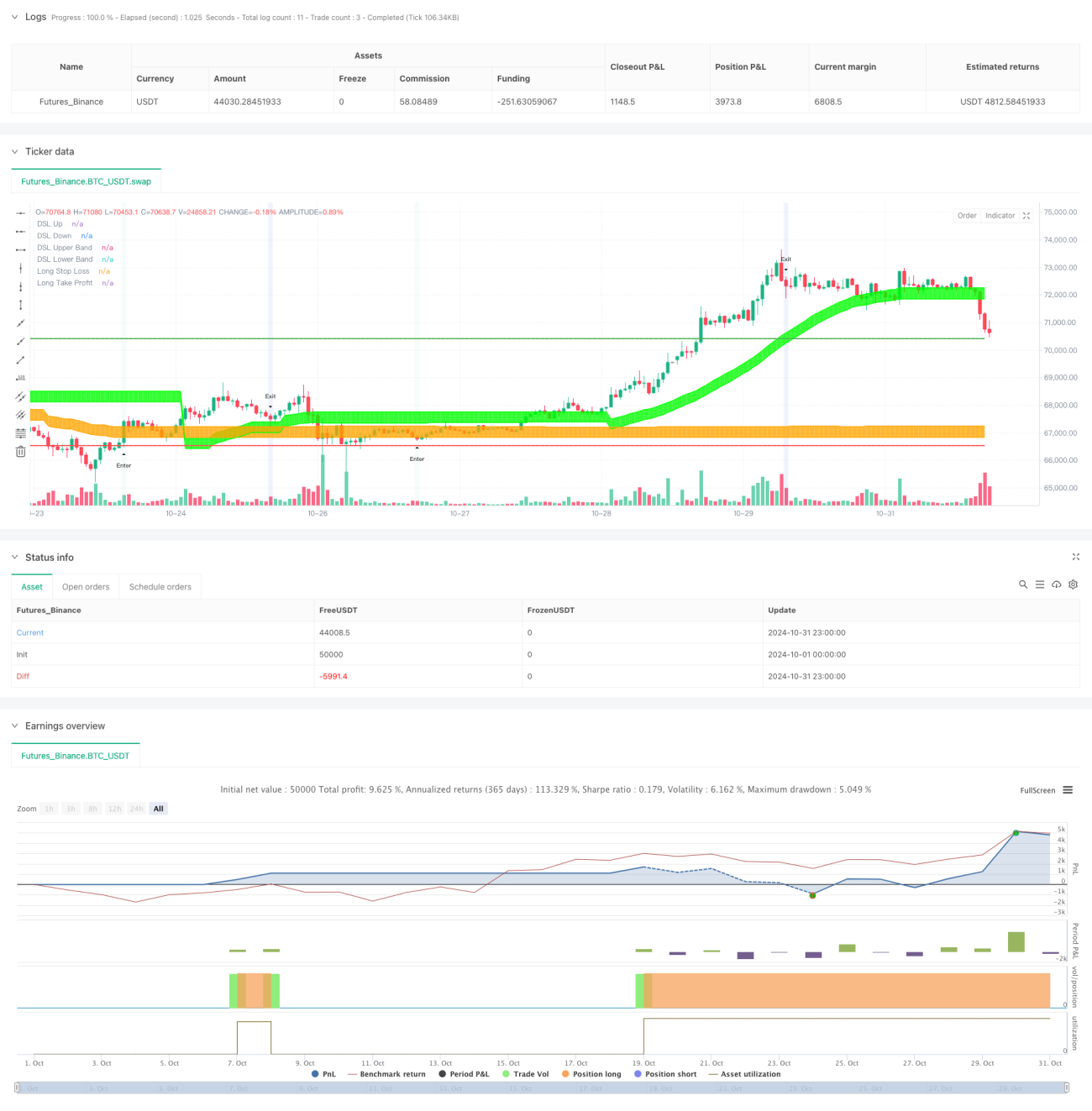

概要

本戦略は、ダイナミックシグナルライン(DSL)、ボラティリティ、モメンタム指標を組み合わせた統合取引システムです。動的閾値と適応型ボラティリティバンドにより、市場トレンドを効果的に識別し、モメンタム指標でシグナルをフィルタリングすることで、正確な取引タイミングを捉えます。システムには、動的ストップロスやリスクリワード比に基づく利益目標設定など、完全なリスク管理メカニズムが組み込まれています。

