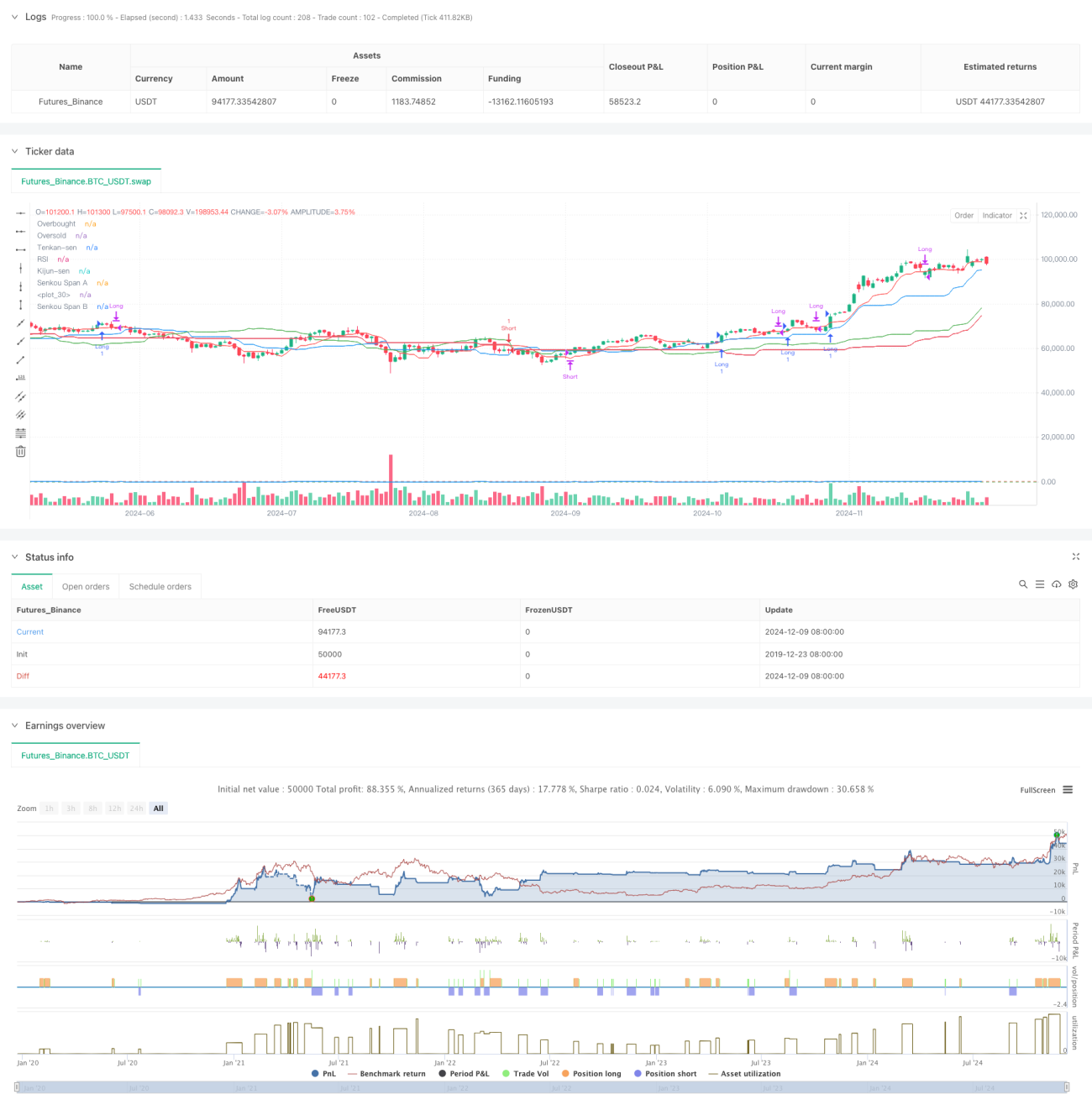

トレンドフォロー型一目均衡表モメンタムダイバージェンス戦略

概要

本戦略は、一目均衡表(Ichimoku Cloud)、相対力指数(RSI)、移動平均収束拡散法(MACD)を融合した総合的なトレンドフォロー型取引システムです。この戦略では、雲図で全体のトレンド方向を判断し、RSIで価格のモメンタムを確認し、さらにMACDシグナルラインのクロスを利用して具体的な取引タイミングを決定することで、多面的な市場分析と取引判断を実現します。

