1

Follow

1802

Followers

概要

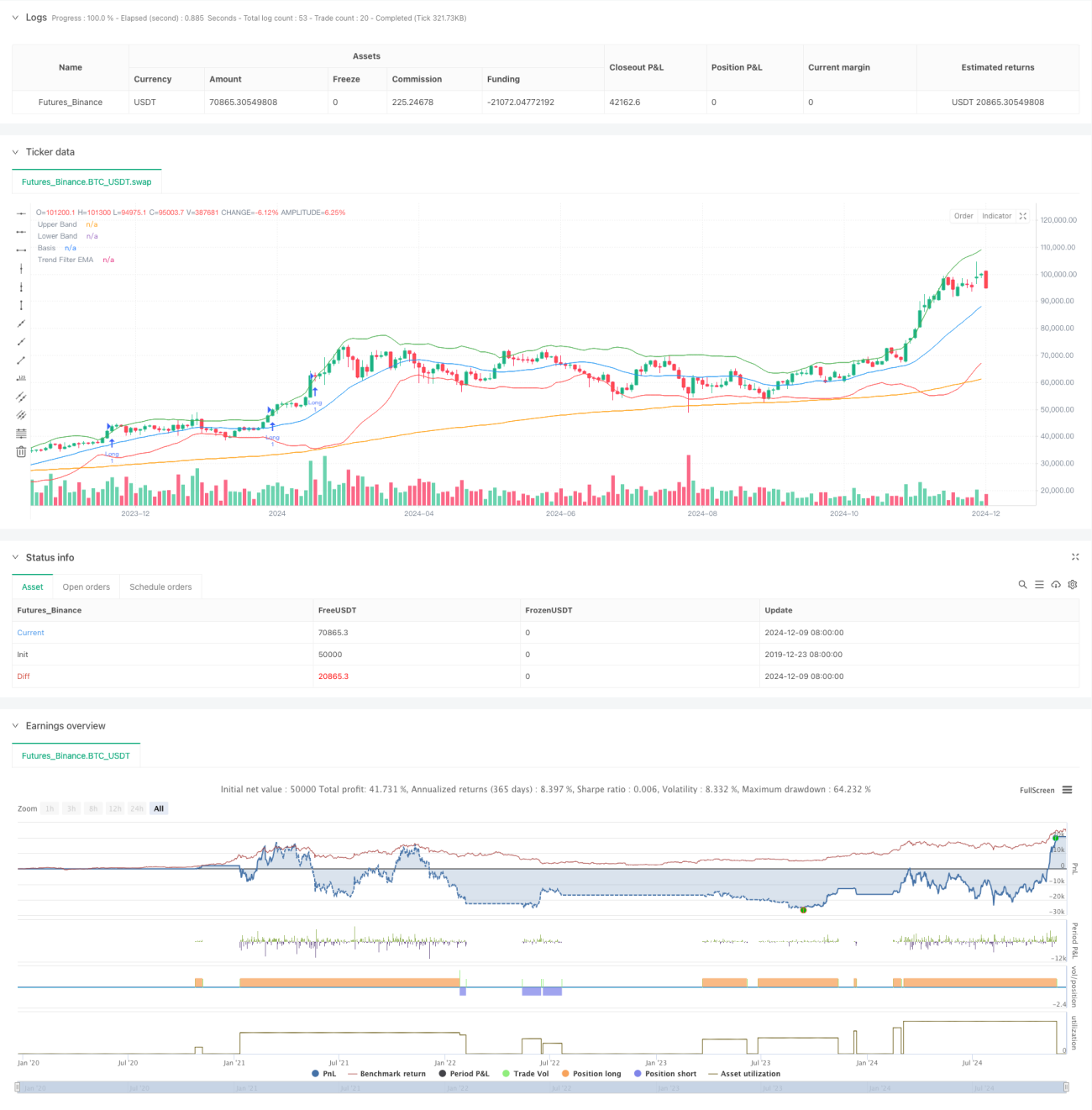

本戦略は、ボリンジャーバンド、RSIインジケーター、200周期EMAトレンドフィルターを組み合わせた、高度な定量取引システムです。複数のテクニカル指標を連携させることで、トレンド方向における高確率なブレイクアウト機会を捉えつつ、レンジ相場での錯誤シグナルを効果的にフィルタリングします。動的なストップロスとリスク・リワード比に基づく利益確定目標を採用し、安定的なトレードパフォーマンスを目指します。

戦略の原理

戦略の中心ロジックは、以下の3つの層に基づいています。

- ボリンジャーバンドブレイクアウトシグナル:ボリンジャーバンドの上下バンドをボラティリティチャネルとして利用し、価格が上バンドを突破すれば買いシグナル、下バンドを突破すれば売りシグナルとします。

- RSIモメンタム確認:RSIが50以上で買いモメンタム、50未満で売りモメンタムを確認し、トレンドがない局面での取引を回避します。

- EMAトレンドフィルター:200周期EMAでメイントレンドを判断し、トレンド方向にのみポジションを取ります。価格がEMAより上なら買い、下なら売りとします。

取引確認には以下の条件が必要です。

- 連続する2本のローソク足がブレイク状態を維持

- 出来高が20周期平均を上回る

- ATR値に基づく動的ストップロス

- リスク・リワード比1.5倍に基づく利益確定目標

戦略の利点

- 複数のテクニカル指標による連携フィルタリングにより、シグナル品質が大幅に向上

- 市場のボラティリティに応じて動的に調整されるポジション管理メカニズム

- 厳格な取引確認メカニズムにより、錯誤シグナルを効果的に低減

- 動的ストップロスと固定リスク・リワード比を含む完全なリスク管理システム

- 柔軟なパラメータ最適化の余地があり、様々な市場環境に適応可能

戦略のリスク

- パラメータ最適化の過剰によりオーバーフィッティングが発生する可能性

- 急激な変動相場では頻繁なストップロスが発生する可能性

- レンジ相場では連続損失が発生する可能性

- トレンド転換点でのシグナルの遅れ

- テクニカル指標間で矛盾するシグナルが発生する可能性

リスク管理の推奨事項:

- ストップロスルールを厳守

- 1回の取引リスクを制御

- 定期的にバックテストを行いパラメータの有効性を検証

- ファンダメンタル分析と組み合わせる

- 過剰な取引を避ける

戦略の最適化方向性

- より多くのテクニカル指標を導入して相互検証

- 適応型パラメータ最適化メカニズムの開発

- マーケットセンチメント指標の追加

- 取引確認メカニズムの最適化

- より柔軟なポジション管理システムの開発

主な最適化のアイデア:

- 異なる市場サイクルに応じて動的にパラメータを調整

- 取引フィルター条件を追加

- リスク・リワード比の設定を最適化

- ストップロスメカニズムを改善

- よりインテリジェントなシグナル確認システムの開発

まとめ

本戦略は、ボリンジャーバンド、RSI、EMAなどのテクニカル指標を有機的に組み合わせることで、完全な取引システムを構築しています。取引品質を確保しつつ、厳格なリスク管理と柔軟なパラメータ最適化の余地により、実戦での高い応用価値を示しています。トレーダーは、実取引においてパラメータを慎重に検証し、取引規律を厳守し、継続的に戦略パフォーマンスを最適化することを推奨します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1