戦略の原理

戦略の中核ロジックは、以下の3つの主要コンポーネントで構成されています。

まず、ダイナミックシグナルラインシステムです。移動平均線に基づいた動的な上下軌道線を計算します。これらの軌道線は、市場の最近の高値と安値に応じて自動的に位置を調整し、トレンドに適応して追跡します。また、ATR指標を用いた動的ボラティリティバンドを構築し、トレンドの強さを確認するとともに、ストップロスの位置を設定します。

次に、モメンタム分析システムです。ゼロラグ指数移動平均(ZLEMA)で最適化されたRSI指標を使用します。RSIにダイナミックシグナルラインの概念を適用することで、買われすぎ・売られすぎ領域をより正確に識別し、モメンタムブレイクアウトシグナルを生成します。

3つ目は、シグナル統合メカニズムです。取引シグナルは、トレンド確認とモメンタムブレイクアウトの両方の条件が満たされた場合にのみトリガーされます。ロングエントリーには、価格が上軌道を突破し、その上に維持されること、さらにRSIが下方のダイナミックシグナルラインを突破することが必要です。ショートシグナルには、その逆の条件が同時に満たされる必要があります。

戦略の優位性

- 高い適応性:ダイナミックシグナルラインとボラティリティバンドが市場状況に応じて自動調整されるため、さまざまな市場環境に適応できます。

- 誤シグナルのフィルタリング:トレンドとモメンタムの二重確認を要求することで、誤シグナルの確率を大幅に低減します。

- 完全なリスク管理:ATRベースの動的ストップロスとリスクリワード比に基づく利益目標設定を統合し、体系的なリスクコントロールを実現します。

- 柔軟なカスタマイズ:戦略パラメータは、異なる市場や時間枠に合わせて最適化・調整可能です。

戦略のリスク

- トレンド反転リスク:急激な市場反転時には、ダイナミックシグナルラインの調整が間に合わず、大きなドローダウンが発生する可能性があります。

- レンジ相場でのリスク:レンジ相場では、頻繁なブレイクアウトにより複数回のストップロスが発生する可能性があります。

- パラメータ感度:戦略のパフォーマンスはパラメータ設定に敏感であり、不適切なパラメータは戦略の効果に悪影響を及ぼす可能性があります。

戦略の最適化方向性

- 市場環境の識別:市場環境分類メカニズムを追加し、異なる市場状態で異なるパラメータ設定を使用します。

- 動的パラメータ最適化:適応型パラメータ調整メカニズムを導入し、市場のボラティリティに応じてシグナルラインとボラティリティバンドのパラメータを自動最適化します。

- マルチタイムフレーム分析:複数の時間枠のシグナルを統合し、取引判断の信頼性を高めます。

- ボラティリティ適応:高ボラティリティ期間中はストップロス幅とリスクリワード比を調整し、リスク調整後リターンを向上させます。

まとめ

本戦略は、ダイナミックシグナルラインとモメンタム指標の革新的な組み合わせにより、市場トレンドを効果的に捉えます。完全なリスク管理メカニズムとシグナルフィルタリングシステムにより、実戦での応用価値が高いです。継続的な最適化とパラメータ調整により、さまざまな市場環境で安定したパフォーマンスを維持することが期待されます。一定のリスクは存在しますが、適切なパラメータ設定とリスク管理対策により、これらのリスクはコントロール可能です。

- 1