1

Follow

1802

Followers

概要

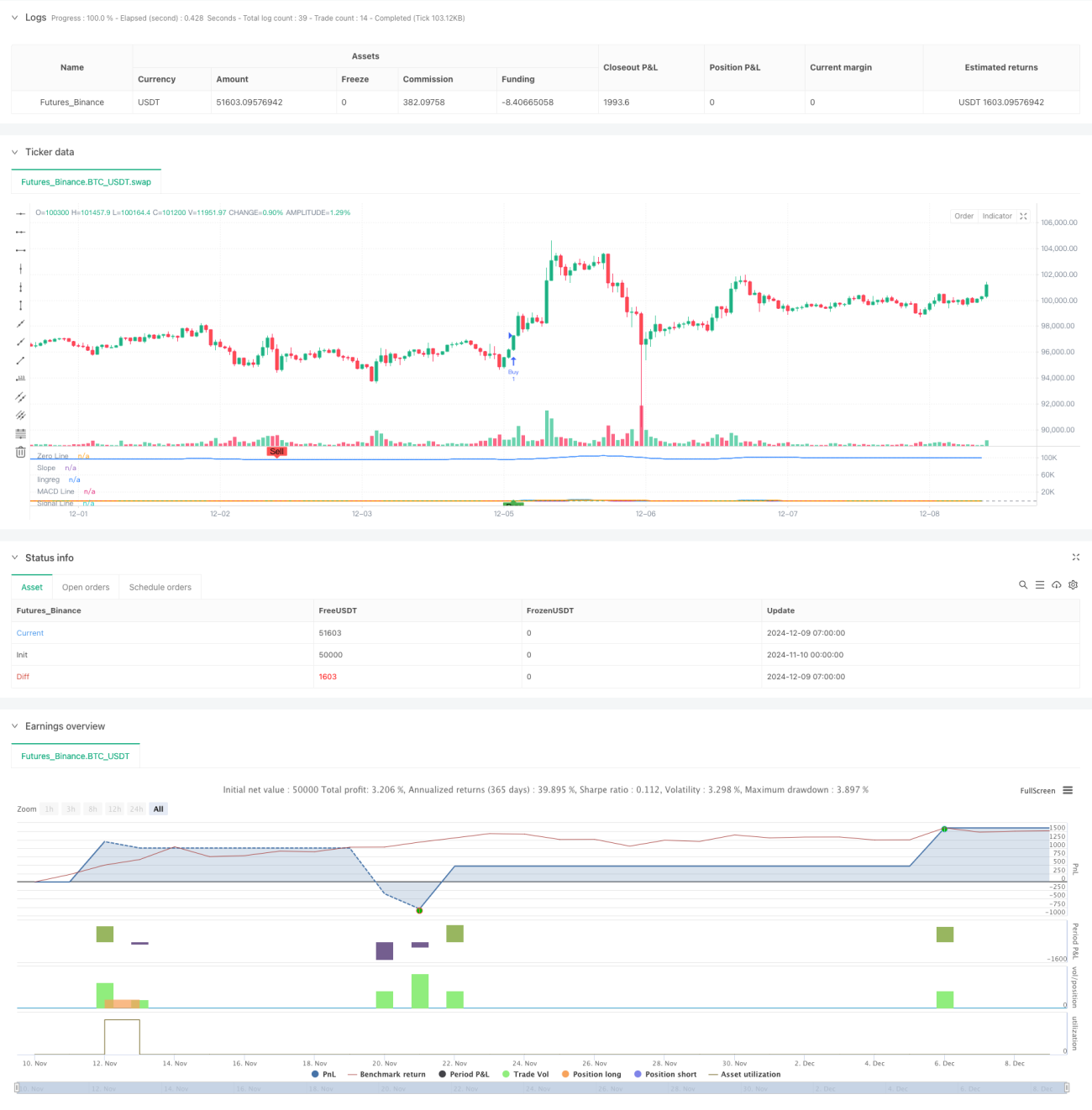

本戦略は、MACD(移動平均収束拡散指標)と線形回帰傾き(LRS)を組み合わせたスマートトレーディングシステムです。戦略では、複数の移動平均法の組み合わせによりMACD指標の計算を最適化し、線形回帰分析を導入して取引シグナルの信頼性を高めています。トレーダーは単一指標または二指標の組み合わせを柔軟に選択して取引シグナルを生成でき、損切り・利確メカニズムを備えてリスクを管理します。

戦略の原理

戦略の中核は、最適化されたMACDと線形回帰指標により市場トレンドを捉えることです。MACD部分では、SMA、EMA、WMA、TEMAの4種類の移動平均法を組み合わせて計算し、価格トレンドへの感応度を強化しています。線形回帰部分では、回帰直線の傾きと位置を計算してトレンドの方向と強さを判断します。買いシグナルはMACDのゴールデンクロス、線形回帰の上昇トレンド、または両方の組み合わせ確認に基づきます。同様に売りシグナルも柔軟に設定可能です。戦略にはパーセンテージベースの利確・損切り設定も含まれており、各取引のリスクリワード比を効果的に管理します。

戦略の優位性

- 指標組み合わせの柔軟性:市場状況に応じて単一指標または二指標の組み合わせを選択可能

- 改良されたMACD計算:複数の移動平均法によりトレンド認識の精度が向上

- 客観的なトレンド確認:線形回帰により数学的統計に基づいたトレンド判断を提供

- リスク管理の充実:利確・損切りメカニズムを統合

- パラメータ調整の高自由度:主要パラメータは異なる市場特性に応じて最適化可能

戦略のリスク

- パラメータ感応度:市場環境の変化に応じて頻繁なパラメータ調整が必要となる可能性

- シグナルの遅延:移動平均系指標には一定のラグが存在

- レンジ相場での不適応:横ばいのレンジ相場では偽シグナルが発生する可能性

- 二重確認による機会損失:厳格な二指標確認により、一部の良好な取引機会を逃す可能性

戦略の最適化方向

- 市場環境認識の追加:ボラティリティ指標を導入しトレンド相場とレンジ相場を区別

- 動的パラメータ調整:市場状態に応じてMACDと線形回帰のパラメータを自動調整

- 利確・損切りの最適化:動的な利確・損切りを導入し、市場の変動度に応じて自動調整

- 取引量分析の追加:出来高指標と組み合わせてシグナルの信頼性を向上

- 時間周期分析の導入:複数時間周期の確認により取引精度を向上

まとめ

本戦略は、古典的指標の改良版と統計学的手法を組み合わせることで、柔軟性と信頼性を兼ね備えた取引システムを構築しています。モジュール設計により、トレーダーは異なる市場環境に応じて戦略パラメータやシグナル確認メカニズムを柔軟に調整できます。継続的な最適化と改良により、本戦略は様々な市場環境で安定したパフォーマンスを発揮することが期待されます。

Source

Pine

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('SIMPLIFIED MACD & LRS Backtest by NHBProd', overlay=false)

// Function to calculate TEMA (Triple Exponential Moving Average)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1