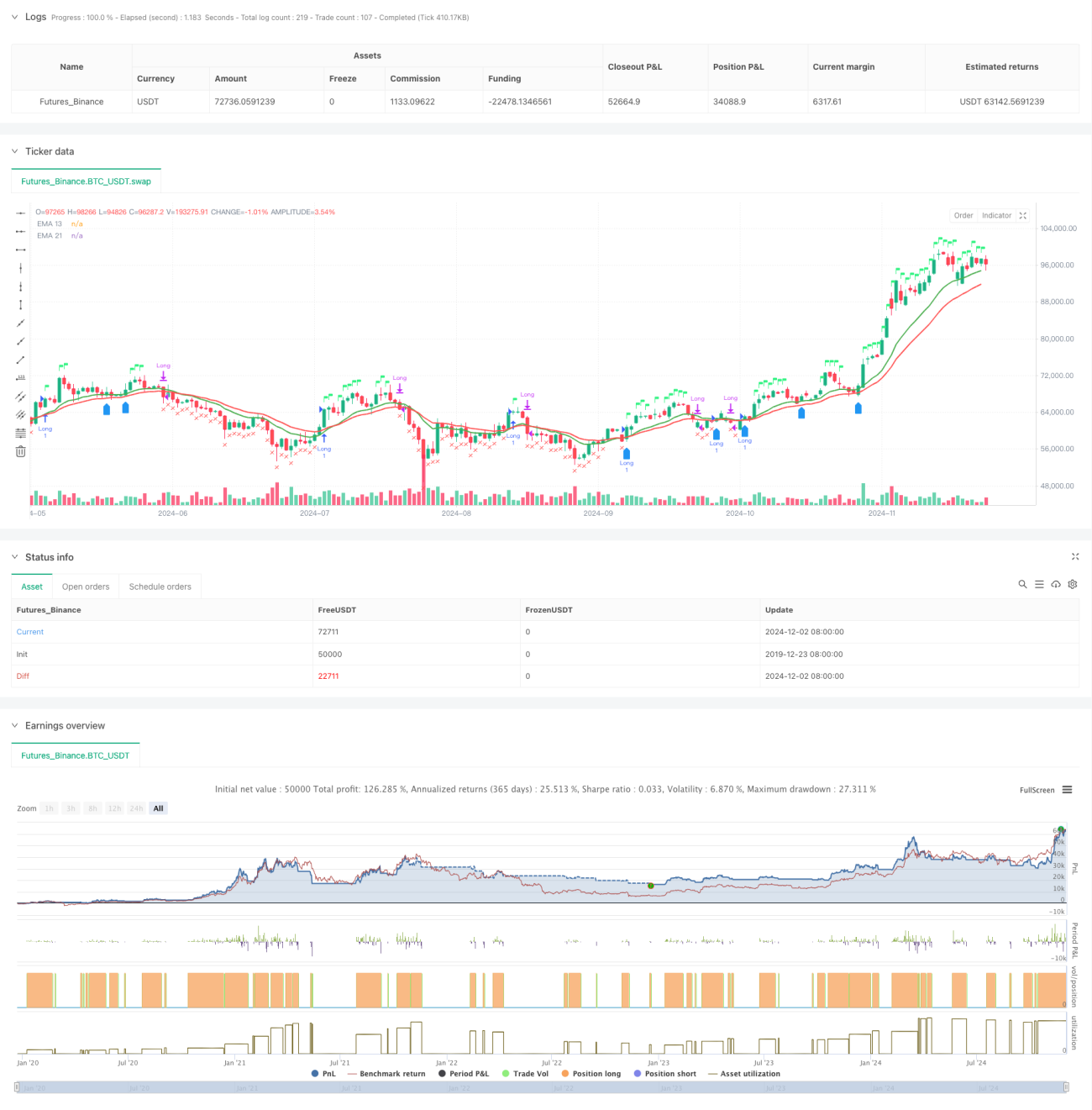

ダブル移動平均線とRSIのハイブリッド適応型戦略

1

Follow

1802

Followers

概要

本戦略は、2本の移動平均線システム、相対力指数(RSI)、および相対強度(RS)分析を組み合わせた総合取引システムです。13日と21日の指数平滑移動平均線(EMA)のクロスでトレンドを確認し、同時にRSIとベンチマーク指数に対するRS値を用いて取引シグナルを確認することで、多次元的な取引判断メカニズムを実現しています。また、52週高値に基づくリスク管理メカニズムと再エントリー条件の判断も含まれています。

戦略の原理

戦略は複数のシグナル確認メカニズムを採用:

- エントリーシグナルは以下の条件をすべて満たす必要がある:

- EMA13がEMA21を上抜ける、または価格がEMA13より上にある

- RSIが60より大きい

- 相対強度(RS)が正の値

- エグジット条件:

- 価格がEMA21を下回る

- RSIが50未満

- RSが負の値に転じる

- 再エントリー条件:

- 価格がEMA13を上抜け、かつEMA13がEMA21より大きい

- RSが正の値を維持

- または価格が先週の高値を突破

戦略の利点

- 複数のシグナル確認メカニズムにより、偽の突破リスクを低減

- 相対強度分析を組み合わせ、強力な銘柄を効果的に選別

- 適応的な期間調整メカニズムを採用

- 完全なリスク管理体制を備える

- インテリジェントな再エントリーメカニズムを含む

- リアルタイムの取引状態可視化を提供

戦略のリスク

- レンジ相場では頻繁な取引が発生する可能性がある

- 複数の指標に依存するため、シグナルが遅れる可能性がある

- 固定されたRSI閾値がすべての市場環境に適応するとは限らない

- 相対強度の計算はベンチマーク指数の正確性に依存する

- 52週高値によるストップロス水準が緩すぎる可能性がある

戦略の最適化方向

- 適応型RSI閾値の導入

- 再エントリー条件の判断ロジックの最適化

- 出来高分析の次元追加

- 利確・損切りメカニズムの改善

- ボラティリティフィルターの追加

- 相対強度計算期間の最適化

まとめ

本戦略は、テクニカル分析と相対強度分析を組み合わせることで、総合的な取引システムを構築しています。複数のシグナル確認メカニズムとリスク管理体制により、実用性が高くなっています。提案された最適化方向により、戦略はさらに改善の余地があります。戦略の成功には、トレーダーが市場を深く理解し、取引する銘柄の特性に応じて適切なパラメータ調整を行うことが必要です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1