1

Follow

1802

Followers

概要

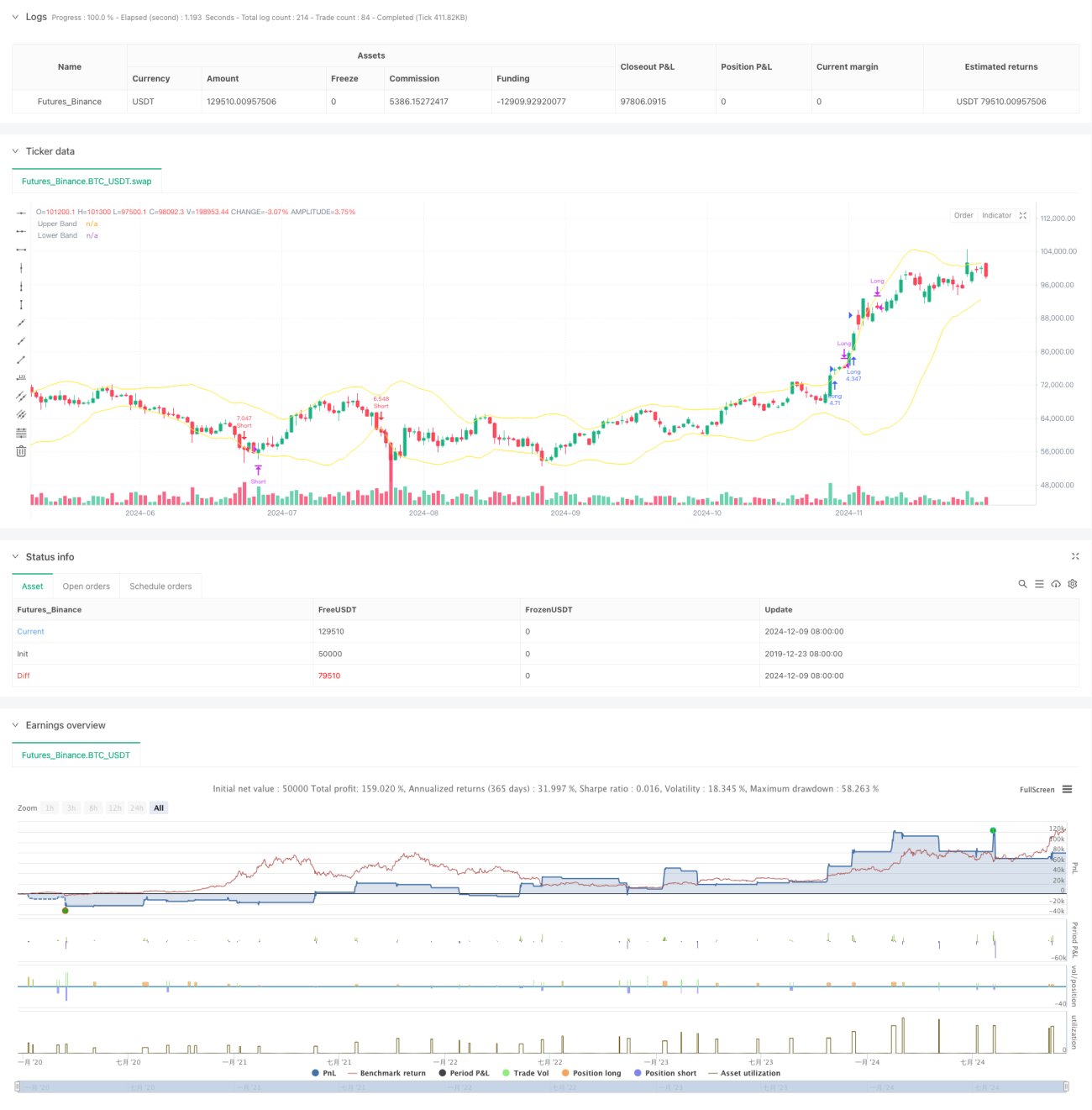

本戦略は、ボリンジャーバンドインジケーターをベースとした4時間足レベルの定量取引システムであり、トレンドブレイクアウトと平均回帰の取引概念を組み合わせています。戦略は、ボリンジャーバンドの上限・下限ラインのブレイクを捉えて市場のモメンタムを取得し、同時に価格が平均値に回帰する性質を利用して利確を行い、ストップロスによりリスクを管理します。レバレッジ3倍を採用し、収益を確保しつつリスク管理も十分に考慮しています。

戦略原理

戦略のコアロジックは以下の主要要素に基づいています。

- 20期間の移動平均線をボリンジャーバンドの中央線とし、2倍の標準偏差を変動幅とする。

- ポジション構築シグナル:ローソク足の実体(始値と終値の平均)が上限ラインをブレイクした場合に買い、下限ラインをブレイクした場合に売りを仕掛ける。

- ポジション決済シグナル:買いポジション保有時、連続2本のローソク足の終値と始値がともに上限ラインを下回り、かつ終値が始値を下回った場合に決済する。売りポジションでは逆のロジックを採用。

- リスク管理:建倉時に当該ローソク足の最高値/最安値にストップロスを設定し、1回あたりの損失を管理可能な範囲に抑える。

戦略の優位性

- 取引ロジックが明確:トレンドと平均回帰の2つの取引思考を組み合わせ、異なる市場環境でも良好なパフォーマンスを発揮。

- リスク管理が充実:ローソク足の変動に基づく動的ストップロスを設定し、ドローダウンを効果的に抑制。

- 偽シグナルのフィルタリング:終値のみではなくローソク足の実体の位置を判断してブレイクを確認することで、偽のブレイクによる損失を軽減。

- 資金管理が合理的:口座残高に応じてポジションサイズを動的に調整し、収益を確保しつつリスクを管理。

戦略のリスク

- レンジ相場リスク:もみ合い相場では偽のブレイクシグナルが頻発し、連続ストップロスが発生する可能性。

- レバレッジリスク:レバレッジ3倍は急激な変動時に大きな損失をもたらす可能性。

- ストップロス設定リスク:ローソク足の最高値/最安値に設定するストップロスは緩すぎる可能性があり、1回あたりの損失が拡大。

- 時間足依存:4時間足は市場環境によって反応が遅すぎ、相場の動きを見逃す可能性。

戦略の最適化方向

- トレンドフィルターの導入:より長期のトレンド判断指標を追加し、メイントレンド方向に取引する。

- ストップロス方式の最適化:ATRやボリンジャーバンド幅を用いてストップロス距離を動的に調整することを検討。

- ポジション管理の追加:変動率やトレンド強度に応じてレバレッジ倍率を動的に調整。

- 市場環境判断の追加:出来高や変動率指標を導入し、現在の市場状態を識別して選択的にポジションを構築。

まとめ

本戦略は、ボリンジャーバンドのトレンドフォローと平均回帰特性を組み合わせたものであり、厳格な建玉・決済条件とリスク管理措置により、トレンド相場とレンジ相場の両方で安定した収益を上げることを目的としています。戦略のコア優位性は明確な取引ロジックと充実したリスク管理体系にありますが、レバレッジの使用や市場環境判断の最適化に注意し、戦略の安定性と収益力をさらに向上させる必要があります。

Source

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Bollinger 4H Follow", overlay=true, initial_capital=300, commission_type=strategy.commission.percent, commission_value=0.04)

// StartYear = input(2022,"Backtest Start Year")

// StartMonth = input(1,"Backtest Start Month") Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1