1

Follow

1802

Followers

概要

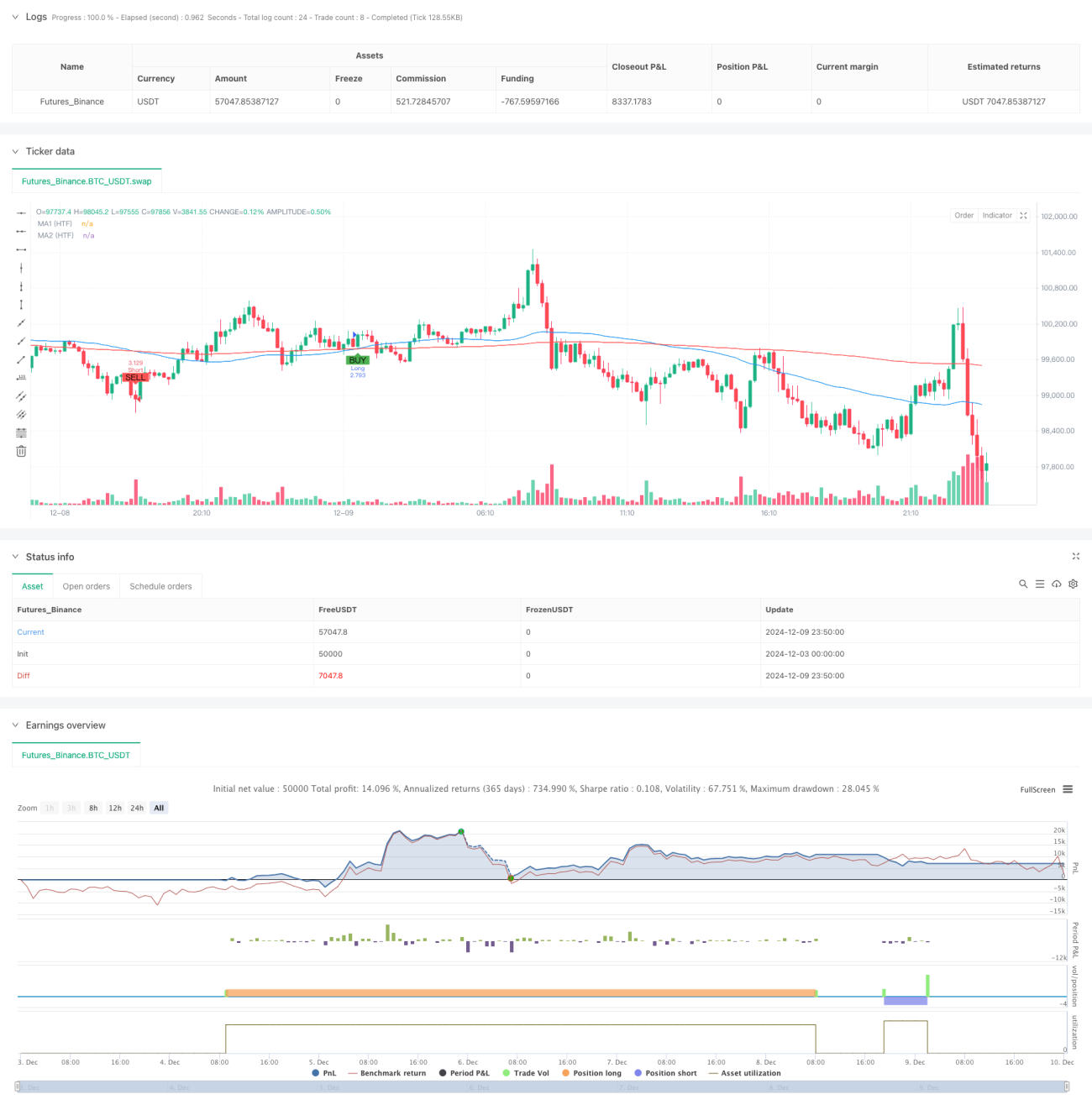

本戦略は、複数の移動平均線とトレンド強度に基づくスマートな取引システムです。価格と異なる期間の移動平均線との乖離度を分析して市場トレンドの強さを測定し、ATRボラティリティ指標を組み合わせてポジション管理とリスクコントロールを行います。高度にカスタマイズ可能であり、さまざまな市場環境や取引ニーズに応じてパラメータを柔軟に調整できます。

戦略の原理

戦略の核心ロジックは以下の点に基づいています:

- 2本の異なる期間(短期と長期)の移動平均線を使用してトレンド方向とクロスシグナルを識別

- 価格と移動平均線の乖離度(ポイント単位)を計算してトレンド強度を定量化

- ローソク足パターン(包み、ハンマー、流れ星、十字線など)を補助確認シグナルとして組み合わせる

- ATR指標を使用してストップロスと利益目標を動的に計算

- 部分利益確定とトレーリングストップによる注文管理を採用

戦略の利点

- システムは高い適応性を持ち、パラメータ調整によりさまざまな市場環境に対応可能

- 乖離度でトレンド強度を定量化し、トレンドが弱い場面での頻繁な取引を回避

- 複数のテクニカル指標とパターン確認を組み合わせ、取引シグナルの信頼性を向上

- ATRベースの動的ストップロス方式を採用し、リスクを適切に管理

- 複利と固定ロットの2つの資金管理方式に対応

- 部分利益確定とトレーリングストップ機能により、利益を効果的に保護

戦略のリスク

- レンジ相場では多くの偽シグナルが発生する可能性があるため、オシレーター系指標によるフィルター追加が推奨される

- 複数の指標を組み合わせることで、一部の取引機会を逃す可能性がある

- パラメータ最適化の過度な実施はオーバーフィッティングのリスクを招く

- 流動性の低い市場では、大口取引がスリッページリスクに直面する可能性がある

- 適切なストップロス比率を設定し、1回の損失が過大にならないようにする必要がある

戦略の最適化方向

- 出来高指標をトレンド確認の補助指標として追加可能

- 市場のボラティリティ指標を導入し、取引頻度を動的に調整することを検討

- 異なる時間枠のトレンド一致性に基づいてシグナルフィルターを実施

- 時間ストップロスなど、より多くのストップロス方式の選択肢を追加

- 適応型パラメータ最適化メカニズムを開発し、戦略の適応性を向上

まとめ

本戦略は、移動平均線、トレンド強度の定量化、ローソク足パターン、動的リスク管理を組み合わせることで、包括的な取引システムを構築しています。戦略ロジックのシンプルさを維持しつつ、複数の確認メカニズムにより取引の信頼性を高めています。高度にカスタマイズ可能であるため、さまざまな取引スタイルや市場環境に適応できますが、使用時にはパラメータ最適化とリスクコントロールに注意が必要です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1