戦略の原理

戦略の中核ロジックは、3つのテクニカル指標の連携に基づいています。

- 一目均衡表はトレンド環境を判断するために用いられ、価格が雲の上にある場合は強気トレンド、雲の下にある場合は弱気トレンドを識別します。

- RSIは極端な相場をフィルタリングするために使用され、買いの場合にはRSIが30より高い(売られすぎではない)、売りの場合にはRSIが70より低い(買われすぎではない)ことを要求します。

- MACDシグナルラインのクロスが具体的なエントリーとエグジットのトリガー条件であり、MACDラインがシグナルラインを上抜けたら買いエントリー、下抜けたら売りエントリーとします。

戦略の取引ルールは以下の通りです。

買い条件:

- 価格が雲の上にある

- RSIが30より大きい

- MACDラインがシグナルラインを上抜ける

売り条件:

- 価格が雲の下にある

- RSIが70より小さい

- MACDラインがシグナルラインを下抜ける

戦略の優位性

- 多重確認メカニズム:3つの独立した指標を統合することで、偽シグナルの影響を低減。

- トレンドフォロー性の高さ:一目均衡表の使用により、明確なトレンドの中で戦略が動作することを保証。

- リスク管理の充実:RSIによるフィルタリングにより、過度な買われすぎ・売られすぎ領域でのエントリーを回避。

- シグナルの明瞭性:MACDクロスが明確なエントリー・エグジットシグナルを提供。

- 適応性の高さ:異なる市場環境や取引銘柄に適用可能。

戦略のリスク

-

トレンド転換リスク:トレンドの転換点で連続的な損失が発生する可能性。

対策:トレンド確認の時間軸要件を追加することを推奨。 -

レンジ相場リスク:レンジ相場では頻繁な取引が発生する可能性。

対策:最小変動幅の要求など、シグナルのフィルタ条件を追加することを推奨。 -

ラグ性リスク:すべての指標に一定のラグが存在し、最適なエントリーポイントを逃す可能性。

対策:より高速な指標や価格アクション分析と組み合わせることを推奨。 -

パラメータ感応性:誤ったパラメータ設定により戦略のパフォーマンスが低下する可能性。

対策:バックテストによる最適化を行い、適切なパラメータ組み合わせを決定する必要がある。

戦略の最適化方向

-

動的パラメータ調整:

- 市場のボラティリティに応じて雲図のパラメータを自動調整

- 市場環境に基づいてRSIの閾値を動的に調整

- MACDパラメータの適応的最適化

-

市場環境フィルタの追加:

- ボラティリティ指標を追加し、低ボラティリティ期間をフィルタリング

- 出来高確認メカニズムの導入

- より多くの市場サイクル情報の考慮

-

リスク管理の強化:

- 動的ストップロス戦略の実現

- ポジションサイジングメカニズムの追加

- より柔軟なエグジットメカニズムの設計

まとめ

本戦略は、一目均衡表、RSI、MACDという3つのクラシックなテクニカル指標を組み合わせることで、完全なトレンドフォロー型取引システムを構築しています。戦略の主な優位性は多重確認メカニズムと明確な取引ルールにありますが、同時にトレンド転換点やレンジ相場によるリスクに注意する必要があります。動的パラメータ調整、市場環境フィルタ、リスク管理の最適化により、戦略の安定性と収益性のさらなる向上が期待できます。

- 1