1

Follow

1802

Followers

概要

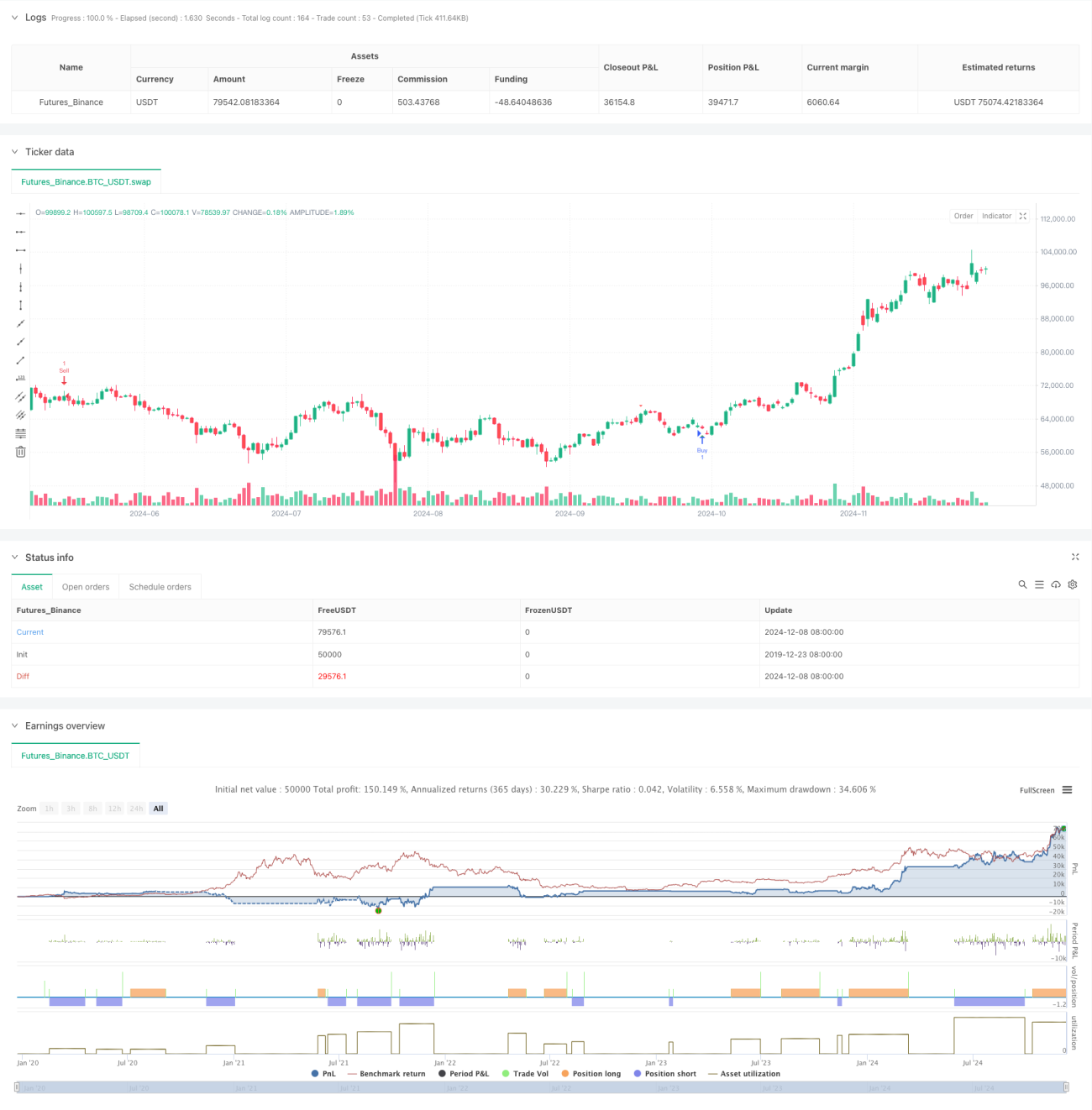

本戦略は、加速オシレーター(AC)とストキャスティクス(Stochastic)を組み合わせた定量取引システムです。価格とテクニカル指標の間のダイバージェンスを識別することで市場のモメンタムの変化を捉え、潜在的なトレンド反転を予測します。また、移動平均線(SMA)と相対力指数(RSI)を統合してシグナルの信頼性を高め、固定の利確・損切りポイントを設定してリスクを管理します。

戦略の原理

戦略の核心ロジックは、複数のテクニカル指標の協調に基づきます。まず加速オシレーター(AC)を計算します。これは価格の中値の5期間と34期間の移動平均線の差から、さらにそのN期間移動平均線を引いたものです。同時にストキャスティクスのK値とD値を計算し、ダイバージェンスシグナルを確認します。価格が新安値を更新する一方でACが上昇する場合、強気のダイバージェンスが形成されます。価格が新高値を更新する一方でACが下落する場合、弱気のダイバージェンスが形成されます。戦略はさらにRSIを補助確認指標として導入し、複数指標のクロス検証によってシグナルの精度を高めます。

戦略の利点

- 複数指標の協調:AC、ストキャスティクス、RSIの3つの指標を組み合わせることで、誤ったシグナルを効果的にフィルタリングできます。

- 自動リスク管理:固定ポイントの利確・損切り設定が組み込まれており、各取引のリスクを効果的にコントロールできます。

- 視覚的なヒント:チャート上に売買シグナルを明確に表示し、トレーダーが機会を素早く識別できるようにします。

- 柔軟性の高さ:パラメータの調整が容易で、異なる市場環境や取引期間に対応できます。

- リアルタイムアラート:リアルタイムアラートシステムが統合されており、取引機会を逃すことがありません。

戦略のリスク

- 偽ブレイクアウトのリスク:レンジ相場では誤ったダイバージェンスシグナルが発生する可能性があります。

- スリッページリスク:固定ポイントの利確・損切りを使用しているため、市場の変動が激しい場合、大きなスリッページが発生する可能性があります。

- パラメータ感応性:異なるパラメータの組み合わせにより、戦略のパフォーマンスに大きな差が生じる可能性があります。

- 市場環境への依存:トレンドが明確でない市場では、戦略の効果が低下する可能性があります。

- シグナルの遅延:移動平均線を使用した計算のため、シグナルに一定の遅延が生じる可能性があります。

戦略の最適化方向性

- 動的な利確・損切り:市場のボラティリティに応じて利確・損切りポイントを動的に調整できます。

- 出来高指標の導入:出来高による確認を追加することで、シグナルの信頼性を高められます。

- 市場環境フィルター:トレンド判定モジュールを追加し、異なる市場環境で異なる取引戦略を採用します。

- パラメータ選択の最適化:機械学習手法を用いて各指標のパラメータ組み合わせを最適化します。

- 時間フィルターの追加:市場の時間特性を考慮し、不利な時間帯の取引を回避します。

まとめ

これは複数のテクニカル指標を融合した定量取引戦略であり、ダイバージェンスシグナルを利用して市場の転換点を捉えます。戦略の利点は複数指標のクロス検証と完備されたリスク管理システムですが、偽ブレイクアウトやパラメータ最適化などの問題にも注意が必要です。継続的な最適化と改善により、本戦略は異なる市場環境で安定したパフォーマンスを維持することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1