動的リスク管理と固定利得に基づく高度な公正価値ギャップ検出戦略

1

Follow

1802

Followers

概要

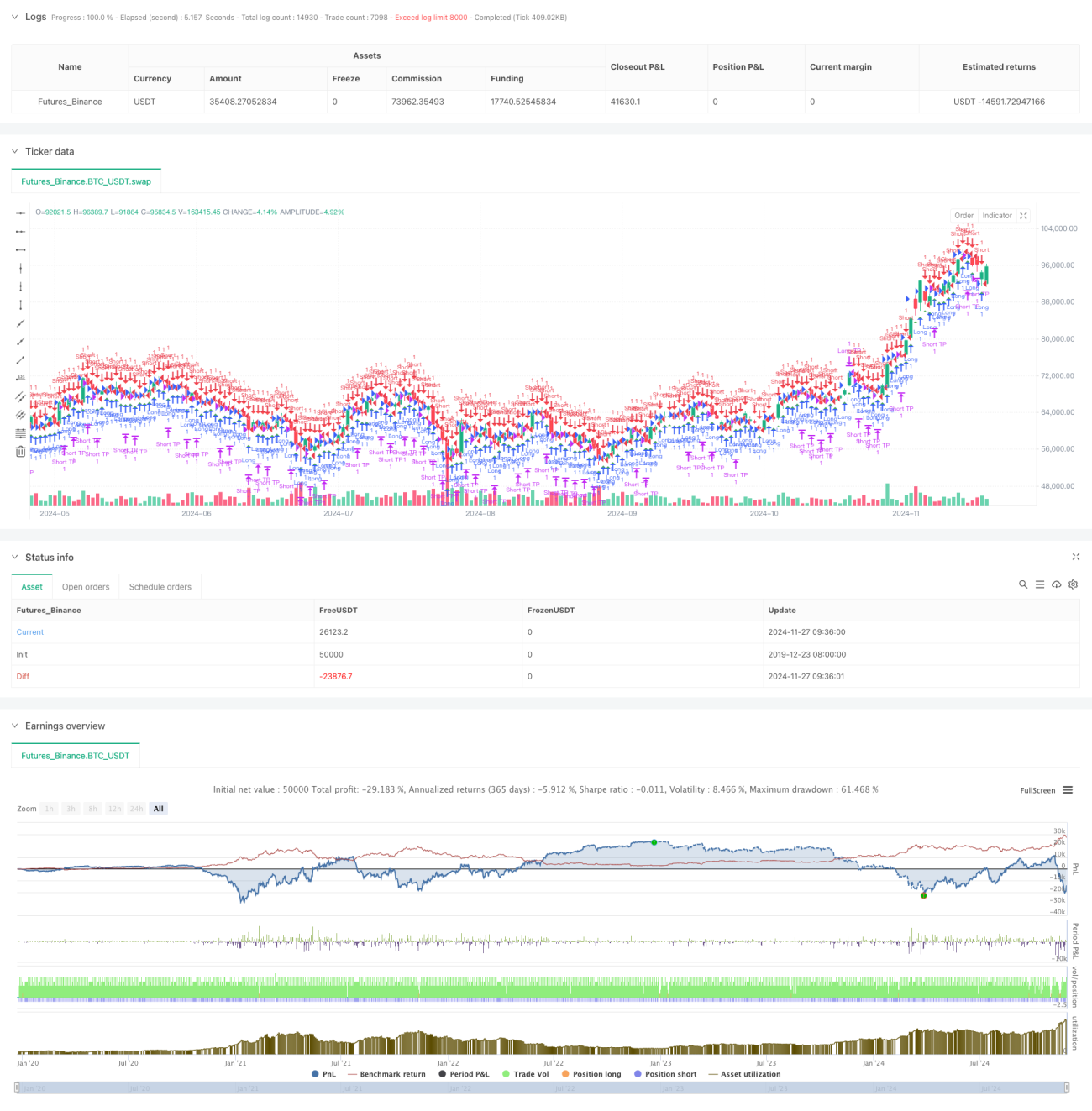

これは、フェアバリューギャップ(FVG)に基づく取引戦略であり、ダイナミックなリスク管理と固定利益目標を組み合わせたものです。この戦略は15分足で動作し、市場の価格ギャップを識別することで潜在的な取引機会を捉えます。バックテストデータによると、2023年11月から2024年8月の期間に、この戦略は284.40%の純利益率を達成し、合計153回の取引を完了し、勝率は71.24%、プロフィットファクターは2.422でした。

戦略の原理

戦略の核心は、連続する3本のローソク足間の価格関係を監視してフェアバリューギャップを識別することです。具体的には以下の通りです。

- ロングFVG形成条件:前のローソク足の高値が、その前の2本のローソク足の最安値よりも低い場合。

- ショートFVG形成条件:前のローソク足の最安値が、その前の2本のローソク足の高値よりも高い場合。

- エントリーシグナルはFVGしきい値パラメータによって制御され、ギャップの大きさが価格の一定割合を超えた場合にのみトリガーされます。

- リスク管理は、アカウント資産の固定割合(1%)をストップロスの基準として使用します。

- 利益目標は固定ポイント数(50ポイント)で設定されます。

戦略の利点

- リスク管理が科学的かつ合理的:アカウント資産割合のストップロスにより、動的なリスク管理が可能。

- 取引ルールが明確:固定の利益目標を使用するため、主観的な判断を回避。

- パフォーマンスが優れている:高い勝率とプロフィットファクターは、戦略の良好な安定性を示す。

- 実装が簡単:コードの論理が明確で、理解とメンテナンスが容易。

- 適応性が高い:パラメータ調整により、さまざまな市場環境に適応可能。

戦略のリスク

- 市場変動リスク:変動の激しい市場では、固定ポイントの利益目標が柔軟性を欠く可能性がある。

- スリッページリスク:頻繁な取引は、高いスリッページコストにつながる可能性がある。

- パラメータ依存性:戦略のパフォーマンスは、FVGしきい値の設定に強く依存する。

- 偽ブレイクアウトリスク:一部のFVGシグナルは偽ブレイクアウトである可能性があり、追加の確認指標が必要。

- 資金管理リスク:連続損失時には、固定割合のストップロスにより資金が急速に減少する可能性がある。

戦略の最適化方向性

- 市場変動性指標を導入し、利益目標を動的に調整する。

- トレンドフィルターを追加し、レンジ相場での取引を回避する。

- 複数時間足の確認メカニズムを開発する。

- ポジション管理アルゴリズムを最適化し、変動ポジションシステムを導入する。

- 取引時間フィルターを追加し、変動の激しい時間帯を避ける。

- シグナル強度評価システムを開発し、高品質な取引機会を選別する。

まとめ

この戦略は、フェアバリューギャップ理論と科学的なリスク管理手法を組み合わせることで、良好な取引結果を示しています。高い勝率と安定したプロフィットファクターは、実戦での価値を示しています。提案された最適化の方向性により、戦略にはさらなる改善の余地があります。トレーダーは、リアルマネー取引に使用する前に、十分なパラメータ最適化とバックテスト検証を行うことを推奨します。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// ParametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1