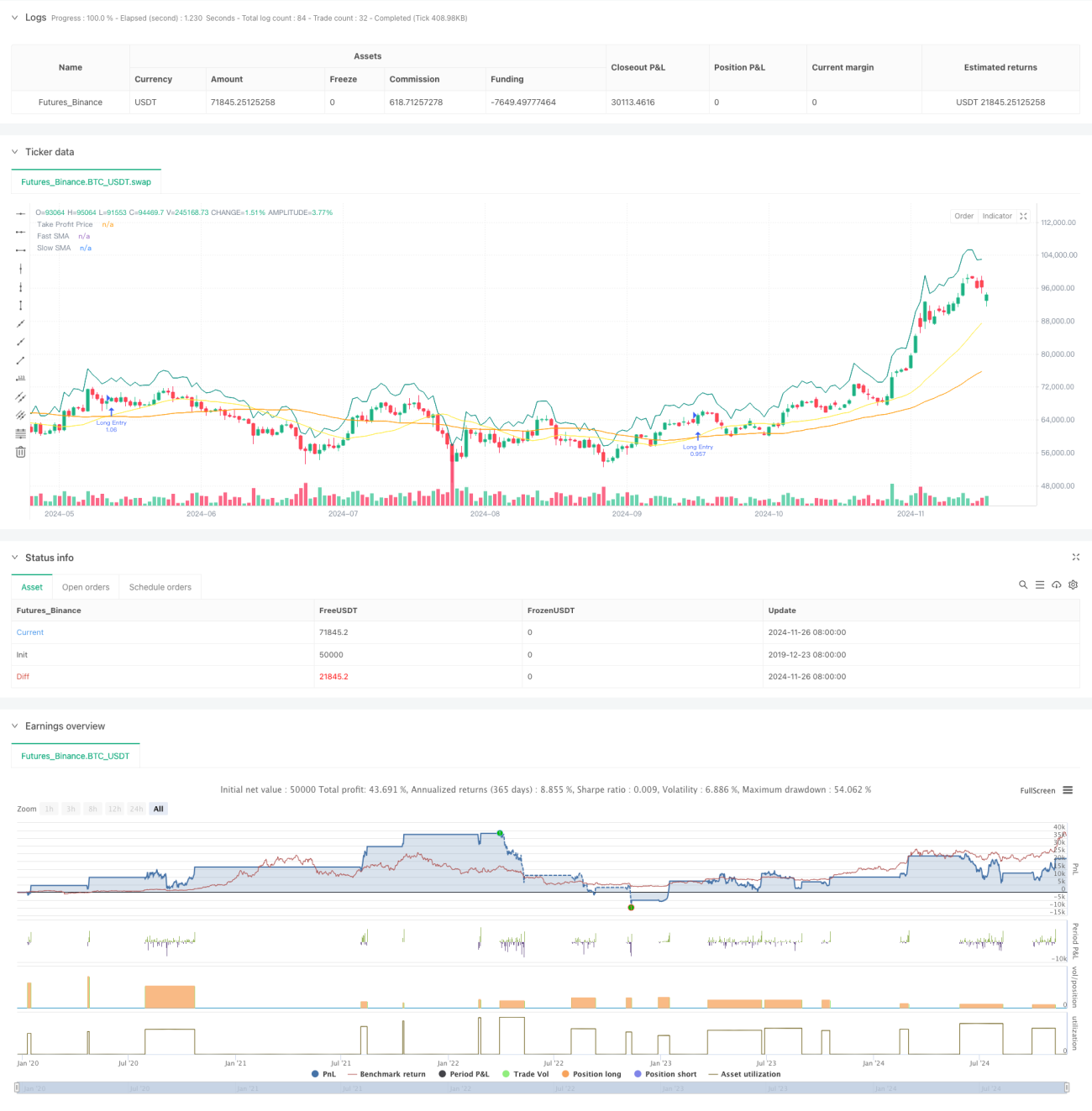

本戦略は、古典的なダブル移動平均線トレンドフォローとATR動的リスク管理を組み合わせた適応型取引システムです。戦略は2つの取引モードを提供します。基本モードでは単純なダブル移動平均線クロスによるトレンドフォローを行い、上位モードではより高い時間枠でのトレンドフィルターとATRベースの動的ストップロス機構を追加します。シンプルなドロップダウンメニューで2つのモードを切り替えられるため、初心者の使いやすさと、経験豊富なトレーダーのリスク管理ニーズを両立しています。

戦略の原理

戦略1(基本モード)は21日と49日のダブル移動平均線システムを採用し、短期移動平均線が長期移動平均線を上抜けた場合に買いシグナルを生成します。利益目標はパーセンテージまたはポイント単位で設定可能で、オプションのトレーリングストップ機能により利益を確保できます。戦略2(上位モード)はダブル移動平均線システムに日足レベルのトレンドフィルターを追加し、価格がより高い時間枠の移動平均線より上にある場合のみエントリーを許可します。さらに、14期間のATRに基づく動的ストップロスを導入し、ストップロス幅が市場のボラティリティに応じて自動調整され、部分利益確定機能により既得利益を保護します。

戦略の優位性

- トレーダーの経験レベルや市場環境に応じて柔軟に切り替え可能な高い適応性

- 上位モードの複数時間枠分析によりシグナル品質が向上

- ATR動的ストップロスが様々な市場変動条件に対応

- 部分利益確定メカニズムが利益保護とトレンド継続のバランスを実現

- パラメータ設定が柔軟で、異なる市場特性に応じた最適化が容易

戦略のリスク

- ダブル移動平均線システムはレンジ相場で頻繁な偽シグナルを発生させる可能性あり

- トレンドフィルターによりシグナルが遅れ、一部の取引機会を逃す可能性

- ATRストップロスはボラティリティの急変時に間に合わない可能性

- 部分利益確定により早期にポジションを縮小し、大きなトレンド利益を逃す可能性

戦略の最適化方向性

- 出来高やボラティリティ指標を追加し、偽シグナルをフィルタリング

- 動的パラメータ適応メカニズムを導入し、市場状態に応じて移動平均線期間を自動調整

- ATR計算期間を最適化し、感度と安定性のバランスを図る

- 市場状態認識モジュールを追加し、最適な戦略モードを自動選択

- トレーリングストップや時間ストップなど、追加のストップロス方式を選択可能に

まとめ

本戦略は設計が合理的で機能が充実した取引戦略システムです。ダブル移動平均線トレンドフォローとATRリスク管理の組み合わせにより、信頼性の高い戦略と優れたリスク管理を両立しています。デュアルモード設計は様々なレベルのトレーダーのニーズに対応し、豊富なパラメータ設定により十分な最適化の余地を提供します。トレーダーは実践において保守的なパラメータから始め、徐々に調整・最適化して最良の結果を得ることを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1