複数移動平均線トレンド追跡とRSIモメンタム戦略

1

Follow

1797

Followers

概要

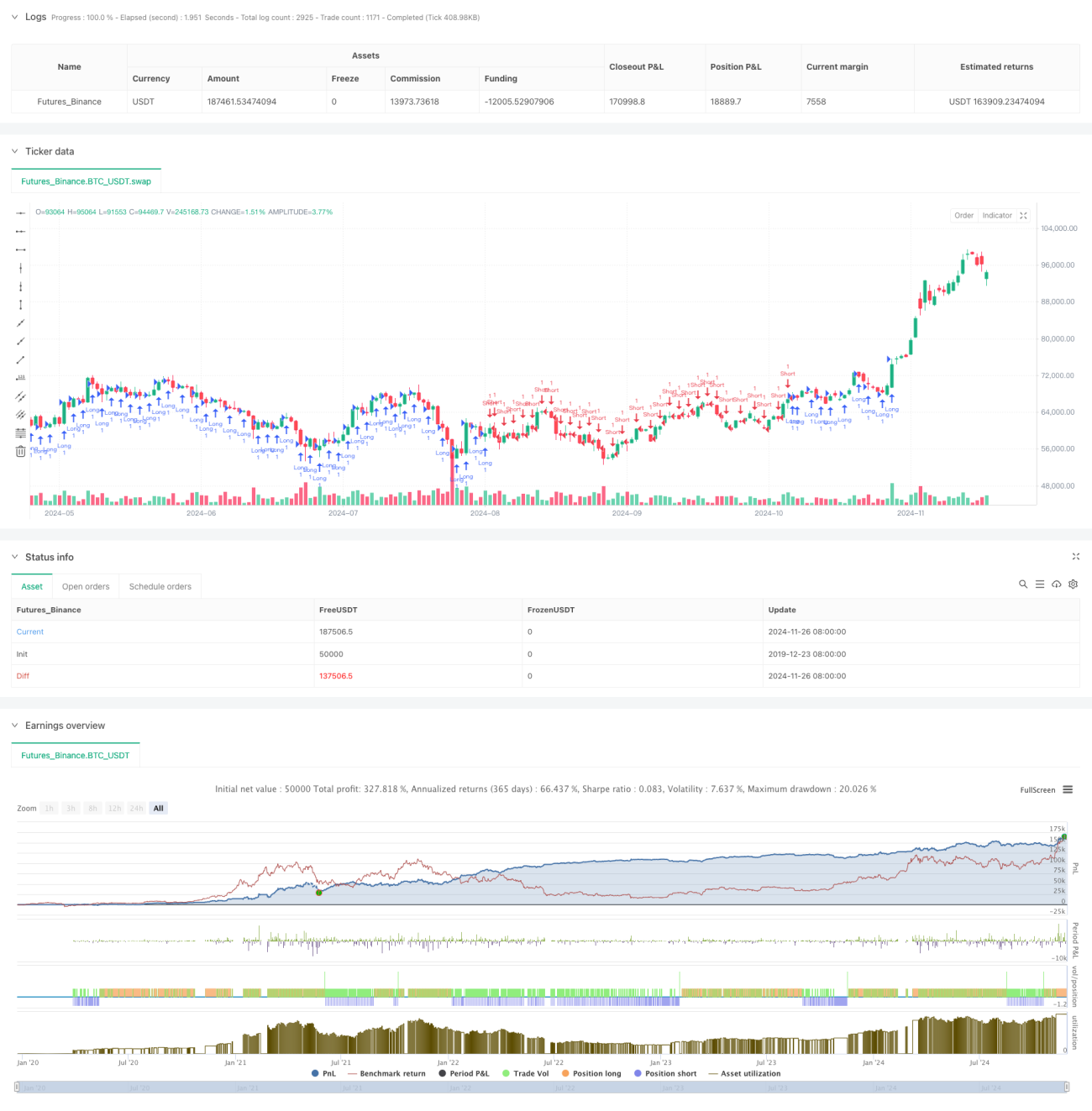

本戦略は、複数の移動平均線システムとRSIインジケーターを組み合わせたトレンドフォロー戦略です。戦略では20、50、200期間の移動平均線を組み合わせ、異なる移動平均線間の位置関係を分析して市場のトレンドを判断し、RSIインジケーターによる取引シグナルの確認を行います。動的なストップロスと利益目標を設定し、トレーリングストップにより獲得した利益を保護します。

戦略の原理

戦略の核心は、3本の移動平均線(MA20、MA50、MA200)の相対的な位置関係を分析して市場トレンドを判断することです。戦略は18種類の異なる移動平均線シナリオを定義し、主に移動平均線のクロスと位置関係に注目します。短期移動平均線が長期移動平均線より上にある場合は買い傾向、逆の場合は売り傾向とします。過剰な取引を避けるため、戦略ではRSIインジケーターをフィルター条件として導入し、RSIが70未満の場合に買いを許可し、30を超える場合に売りを許可します。戦略はリスク対リターン比1:10を設定し、25ポイントのトレーリングストップで利益を保護します。

戦略のメリット

- 多次元のトレンド確認:複数の移動平均線の関係を分析することで、市場トレンドの強さと方向性をより正確に判断できます。

- 動的なリスク管理:トレーリングストップ機構を採用し、獲得した利益を保護しながら利益の継続的な成長を可能にします。

- フィルター機構の完成度:RSIインジケーターによるシグナルフィルターにより、偽のシグナルを効果的に削減します。

- リスク対リターン比の最適化:リスク対リターン比1:10を採用し、大きなトレンドによる利益を追求します。

- 適応性の高さ:さまざまな市場や時間足に適用可能です。

戦略のリスク

- レンジ相場のリスク:横ばいのレンジ相場では、頻繁な偽のブレイクアウトシグナルが発生する可能性があります。

- スリッページリスク:急激な相場では、25ポイントのトレーリングストップがスリッページにより正確に執行されない可能性があります。

- トレンド反転リスク:トレンドが反転した場合、戦略の反応が遅れ、獲得した利益が目減りする可能性があります。

- パラメータ依存性:戦略の効果は、移動平均線の期間とRSIパラメータの選択に大きく依存します。

戦略の最適化方向

- 出来高インジケーターの導入:出来高分析を追加することで、トレンド判断の精度を向上させることができます。

- シナリオ定義の最適化:重複するシナリオ定義を簡略化し、戦略の実行効率を向上させることができます。

- 動的なパラメータ調整:市場のボラティリティに応じてトレーリングストップのポイントを動的に調整することができます。

- 時間フィルターの追加:取引時間帯のフィルターを追加し、ボラティリティの大きい市場の寄付きと引けの時間帯を回避します。

- シグナル確認の最適化:トレンド強度確認インジケーターを追加し、取引シグナルの信頼性を高めることができます。

まとめ

本戦略は、構造が整っており論理が明確なトレンドフォロー戦略です。複数の移動平均線システムを組み合わせ、RSIインジケーターによるフィルターを加えることで、比較的信頼性の高い取引システムを構築しています。戦略のリスク管理機構は合理的に設計されており、トレーリングストップにより利益を保護しつつ早期に離脱することを防ぎます。戦略にはまだ最適化の余地がありますが、全体のフレームワークは科学的に設計されており、実用的な価値があります。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1