1

Follow

1802

Followers

概要

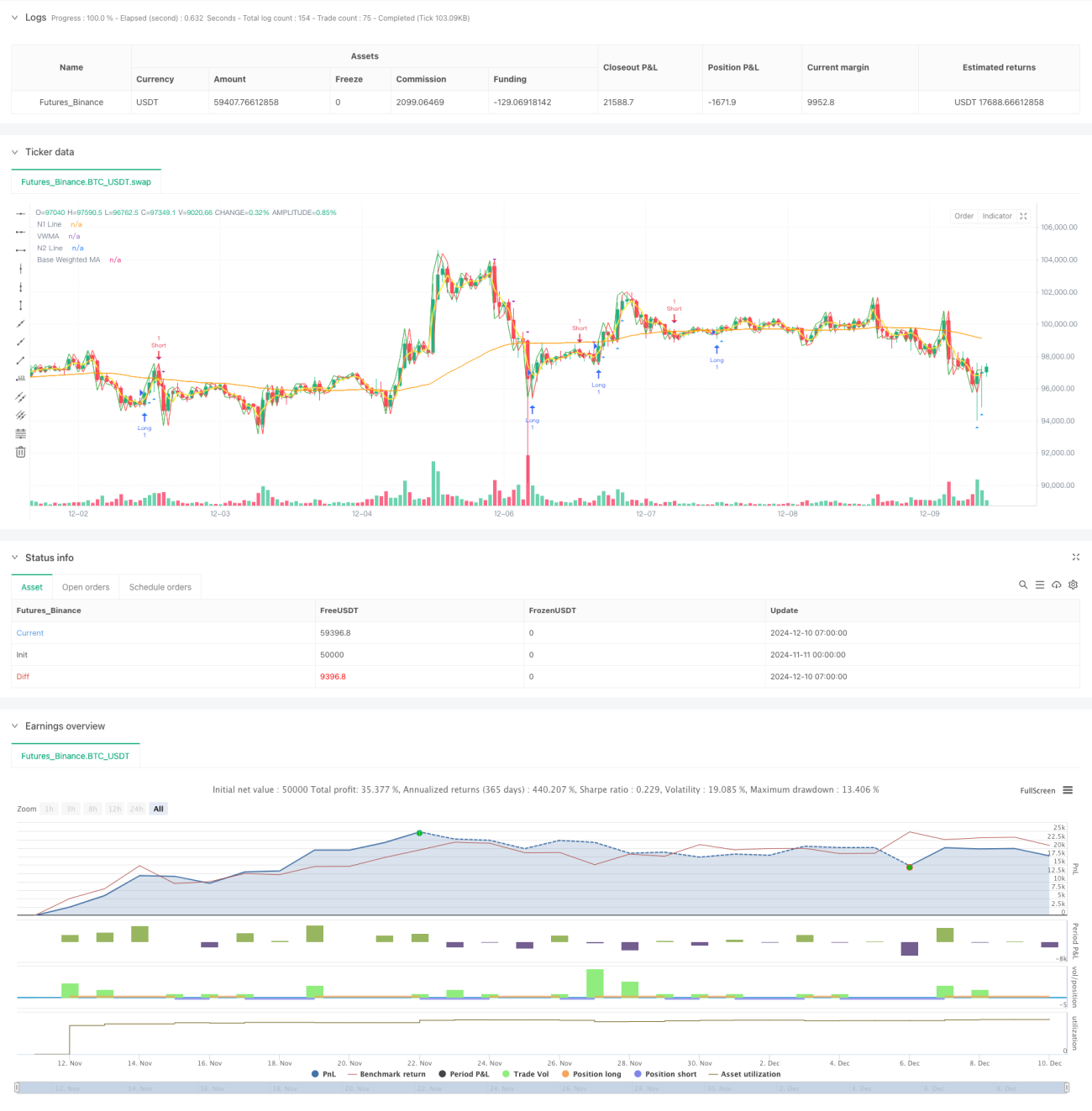

本戦略は、複数の移動平均線、相対力指数(RSI)、平均方向性指数(ADX)、および出来高分析を組み合わせた総合的な定量取引システムです。複数のテクニカル指標を連携させることで、トレンドが確認された上で取引を行い、出来高やモメンタム指標によるフィルターを活用して取引の信頼性を高めます。

戦略の原理

戦略の中核ロジックは、以下の主要コンポーネントに基づいています。

- 二重ヘル移動平均(Double HullMA)、出来高加重移動平均(VWMA)、および基本加重移動平均(WMA)を用いて複数移動平均システムを構築

- ADX指標でトレンドの強さを判断し、トレンドが明確な場合のみ取引を行う

- RSI指標で極端な市場状態をフィルタリングし、買われ過ぎ・売られ過ぎの領域での取引を回避

- 出来高分析と組み合わせ、取引シグナル発生時に出来高が一定の閾値を超えていることを要求

- n1線とn2線のクロスにより具体的な取引方向を決定

複数移動平均システムは価格トレンドの基準判断を提供し、ADXはトレンドが十分に強い場合のみ取引を行うことを保証し、RSIは高値掴みや底値売りを防ぎ、出来高分析は市場の活発な時期に取引が行われることを確保します。

戦略の利点

- 複数の確認メカニズムにより、偽のブレイクアウトのリスクを低減

- テクニカル指標と出来高分析の組み合わせにより取引の信頼性が向上

- RSIで極端な市場状態をフィルタリングし、不利なタイミングでのエントリーを回避

- ADXの使用によりトレンドが明確な場合のみ取引を行い、勝率を向上

- 出来高条件により市場のコンセンサスを確認

- 戦略ロジックが明確で、パラメータ調整の柔軟性が高い

戦略のリスク

- 複数のフィルター条件により、一部の取引機会を逃す可能性がある

- レンジ相場ではパフォーマンスが低下する可能性がある

- パラメータの最適化により過学習のリスクがある

- 移動平均システムは急激な反転相場で反応が遅れる可能性がある

- 出来高フィルターは低流動性市場で取引機会を制限する可能性がある

以下の方法でリスクを管理することを推奨します。

- 市場特性に応じてパラメータを調整

- 適切な損切り・利確を設定

- 1回の取引における資金割合を管理

- 定期的なバックテストによる戦略の有効性検証

戦略の最適化方向

- 適応型パラメータ機構を導入し、市場状態に応じて動的に調整

- 市場変動率フィルターを追加し、高変動期間にポジションサイズを調整

- エグジットメカニズムを強化し、トレーリングストップの検討

- 出来高フィルターを最適化し、絶対値ではなく相対出来高を考慮

- 時間フィルターを追加し、重要なニュース発表期間を避ける

- 価格変動率指標を追加し、市場リスクの識別能力を向上

まとめ

本戦略は、複数のテクニカル指標を連携させることで、比較的完成度の高いトレンド追従システムを構築しています。複数の確認により取引の信頼性を高めつつ、各種フィルターでリスクをコントロールすることが主な特徴です。一部の取引機会を逃す可能性はありますが、全体的に取引の安定性向上に寄与します。提案された最適化方向に従うことで、戦略はさらに改善の余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1