1

Follow

1802

Followers

概要

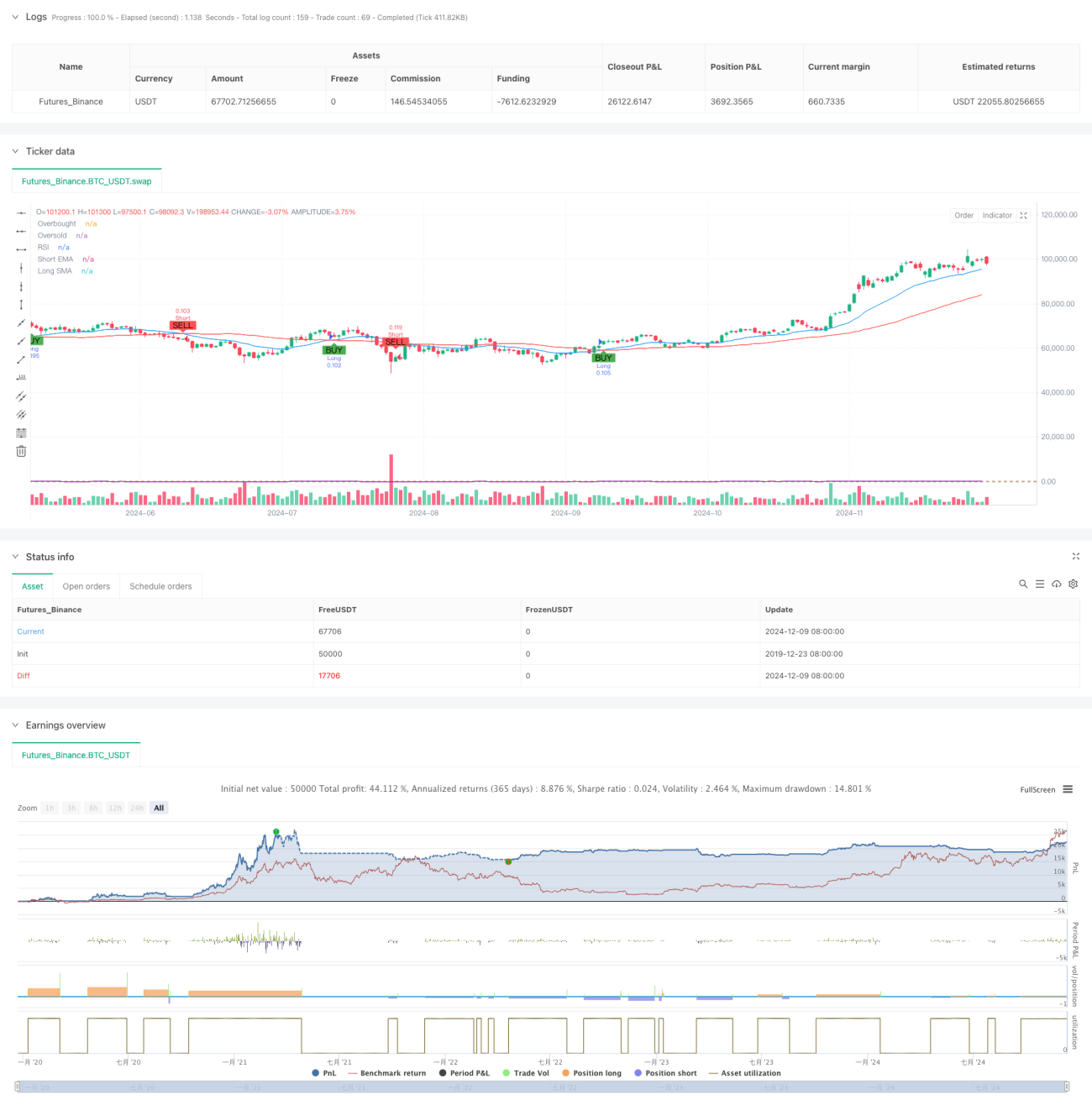

本戦略は、テクニカル指標に基づくスイングトレード戦略であり、移動平均線のクロス、RSIの買われすぎ・売られすぎ、ATRによるストップロス・利益確定など、複数のシグナルを組み合わせています。戦略の核心は、短期EMAと長期SMAのクロスによって市場のトレンドを捉え、同時にRSI指標でシグナルを確認し、ATRによってストップロスと利益確定の位置を動的に設定することです。この戦略はロング・ショート両方向の取引をサポートし、ユーザーの好みに応じて任意の方向を柔軟に有効・無効にできます。

戦略の原理

この戦略は、複数層のテクニカル指標を組み合わせて取引システムを構築します。

- トレンド判断層:20期間EMAと50期間SMAのクロスでトレンドの方向を判断します。EMAがSMAを上抜けた場合はロングシグナル、下抜けた場合はショートシグナルとします。

- モメンタム確認層:RSI指標を用いて買われすぎ・売られすぎを判断します。RSIが70未満の場合はロングを許可し、30超の場合はショートを許可します。

- ボラティリティ計算層:14期間ATRを使用してストップロス・利益確定の位置を計算します。ストップロスはATRの1.5倍、利益確定はATRの3倍に設定します。

- ポジション管理層:初期資金と1回の取引あたりのリスク比率(デフォルト1%)に基づいて、動的に建玉数量を計算します。

戦略の利点

- 複数シグナルの確認:移動平均線クロス、RSI、ATRの3つの指標を組み合わせることで、偽シグナルの影響を効果的に低減します。

- 動的なストップロス・利益確定:ATRに基づいてストップロス・利益確定の位置を動的に調整するため、市場のボラティリティ変化に適応しやすくなります。

- 柔軟な取引方向:市場環境に応じてロングまたはショート取引を個別に有効化できます。

- 厳格なリスク管理:パーセンテージベースのリスク管理と動的なポジション管理により、1回の取引あたりのリスクエクスポージャーを効果的に制御します。

- 可視化サポート:この戦略はシグナルマーカーやインジケーター表示を含む、完全なチャート可視化をサポートしています。

戦略のリスク

- レンジ相場のリスク:横ばいのレンジ相場では、移動平均線クロスが多くの偽シグナルを発生させる可能性があります。

- スリッページリスク:ボラティリティが高い時期には、実際の約定価格がシグナル価格から大きく乖離する可能性があります。

- 資金管理リスク:リスク比率を高く設定し過ぎると、1回の取引で大きな損失が発生する可能性があります。

- パラメータ感度:戦略の効果はパラメータ設定に敏感であり、注意深いチューニングが必要です。

戦略の最適化の方向性

- トレンド強度フィルターの追加:ADX指標を追加して、弱いトレンド環境での取引シグナルをフィルタリングできます。

- 移動平均線期間の最適化:異なる市場サイクルの特性に応じて、移動平均線のパラメータを動的に調整できます。

- ストップロス機構の改善:トレーリングストップロス機能を追加して、利益をより確実に確保できます。

- 出来高確認の追加:補助確認として出来高指標を追加し、シグナルの信頼性を高めます。

- 市場環境の分類:市場環境認識モジュールを追加し、異なる市場環境で異なるパラメータセットを使用します。

まとめ

本戦略は、複数のテクニカル指標を組み合わせて使用することで、比較的完全な取引システムを構築しています。戦略の利点はシグナル確認の信頼性とリスク管理の完全性にありますが、市場環境が戦略のパフォーマンスに与える影響にも注意が必要です。提案された最適化の方向性を通じて、戦略にはさらなる改善の余地があります。実運用に適用する際には、十分なパラメータテストとバックテストによる検証を推奨します。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © CryptoRonin84

//@version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1