多段階ボラティリティ適応型動的スーパートレンド戦略

概要

多段ボラティリティ適応型ダイナミック・スーパートレンド戦略は、ベガス・チャネルとスーパートレンド指標を組み合わせた革新的なトレーディングシステムです。この戦略の特長は、市場のボラティリティに動的に適応する能力と、多段利益確定メカニズムを採用してリスク・リターン比を最適化する点にあります。ベガス・チャネルのボラティリティ分析とスーパートレンドのトレンド追跡機能を組み合わせることで、市場環境の変化に応じて自動的にパラメータを調整し、より精度の高い取引シグナルを提供します。

戦略の原理

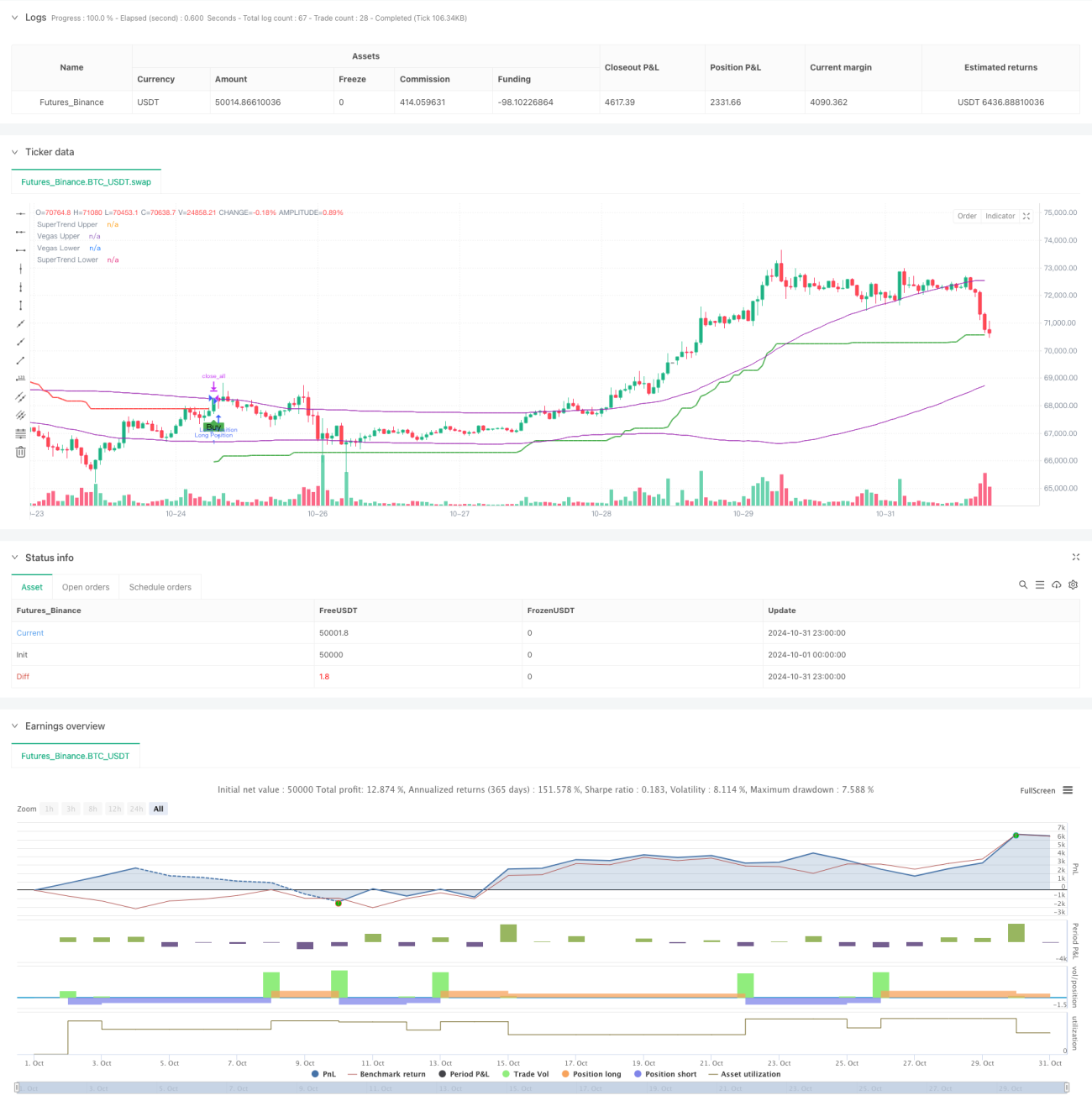

戦略は、ベガス・チャネル計算、トレンド検出、多段利益確定メカニズムの3つのコアコンポーネントに基づいて動作します。ベガス・チャネルは単純移動平均線(SMA)と標準偏差(STD)を用いて価格変動レンジを定義し、スーパートレンド指標は調整後のATR値に基づいてトレンド方向を決定します。市場トレンドが変化した際にシステムは取引シグナルを生成します。多段利益確定メカニズムにより、異なる価格帯で段階的にポジションを決済することが可能で、この方法は利益を確定しつつ、一部のポジションでさらなる潜在収益を得ることを可能にします。本戦略の独自性はボラティリティ調整係数にあり、この係数はベガス・チャネルの幅に基づいてスーパートレンドの乗数を動的に調整します。

戦略の利点

- 動的適応性:ボラティリティ調整係数により、異なる市場環境に自動的に適応できます。

- リスク管理:多段利益確定メカニズムは体系的な利益確定スキームを提供します。

- カスタマイズ性:複数のパラメータ設定オプションを提供し、さまざまな取引スタイルに対応します。

- 包括的な市場カバレッジ:ロング・ショート双方向取引をサポートします。

- 視覚的フィードバック:明確なグラフィカルインターフェースを提供し、分析と意思決定を容易にします。

戦略のリスク

- パラメータ感応性:パラメータの組み合わせによって戦略のパフォーマンスが大きく異なる可能性があります。

- ラグ:移動平均に基づく指標には一定のラグが存在します。

- 偽ブレイクアウトのリスク:レンジ相場では誤ったシグナルが発生する可能性があります。

- 利益確定設定のトレードオフ:早期の利益確定は大きなトレンドを逃す恐れがあり、遅すぎると既得利益を失う可能性があります。

戦略の最適化方向

- 市場環境フィルターを導入し、異なる市場条件下で戦略パラメータを調整する。

- 出来高分析を追加し、シグナルの信頼性を高める。

- 適応型利益確定メカニズムを開発し、市場のボラティリティに応じて利益確定水準を動的に調整する。

- 他のテクニカル指標を統合し、シグナルの確認を行う。

- 動的ポジション管理を実装し、市場リスクに応じて取引サイズを調整する。

まとめ

多段ボラティリティ適応型ダイナミック・スーパートレンド戦略は、複数のテクニカル指標と革新的な利益確定メカニズムを組み合わせることで、トレーダーに包括的な取引システムを提供する高度な定量取引手法です。その動的適応性とリスク管理機能は、特に異なる市場環境での運用に適しており、拡張性と最適化の余地も良好です。継続的な改善と最適化により、本戦略は将来的に安定した取引パフォーマンスを提供することが期待されます。

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Multi-Step Vegas SuperTrend - strategy [presentTrading]", shorttitle="Multi-Step Vegas SuperTrend - strategy [presentTrading]", overlay=true, precision=3, commission_value=0.1, commission_type=strategy.commission.percent, slippage=1, currency=currency.USD)

// Input settings allow the user to customize the strategy's parameters.- 1